“not as much as they say `doing nothing' and not very much `capturing horses', but the flow of people on commercial projects is not very large.” a former property mediaman recently told daily economics reporters how he felt when he saw business projects that had been reported earlier in his absence。

So, how was the commercial real estate market over the past 2022

In recent days, institutions such as the institute of research, the deeds liner and wisdom have been issuing annual reports on the commercial property market of 2022. According to a report issued by the institute on 18 january, the country's commercial premises, investment in office buildings and the area of sale had declined in comparison to the average, the volume of large transactions in 20 key cities had fallen significantly and the rent of writing buildings and shops continued to fall。

“on the macro level, the epidemic has strained the services economy and the consumer market, thereby impacting on the commercial real estate sector, with investment in commercial housing and a decline in the area of sale, a contraction in the size of supply and demand for commercial land and a downward pressure on the market as a whole.”。

Commercial housing investment and sales dropped at the same time

The market as a whole is exposed to downward pressure in terms of its commercial dimensions。

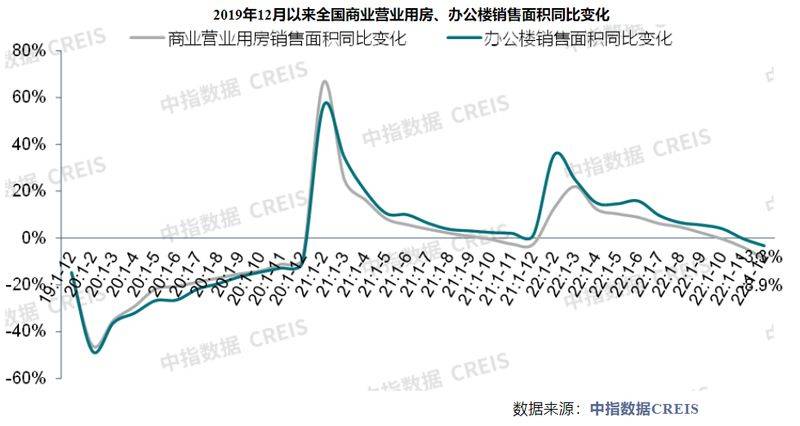

Data from the institute show a decline in commercial business premises, investment in office buildings and sales area by year in 2022, and a negative monthly increase in commercial property sales since the second quarter。

In the area of commercial housing, the total area sold in 2022 was 8,239 million square metres, a decrease of 8. 9 per cent over the same period; of this, the total area sold in december 2022 was 1,05 million square metres, a decrease of 33. 7 per cent over the same period; and, since july 2022, the total area sold in the single month of commercial housing has decreased for six months。

In terms of office buildings, the total area sold in 2022 was 3,264,000 square metres, a decrease of 3. 3 per cent over the same period; of that total, 4. 44 million square metres was sold in december, a decrease of 18. 9 per cent over the same period; and, since july, the total area sold in office buildings for one month, with the exception of september, had decreased in the same period。

Low market confidence and continued negative sales have somewhat slowed the continued supply of commercial land. In 2022, the total area of commercial land in 300 cities nationwide was 200580,000 square metres, a decrease of 23. 3 per cent over the same period; the total area traded was 1. 7658 million square metres, a decrease of 17. 6 per cent over the same period. This represents a decrease of over 50 per cent in december。

The institute's analysis suggests that some urban epidemics have been repeated in the last quarter of the year, particularly since late november, with a contraction in demand, supply shocks, an increase in the “triple pressure” expected to slow down, constraining economic recovery and a decline in the economic activity of services, which is more relevant to the rental market for writing buildings. Although the overall rental demand for key urban writing buildings continues to be released, the rate of demand release has slowed down in some cities, and even more rent withdrawals have occurred, owing to adverse factors。

The 20-city deal is worth the same amount as the "cut off."

Major national trade investments have also been suspended owing to multiple factors such as the global economy, policies and recurrent epidemics。

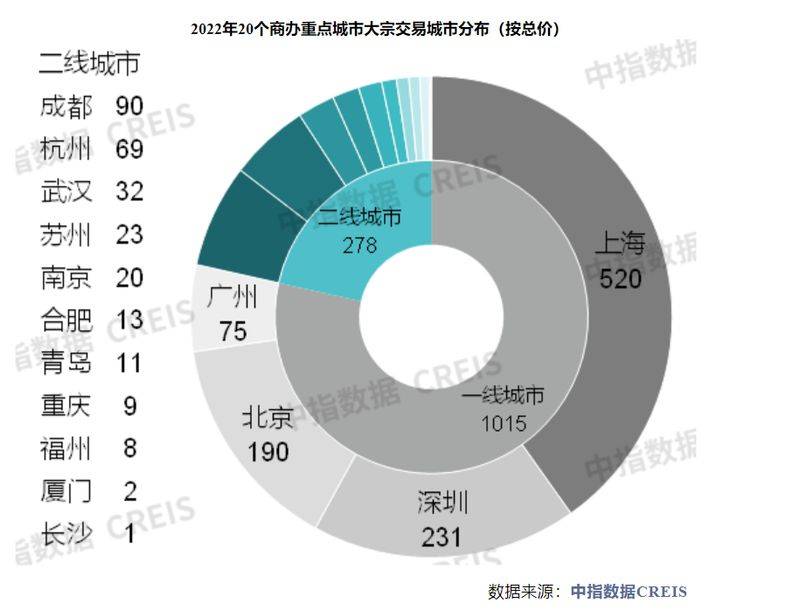

According to the institute, in 20 of the key cities that monitored data in 2022, 141 large transactions were monitored, a decrease of 78 transactions compared to 2021; the value of transactions was $12. 9 billion, a decrease of 50 per cent。

