I. Current realities in the gold market

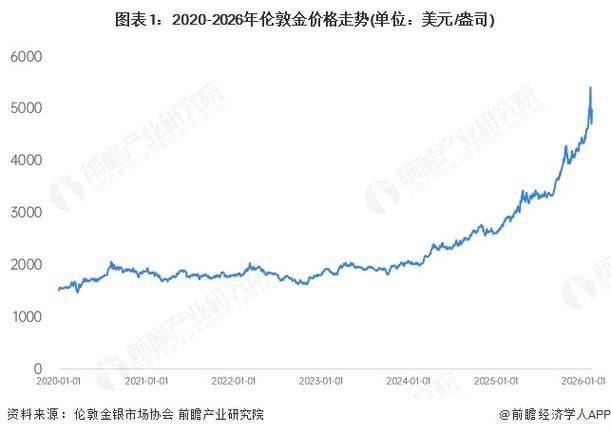

As of 22 april 2026, the latest market data show that international spot gold prices were $4759. 49 per ounce, up from a historical high of $4,800 in mid-march, with a return of about 1. 7 per cent, with a minimum of $4553 for the period; the domestic principal collection price of $1051. 4/g; and the domestic mainstream gold store's full retail price of $1448-1457/g, with bank investment gold prices of approximately $1060-1067/g。

In terms of trends, this turnback is a normal technical adjustment and is not a downward trend. Over the past year, the cumulative increase in international gold prices has exceeded 35 per cent and has accumulated a large margin of profitability, with short-term gains as normal for the market, influenced by the expected changes in the federal reserve policy。

Ii. Short term (1-3 months): concussion shock, but with limited fall space

In the coming months, the price of gold does face a certain amount of repression, but at the same time it also has a strong supporting force, with a general pattern of high-level shocks and no sustained collapse。

Main constraints

First, the fed’s interest rate reduction is expected to be substantially delayed. The march fed conference reduced interest rate reductions from three to one for the whole year, with the first reduction postponed from june, which was widely expected in the market, to september. The imf, in its annual economic assessment of the united states, published in april, noted that the fed could only reduce interest rates once this year, at most, owing to the risks of a rebound in inflation, a robust job market and rising energy prices. The current 10-year rate of return on united states debt has risen to 4. 39 per cent, and the opportunity cost of holding gold has risen, stifling gold prices。

The second is the short-term depression of some central banks. A few countries, such as turkey, have recently concentrated on the sale of gold reserves in order to stabilize their exchange rates, causing short-term liquidity shocks. However, such sales are the special needs of individual countries and are not common to global central banks。

The third is the continued outflow of gold etf funds. The world's largest gold etf, spdr gold shares, has continued to decline since this year, reflecting short-term market sentiment。

Core support factor (closure of fall space)

Despite the above-mentioned disincentives, the three cores have secured the drop in gold prices, leaving a very low probability of breaking down $4,400/ounce。

First, central bank purchases form a solid “policy base”. Forty-four hundred-six hundred dollars per ounce is the global central bank's cost line of intensive money purchases, and once the price of the money breaks down, it triggers a massive sweep by central banks。

