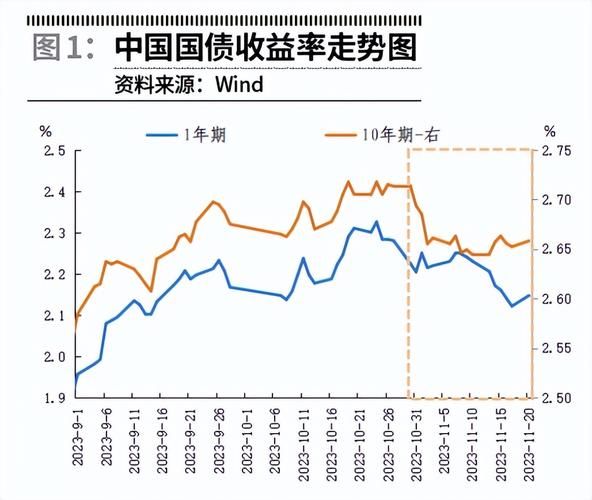

Last week, the rate of return on maturity national debt continued to rise on a full line, with 10 years of 3. 28 per cent and 10 years of a fall of 0. 24 per cent in the main bond. The market suffered a major setback on wednesday, when the largest decline in the stock of national debt reached 0. 45 per cent. Four weeks ago, five g5 futures rebounded in two consecutive trading days, and the rate of return on the g5 fell from the highest level of 3. 337 last week to 3. 299。

(the rate of return is inversely proportional to the price of the bonds, and part of the proceeds of the debt base is derived from the difference in the price of the bonds bought and sold. In general, the higher the price of the bonds and the lower the return on the national debt, the better for the investors in the debt base. Why is the debt market so stable? Since september, debt markets have continued to adjust, as the price of pigs has pushed up inflation expectations, market easing has failed many times, trade friction has eased the risk preference for increased risk, and next year's advance issuance of earmarked debt has raised concerns. On 15 october, the department of statistics released data that showed a 3 per cent increase in the national cpi (consumer price index) in september. This is a six-year break from the cpi to the "3" era. As a result, the debt market was “deep” and, in early october, the return on the 10-year national debt hovered at 3. 1 per cent and, by late october, had quickly surpassed 3. 2 per cent. The high-frequency data published by the ministry of commerce on the prices of agricultural products and pork have contributed to some inflationary expectations, leading to the collapse of the debt market. However, with the release of pmi data on 31 october, the pmi showed that the fundamentals were back on the bonds, that the bond market rebounded and that the price of the northern pigs fell on 10. 31,11. 01, which could also lead to a return to the debt market. China gold stated that pmi showed fundamentals to be in favour of bonds again, and that the value of the allocation had been highlighted by the current rebalancing of the debt market, each of which was an opportunity for stowage. As can be seen from the market performance of the second half of last week, the debt market, although still under pressure, is shrinking. So how's the rate of return going in the long run? In recent days, markets have been gradually digesting fast-paced debt-market adjustments, and how the future debt-markets will continue to grow at around 6 per cent of GDP, while short- and medium-term inflation will continue to be a central factor in the evolution of debt markets. Investment depends on medium- to long-term trends, so whether debt markets are worth configuring in the medium to long term. The five key elements affecting bond yields include fundamentals, financial aspects, policy aspects, emotional aspects, supply and demand aspects. The financial landscape has remained largely stable and has not been affected by factors such as taxation, and inter-bank market liquidity has remained relatively stable and has not changed significantly. The emotional situation, which was facilitated by the recent us-american trade frictions, the prospect of a first-stage agreement, and the prospect of an agreement in the u. K. Deutsche, led to an improvement in investor sentiment, an increase in risk preferences, and a small rebound in the stock market, with some repression of the bond market. On the supply and demand side, a major uncertainty in the near future is whether government-specific debt will be released early in the fourth quarter, which, if released early, will increase supply and put some pressure on market liquidity. Changes in mood and supply and demand have not been sufficient to challenge investors ' expectations, while changes in fundamentals and policies have led to some poor expectations and have been key factors in the restructuring of the current market. On the policy front, the market has stronger expectations of lower central bank interest rates, largely as a result of sustained interest-rate cuts in both developed and developing countries, represented by the united states, and into the cycle of lower interest rates, especially after our interest rate has been brought on track, with the market expecting lower central bank interest rates, in parallel with other countries, on the one hand, and the problems of weak demand, expensive corporate finance, and difficult financing, on the other. However, a slight over-market expectation is that central banks have not tended to reduce interest rates, which may be due to the instability of the existing lpr mechanism, the failure of the transmission mechanism to meet requirements, and the rush to reduce interest rates, which may not have worked well; and, secondly, the current critical period of macroeconomic regulation of real estate, which undoubtedly signals disruption, may further drive up housing prices. Of course, short-term failure to reduce interest rates also has inflationary constraints. On the basic side, the macroeconomic rate of growth continues to decline within expectations, with GDP booms affecting business performance and capital returns, all returning to GDP growth in the long run and bond yields as part of capital returns. In the light of japan’s south korean economic transition and its national debt rate, the return on national debt was limited at the beginning of the transition, but would decline significantly after the transition was completed. In terms of economic restructuring, the country is currently predominantly investment-driven, with capital-intensive characteristics, such as real estate, but investment is inefficient, debt dependence is high and there is a need for a smooth transition between leverage and economic growth, while future shifts in the driving forces of economic growth will lead to higher efficiency in capital utilization, especially a downward trend in debt capital demand, which will drive down bond yields. Overall, the bond market is under upward pressure, but 2020 is a critical year for a fully functioning society, with low growth rates that do not support excessive bond yields, limited margins of return, institutions' perception that the bond market has gone through this rotation, the value of bond allocation has been highlighted, and investors can consider the basis for long-term asset allocation at this time. Perhaps this is the time when the debt market is “the fear of greed”. The financiers' cash-for-profit debt, increased positioning currency, short-term deleveraging, lower risk, with non-negative gains accounting for 96. 19 per cent of the days, and the market shock of the last week, which has continued to maintain a daily non-negative return, with positive returns for the week, suitable for robust investors. The rate of return since the current year has been ranked first among the short- and middle-income countries. (source: fortune no. 2019-11-06 09:19)