At the urban level, the number of major transactions in front-line cities was 87, or 62 per cent. Of these, shanghai, beijing, shenzhen and guangzhou have 47 transactions, 18, 13 and 9; shanghai and beijing are still the most active cities; the second-line cities are significantly less active than the first-line cities, of which chengdu, hangzhou, chongqing, suzhou and wuhan have 5-10 transactions, while the rest are within 5 cases。

In terms of the type of buyer, the investment activity of the domestic finance buyer remained the most active, accounting for 82 per cent, based on transactions that had disclosed the buyer in 2022. In terms of the type of vendor enterprise, as the real estate market enters the adjustment period, some firms choose to sell high-quality assets in order to ease financial pressure, with over 50 per cent of the total number of transactions by the sellers comprising the housing company and the company under the flag。

According to the statistics of the cities, the writing complex remains an absolute bargaining force for large transactions. According to shenzhen's statistics, the value of writing buildings is as high as 89. 7 per cent; in industrial property transactions, three transactions were recorded throughout the year, all in bright and new areas。

With regard to the large transactions recorded next year, u wei dong, director-general of the shenzhen branch of the world bank, concluded that the fall of the financial “three arrows” would be beneficial for the development of housing enterprises in the coming year, and would indeed ease the financial pressure on developers. The willingness to sell the assets of small and medium-sized private enterprises is expected to increase this year, while some state enterprises and high-quality private enterprises are expected to sell assets in order to achieve good business strategy outreach and funding arrangements。

Wu wei dong predicted that the increase in marketable goods would keep the overall market active in 2023. In addition, industrial property will continue to be favoured by investors because of its steady rent performance and the steady returns that can be achieved through the issuance of reits。

Increase in the decline in rent in the real commercial market

Since the second half of 2022, the epidemic has partly slowed down consumption growth and hit the real commercial market。

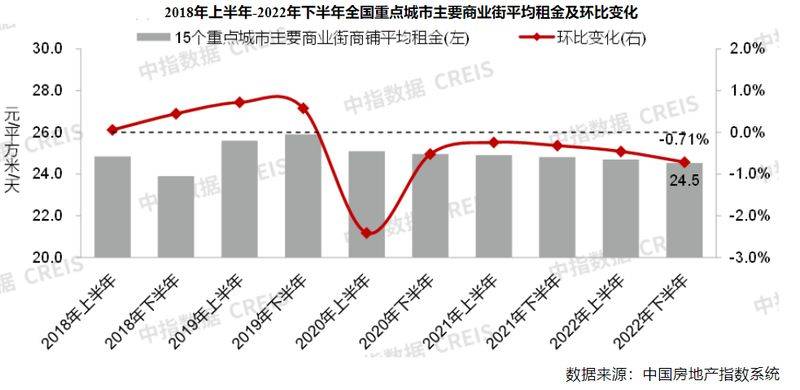

According to the central institute of studies, in the second half of 2022, the rent-rate ratio of commercial shops nationwide increased to 0. 71 per cent, while the rent-rate-rate ratio of commercial shops (shopping centres) decreased by 0. 09 per cent

Of these, the average rent of 100 major commercial street (100m) shops, comprising 100 commercial street shops in priority cities throughout the country, was $24. 53/m2/day, a decrease of 0. 71 per cent in the ring ratio, an increase of 0. 25 percentage points from the second half of 2021; the average rent of 100 shopping malls (100m2/m2/day) made up of 100 typical shopping malls was $26. 94, a decline of 0. 09 per cent from 0. 14 per cent in the ring ratio in the first half of 2022。

Not only has there been an increase in the decline in the rental ring, but the epidemic and market expectations have also affected the pace of entry to multiple shopping centres。

In shenzhen, for example, the market for 24 proposed new projects, with a new size of 1. 99 million square metres compared to the previous market, was expected to open a total of 15 new shopping centres in shenzhen city in 2022, with an additional supply of approximately 1. 32 million square metres and a stock of 21 million square metres. However, it is wise to believe that the market entry project shows a higher standard of business construction, thus also creating new expectations for the business market in 2023。

In addition, according to data from a survey of rental samples from the china real estate index system for writing buildings in major business circles throughout the country, in the fourth quarter of 2022 the average rent for major business buildings in key cities was 4. 74 yuan/m2/day, a decrease of 0. 18 per cent in the ring ratio。

“since late in december last year, consumer markets in some cities have shown signs of warming, and real business traffic has picked up. It is expected that in 2023, when the impact of the epidemic is reduced, consumption will either increase or the consumer market will recover steadily, and a steady recovery of the market for rentals is expected in key urban businesses.”。