Contents

A while ago, some of my friends who worked in finance threw up at me..

The company has been spending money to promote it, but the sales have not improved and the money seems to have been wasted

Every month at the end of the month, departments resorted to obfuscation of each other's responsibility for budget overruns

It was not possible to judge what money was to be spent and what money was to be spent in the province by looking at the figures on the financial statements, which were so dense。

In fact, these difficulties have come to light, and the central cause is probably the lack of a key task: cost analysis。

And then i'll talk to you in this article from the definition of cost analysis, the perspective of classification and the difference between cost and cost。

I. What is the cost analysis

It is easy to say that cost analysis is the process by which money is spent in a clear and clear manner。

It's not just a bookkeeping, it's a deep-seated story behind every spending: where is the money spent? Why? Is it reasonable to spend it? Is there a better trick? The requirements for cost analysis are higher and more detailed。

The core purpose of the cost analysis is threefold:

Control the costs, improve efficiency: find unnecessary and unreasonable costs, save them or spend them somewhere more important. Supporting decision-making, giving direction: for example, analysing the cost of advertising and the amount of sales that it brings will help us determine which marketing channels are most effective, thus determining the next budget direction. Assessment of performance, implementation of responsibilities: which department was overspent? Which project costs are well controlled? The results of the analysis clearly reflect the effectiveness of team and individual work。

Does that sound familiar? And that's what everybody says about good steel. The cost analysis is the system that helps you find the blade and ensures that the good steel works。

I have always stressed that enterprises that do not carry out cost analyses are financially unclear and that the risks ahead are enormous。

In carrying out the cost analysis, it would be useful to analyse the data, and i suggest that you use a specific data analysis tool, such as finebi, which can analyse the data received and enable material extraction and connectivity to help you visualize changes in content. I put the link here and asked for it: free experience with finebi

Well, it's important to understand, and you're going to look at the big concept of “cost”. There is no analysis without an internal structure。

Three common classification perspectives for cost analysis

The cost is not a piece of iron, and we need to look at it from different angles to see it clearly. There are three main types of classification, each of which has its own usefulness and which have different information。

Perspective i: operational costs

This is the most basic and close to the nature of the business。

It answers the question “what kind of business is everyone's money spent for”, which, frankly, is the part of the business that it is spent on。

Sales costs (or operating expenses): all expenses incurred to sell products or services. For example, the salaries of sales personnel, advertising, hospitality and marketing activities. Management costs: all expenses incurred to maintain the company's overall day-to-day operations. Examples include salaries for administrative personnel, office rent, office supplies and travel. Financial costs: all expenditures related to borrowing and financial management. For example, interest on bank loans, bank charges, exchange losses。

What? That's the advantage of this classification

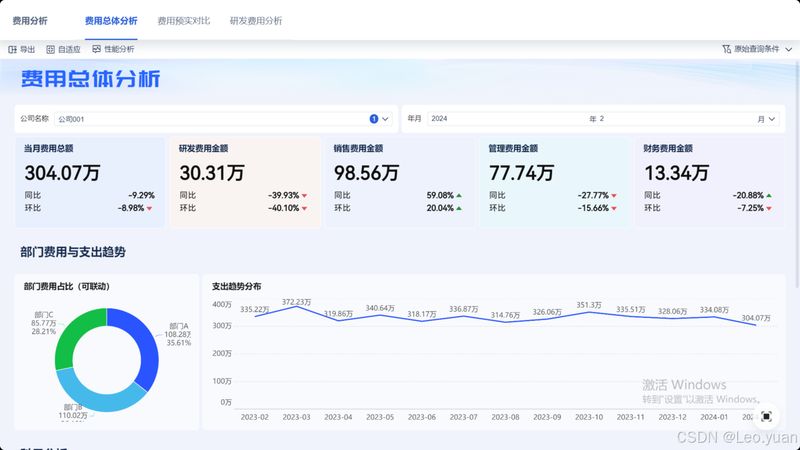

It directly reflects the cost of different business segments of the enterprise. At first glance, you can see whether the company's cost focus is on market opening (high sales costs) or internal management (high management costs)。

For example, based on graphic information, we can figure out that the company's cost focus is on internal management and research and development inputs. Management costs account for the bulk of total costs, followed by r & d costs. This suggests that at this stage, companies may invest more resources in team-building, day-to-day operations management and product or technology development rather than large-scale market promotion。

