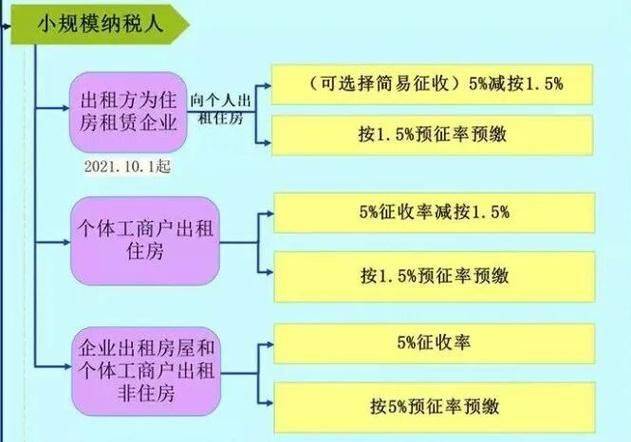

Question

What are the different provisions for individual rental and sub-rent housing in terms of combined collection of taxes and fees

Answer

Reference is made to the proclamation of the guangzhou city local tax administration on the adjustment of the tax policy on private rental housing in our city (no. 8 of 2016) which provides:

If the monthly rental income (excluding vat tax) is not up to 2000 yuan, the combined tax rate is 4 per cent; if the monthly rental income is more than 2000 yuan (including 2000 yuan), the combined tax rate is less than 30,000 yuan, or 6 per cent; if the monthly rental income is more than 30,000 yuan, the combined rate is 7. 9 per cent; and if the monthly rental income is more than 100,000 yuan, the combined tax rate is 8 per cent。

If the monthly rental income of a person rents a non-residential house does not reach 2000 yuan, the combined tax rate is 5 per cent; the combined tax rate is 8 per cent for a monthly rental income of more than 2000 yuan (including 2000 yuan) and less than 30,000 yuan (including 30,000 yuan); the combined tax rate is 13. 7 per cent for a monthly rental income of more than 30,000 yuan and under 100,000 yuan (including 100,000 yuan); and the combined tax rate is 14 per cent。

3. The combined rate of tax collection is 0 per cent if the monthly rental income of the individual sublet dwelling is less than $5,000; the combined rate of tax collection is 1 per cent if the monthly rental income is more than $5,000 (including $5,000) and less than $30,000 (including $30,000); the combined rate of tax collection is 2. 9 per cent if the monthly rental income is more than $30,000 and less than $100,000 (including $100,000); and the combined rate of tax collection is 3 per cent。

Iv. The combined rate of tax collection is 0 per cent if the monthly rental income of a person is less than $5,000 for a non-residential dwelling; 2 per cent for a monthly rental income of more than $5,000 (including $5,000) and less than $30,000 (including $30,000); 7. 7 per cent for a monthly rental income of more than $30,000 and $100,000 (including $100,000); and 8 per cent for a monthly rental income。

Membership is granted to:

2. Team growth fund

6. Direct interpretation of the new deal