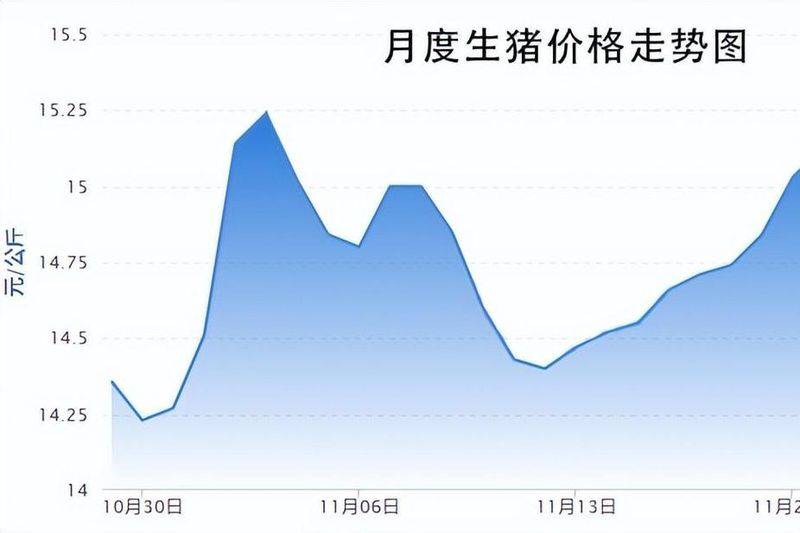

On 27 june, the main contract for pig futures at the dalian commodity exchange was reported at 17615 points, an 18 per cent increase over the closing of 14925 points on 13 july 2023 and a continuous shock for nearly a year. Has the cycle of the expected price of pigs arrived?

The upturn cycle has started

"a new round of pigs has been launched." researcher at the beijing institute of livestock and veterinary research of the chinese academy of agricultural sciences and chief analyst of early warning on the whole chain monitoring of pork industry of the ministry of agriculture and rural development, zhu jinyong, told the journalist。

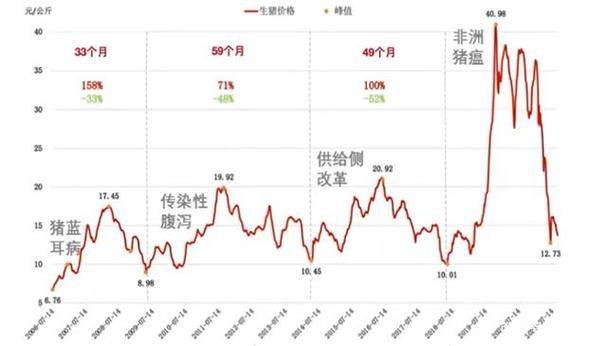

Since 2002, my country has undergone six full rounds of pig cycles. The full cycle of each round includes the up and down phases. The longest of the six completed round (june 2009 to april 2014) was the third round of pigs, lasting 59 months over five years; the shortest was the recently completed sixth round of pigs (april 2022 to march 2024), which lasted 24 months and spans only two years. Starting in april of this year, it rebounded into a new pig cycle。

After a long industry-wide loss, the cycle of price increases for pigs has finally arrived. However, zhu jingyong has reminded operators that reason is still to be maintained. In the case of the recently completed 6th round of pigs, it did not continue to rise for several years, as it had in previous cycles, but from april 2022, when it rose sharply to a point of 26. 64 per kilogram in october, when the movement stopped. Since then, the price of pigs has been falling steadily from november 2022 to 14. 95 yuan/kg in march 2024, due to the availability of sufficient capacity and supplies for the production of pigs, and the panic of super-hogs with two-thirds fertility。

The new changes that have taken place in this recently concluded round of pigs deserve industry vigilance. The sixth round of pig cycle rose from may 2022 to october 2022, in only six months, and the price per kilogram of raw pig increased by 1. 98 yuan/month. The supply side has experienced rapid price increases in the short term due to increases in farmer pressure bars and secondary fertility, increasing the rate of increase in the price of pigs during the cycle. In terms of the rate of decline, the price per kilogram of raw pig fell by $0. 69 per month during the cycle. High levels of supply, combined with declining demand, have led to long-term low prices of pigs。

Import pressure eased

Domestic pig prices have long been significantly higher than international markets and import pressures have been high. For the pig farming industry, the good news is that imports of pork dropped significantly in the first months of the year。

Between january and may this year, my country imported 427,000 tons of pork, a decrease of 47. 1 per cent over the same period, and $830 million over the same period, a decrease of 57. 3 per cent. Spain, brazil, chile, canada, the netherlands and the united states together accounted for 81. 0 per cent of our total imports. Our total imports from eu countries amounted to 201,000 tons, or 47. 1 per cent, a decrease of 3. 8 percentage points compared to the same period of the previous year。