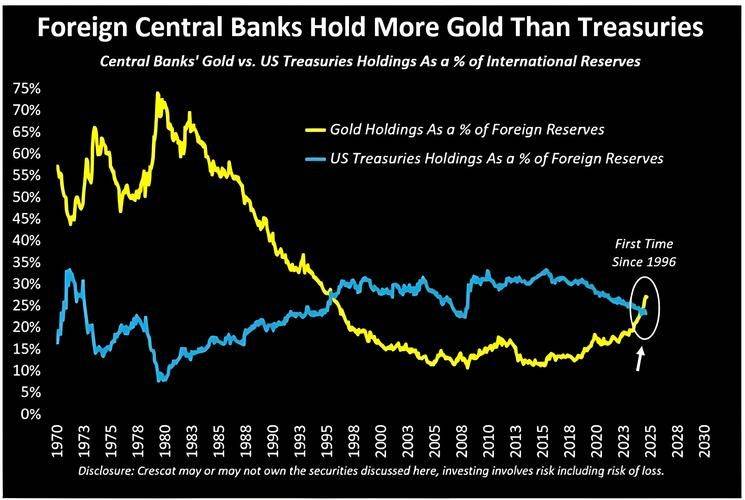

Second, the continued strategy of global central banks is to increase gold. World gold association data show that global central bank net purchases reached 215 tons in the first quarter of 2026 and have remained net buying for 19 consecutive months, with annual net purchases expected to remain at a high level of 800 to 850 tons, well above historical averages。

Third, the central bank of china held gold for 17 consecutive months. By the end of march 2026, china's gold reserves stood at 2313. 48 tons, with an increase of 4. 98 tons per month in march, the highest level since nearly 13 months. This sustained and steady increase provides a strong underpinning for gold prices。

Iii. Medium term (3-12 months): expected to restart the rise after the fall

In the medium term, the core trigger for the resumption of the price increase was the start-up interest rate of the federal reserve. It is now widely expected that the fed will reduce interest rates for the first time in september 2026. In short, the fed interest rate drops mean lower interest on the united states dollar, lower earnings from holding the dollar, and the relative attractiveness of gold as an asset without interest increases significantly, thus attracting large sums of money back to the gold market。

Many international agencies are also optimistic about the medium-term price trend. Gold is expected to rise to about $4,900 per ounce at the end of 2026; morgan chase is more optimistic that it is expected to rise to $5055 per ounce in the fourth quarter and that there is a possibility of an upward look at $6,000; and eastern kincheng predicts that the price of gold is expected to rise to $6,000 per ounce in 2026。

It is important to note that these projections are based on the current economic and policy environment and that actual trends may be adjusted by factors such as inflation data, employment and geo-situations。

Iv. Long term (over one year): the pattern of cattle markets remains unchanged

In the long run, the three core logics underlying the gold price rise have not changed, and the long-term cattle market pattern of gold remains solid。

First, the global de-dollarization process has accelerated. The current share of the united states dollar in global foreign exchange reserves has fallen to 56. 92 per cent, a new low since 1995. Central banks are increasing their reserves of gold, essentially in order to spread risks and reduce dependence on the united states dollar. Gold's position as a “non-sovereign risk asset” is becoming more important。

Secondly, the united states debt crisis continues to worsen. The united states federal government's debt has exceeded $38 trillion, with a widening fiscal deficit and increasing fiscal vulnerability, which will long weaken the united states dollar's credit system and improve gold prices。

Third, geo-risk regularization. The long-standing systemic risks of conflict in the middle east, big power games, and the value of gold as a traditional risk-averse asset and hedge currency credit risk will continue to grow。

V. Risk tips and rational investment advice

There is, of course, some uncertainty about the evolution of gold prices. There may be a more substantial return on the price of gold if: the first is the continued rebound in inflation in the united states, where the fed does not fall or even resume the hike throughout the year; the second is that geo-conflicts have eased considerably and the need for risk avoidance has receded rapidly; and the third is that global central banks have significantly lower-than-anticipated money purchases。

For ordinary investors, the investment value of gold needs to be viewed rationally. For those who have just to buy gold jewelry, it is possible to start with the right price, without overstretching short-term fluctuations of several grams, after all, the main value of gold jewelry is wearing and remembering. For those who want to invest in gold, it is recommended that they buy in batches, not in one-time silos or leverage investments. Low-risk varieties such as bank gold bars and gold etfs can be selected to avoid irregular investment in platforms and products。

In short, gold is a long-term asset, not a tool for short-term speculation. Only by maintaining a rational investment mentality can there be a steady return on market volatility。

♪ i'm gonna go to the headline ♪