It is understood that classification by nature is followed by a more decentralized and manageable perspective by sector. After all, money is ultimately spent by a specific department。

Perspective ii: sectoral costs

It's a very intuitive view of where money is spent. The company is made up of various sectors, with a budget that reaches the sector and responsibilities that need to be fulfilled。

Ministry of markets: advertising, market activity, public relations. Sales department costs: sales staff salaries, travel expenses, customer hospitality. Drr costs: r & d staff salaries, purchase of technical equipment, experimental materials. Administrative personnel department costs: office rental, utilities, employee benefits, recruitment costs。

What? That's the advantage of this classification

It aligns the management of the enterprise's responsibility centres. With experience, budget control is an empty word without departmental cost analysis. When the marketing department complains about the poor quality of the marketing department's leads, you can withdraw the costs and output materials from both departments and use the facts rather than empty arguments. This would greatly improve management efficiency and make it possible for those who are in difficulty to be held accountable。

The macro-classification framework allows for a clear picture. But to solve the problem, we have to go down and detach critical costs in depth. This makes it more difficult for doctors to know which system the patient has, and then to examine it more closely. It's the first two

Perspective iii: marketing and management costs

The two above are macro perspectives, but the real expression of analytical power is the “deep dismantling” of key cost items. We take the most common “marketing costs” and “management costs”。

1. Dismantling marketing costs: more than just how much has been spent, but how hana

It makes no sense if you only record "50 million for marketing this month." you have to take it apart:

Do you know what i mean? The purpose of dismantling is to say, "if we are going to increase the marketing budget next year, which channel should we add 100,000?" if we don't do it, you can only feel it; if you do, you can make decisions with data。

2. Dismantling of management costs: identifying the costs of operating the company

Cost-controlled disaster areas, based on the fact that they are management costs that are seemingly frivolous, are often easily ignored。

A fixed cost: rent, for example, as long as the company is open, the money is basically spent。

Change cost b: for example, office supplies, how much to buy, which is related to the number of people or business。

C-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c-c。

Compressed space (change costs). What are the benefits of this dismantling? It makes you clear which money you can't save, which is the fixed cost, which money

So you know where to start when corporate business contraction requires a reduction in efficiency. The introduction of paperless office space, for example, is an action against changing costs。

Iii. Distinction between costs and costs

The core difference is that there is a direct and clear causal link between cost and income, and that costs and income are indirect and holistic。

Cost: is a direct expense incurred to produce a particular product or to provide a particular service. It has characteristics of objectability, belonging and direct correspondence。

Costs: in order to maintain the company as a whole for a certain period of time, it is difficult for you to know which of these items is specifically spent on which product, which is characterized by a period of time, overall consumption and indirect relevance。

Relative dimensions

Cost

Costs

Relationship to income

Direct, explicit causal link

Indirect, integral relationship

Definitions

Direct expenses incurred for the production of specific products or services

Expenditure incurred to maintain the company as a whole for a certain period of time (difficult to distinguish between specific products)

Core characteristics

Objectability, attribution, direct correspondence

Periodization, overall consumption, indirect relevance

For example, you'll see:

To make the whole company work. It's a furniture factory, the wood, screws, paints, and the wages of the workers on the water line to make a chair, which is the cost of the chair, which is how much it costs to make a chair; and the general manager's salary, the rental of the plant, the cost of advertising, the salary of the sales personnel, etc., for the purpose

So, we analyse the cost to price the product, to see whether the individual product is making money; the cost to see whether the overall operating expenses of the entire company are reasonable for a certain period of time, and the overall profitability。

Summary

Cost analysis, after all, is a rational thinking habit. It requires us to go beyond the easy action of spending money to look into the logic, purpose and effect behind it。

The power of this mindset is enormous: for an enterprise, it can direct its limited resources to the highest levels of output, avoiding confusion and driving healthy growth; and for an individual, this analytical logic applies equally to the management of your personal finances and career planning, giving you a clearer idea of your input and output。

With a few tables and numbers, you can see more clearly the full picture of the company's operations, and more constructive advice in the workplace, leading to the right and useful decision-making. That's why cost analysis is more important than that