Zhu yingyong stated that the short-term factors affecting our imports of pork were domestic supply and demand relations, domestic pork prices and domestic and international price differentials. In the medium to long term, the factors affecting our imports of pork are the difference in the cost of domestic and international production of raw pigs and the complementarity of consumer demand. Against the backdrop of no major changes in the relevant trade policy, the high price of our pigs and the upside down price of our pork, both domestic and foreign, have been the most important factors driving the surge in our pork imports in some years. Sufficient supplies and a fall in pig prices can in turn drive import demand down rapidly to normal levels。

In terms of domestic and foreign price differentials for pork, the price of pork fell by 2. 7 per cent in the first half of the year, overall at a low level, while the price of pork in the european union and the united states, such as spain, rose at a high level, the price of pork in brazil was relatively high, and the price of domestic and international pork fell sharply. In may, the wholesale price differentials for chinese and spanish, american and brazilian pork were $3. 3, 4. 6 and 6. 6 per kilogram, respectively. The averages for the first five months of the year were $3. 7, 5. 3 and 6. 3 respectively, representing a decrease of 2. 8 per cent, 36. 9 per cent and 9. 1 per cent respectively. The price differentials for domestic and foreign pork have returned to normal levels, with a marked decline in import demand。

In the first half of the year, there was a marked decline in pork imports, which had a small impact on the pig industry and the market. In the medium to long term, there is still a certain rigidity in the cost of domestic pig production compared to the main exporters of pork, especially brazil, the united states and russia, while there is a certain rigidity in our consumption of osteoporosis and pork, although the volume of pork imports is expected to fall back to pre-african pig plague levels, but it will remain at more than a million tons。

Pig prices don't go up much

“as a result of a combination of reductions in pre-production capacity and current trends in pig prices, the price of pigs in the second half of the year will generally show a seasonal upward trend, significantly better than during the same period of the previous year. However, it is less likely that the price of pigs will rise significantly.” chu said。

At the end of the production cycle, there has been a steady decline since last year in the number of women and pigs in the country, thanks to a combination of market-led and capacity-regulated production。

According to data from the national statistics institute, at the end of the first quarter of this year, there were 408. 5 million boars in the country, representing a decrease of 5. 9 per cent in the ring compared to 5. 2 per cent in the same year. In the first quarter, the total number of pigs produced in the country stood at 1945. 5 million, representing a 2. 2 per cent decrease in comparison to the previous year, while the total volume of pork produced was 1. 58 million tons, a 0. 4 per cent decrease. At the end of may, there were 3,996 headloads of pigs, representing an increase of 0. 2 per cent in the ring and a decrease of 6. 2 per cent in the same year. Between january and may, there was a targeted slaughtering of 1,360. 4 million pigs by the company, an increase of 0. 8 per cent over the previous year. The number of slaughters started in february was lower than in the same period of the previous year, and in may, 2,666,000 people were massacred by the scavengers, a decrease of 5. 0 per cent over the same period。

In terms of out-posting, although the comparison was higher than the same period in the previous year, the ring-to-ring ratio decreased slightly, indicating a decrease in the stock of big pigs. The decline in the availability of sows has led to a reduction in the adaptiveness of the production of raw pigs, whose oversupply has largely been reversed and the supply and demand have largely been balanced. According to the ministry of agriculture and rural development, the number of new pigs and pigs in the country decreased slightly in december of last year to may, and in the six-month fertilizer cycle, the number of raw pigs will decrease in the next six months from the same period last year. On the other hand, pork consumption will gradually increase in the second half of the year and peak in the fourth quarter. In other words, in the second half of the year, the pork market will be characterized by strong supply and demand, and pork prices are expected to remain generally upwards。

Zhu yungyong recommended that the relevant government departments stabilize the long-lasting support policy for pig production and guide farmers to rationalize their production and improve biosafety. Based on a scientific understanding of the future supply and demand of pigs, the relevant government departments can optimize long-lasting support policies such as land use, environmental protection, finance and vaccination, and stabilize market expectations, while strengthening policy support for family farms and moderately large chemical farms, avoiding over-concentration of production capacity and truly acting as a market stabilizer for the main breeders of modest size. In view of the fact that second-generation, return-concentration and pressure bars are the main causes of the short-term sharp fluctuations in the price of pigs in recent years, the authorities concerned can strengthen the monitoring and early warning of the boar market, rationally channel market sentiment and reduce the disruption of speculative capital to the boar market. The sector can also optimize fiscal and financial policies, play the role of financial capital in the countercyclical regulation of the pig industry, prevent the production of pigs from being too fast or overreducing, and prevent emotional overheating from leading to low-quality expansion. With regard to the prevention of major animal diseases, the mechanism of joint control can be strengthened, leading to the establishment of the correct concept of epidemiological control in farms, encouraging farmers to raise their level of biological safety on their own initiative and fundamentally enhancing the stability of the production of pigs in the country。