Under the current tax administration act, a taxpayer can apply for administrative review of a tax dispute by providing a corresponding tax guarantee. In practice, however, tax guarantees are difficult to operate owing to the absence of inter-unit cooperation mechanisms and related procedural requirements. Among these, the issues of assurance of credit, valuation of property, preservation of property, evaluation costs of auctions, time limits are particularly problematic. In recent years, taxpayers have provided tax guarantees in the form of insurance letters from banks and had access to applications for administrative review。

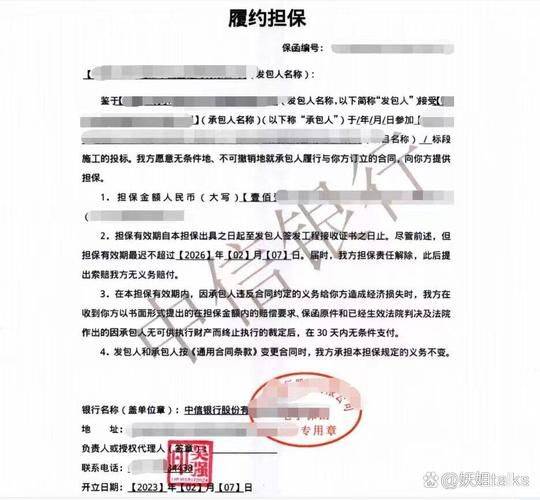

A letter-of-assurance business is a written undertaking by the guarantor bank to the beneficiary at the request of the applicant that the applicant fulfils a specific obligation. It is characterized by the substitution of bank credit for commercial credit, the resolution of mistrust between the parties in legal relations and the facilitation of the performance of contractual or legal obligations. In practice, the bond operation applies in the areas of goods, services, trade in technology, customs declarations of import and export of goods, and procedural preservation in proceedings. The procedures are simple and quick。

Before applying for administrative review, the specific procedure by which an enterprise carries out its tax guarantees by means of a bank guarantee is that the company makes a voluntary application to the bank, which scrutinizes its qualifications. If the conditions are met, the bank will act as guarantor for the payment of tax guarantees for the relevant taxes and demurrage payments and will issue a bond to the tax authorities. Tax authorities confirm tax guarantees. At the end of the review proceedings, the bank will pay the guaranteed amount in accordance with the notice of claim if the party has failed (by agreement) to meet its obligation to pay the relevant tax and late payment within a certain period of time after the decision on administrative review。

Tax guarantees in the form of bank bonds are relatively simple procedures in relation to mortgages and pledges, and taxpayers are not required to travel in search of guarantors; tax guarantees issued by banks are easy to confirm for tax authorities, and enforcement of taxes and demurrages will be more reliable by bank credit; and, for banks, this will also help to open up the bond business and increase the market share of the bond business。