To help you gain a clearer understanding of the tax-related policies for buying and selling housing, the new policy was updated in 2026, covering core taxes such as value added tax, deed tax, tax tax, etc., full dry load, and recommended reserve collection

Part 1

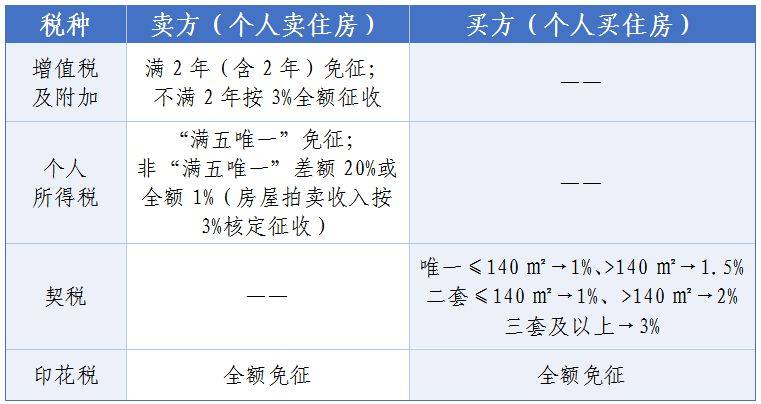

Seller's tax policy (selling is mandatory)

01

Value added tax: exemption for 2 years (including 2 years) and 3 per cent for less than 2 years

The law of the people's republic of china on value added tax has been in force since 1 january 2026. The latest vat rules are as follows:

Up to and including 2 years: vat exemption

2. Less than two years: full vat at 3 per cent

Taxable = ÷ (1+3%) x 3%

The number of years of house ownership is calculated on the basis of the time indicated in the certificate of title to the house or in the certificate of tax completion, in accordance with the principle of precedence。

02

Personal income tax: single exemption, refundable for purchase

There are two types of tax payments, which are conditional on the granting of relief or tax refund benefits for immediate needs and improved households:

1. Tax rules:

Up to five years and as the sole home of the family (one of five): exempt from personal income tax

Failure to meet the “sole five” requirement: personal income tax is calculated in two ways:

(a) income from the transfer of housing, net of the original value of the property, the amount of taxes paid in the transfer of housing and the balance of reasonable expenses, which is taxable, is subject to personal income tax “from the transfer of property”, at a rate of 20 per cent

(b) tax authorities may impose an approved tax on taxpayers who do not provide complete and accurate proof of the original value of the house and are unable to correctly calculate the original value of the house and the amount taxable, i. E. An approved levy of 1 per cent of the income from the transfer of the house (a 3 per cent of the income from the auction)

An individual may not be authorized to collect a gifted, inherited immovable property when it will be sold abroad, and it must be collected in strict accordance with the applicable tax rate of 20 per cent, as provided for in the tax law。

2. Tax rebates on replacement housing (extended until 31 december 2027):

Taxpayers who repurchase their homes in the same city within one year after the sale of their own homes are entitled to the required reimbursement of personal income tax。

Part 2

Buyer's tax policy (buyer's house)

01 deeds: first set of two-slotting benefits, lower rate up to 140 m2

Currently, shanghai fully applies the slotting rate for family housing tax, which is based on the transaction price of houses without vat:

Tax rules:

Family housing

(a) area 140 m2: a tax amounting to 1 per cent

Area >140m2: taxes reduced by 1. 5%。

Second home for families

(a) area 140 m2: a tax amounting to 1 per cent, consistent with the initial rate

Area >140m2: taxes reduced by 2 per cent。

Third home and above

Taxes are levied at 3 per cent。

02 property tax

Households of residents of the municipality who have newly acquired housing in the municipality and belong to the second and more units of the household of the resident (including second-hand stock and new commodity houses) and non-resident families of the municipality shall pay property tax in accordance with the regulations。

Read a list of the taxes and fees of the parties to the real estate deal

Particular attention is paid to the fact that the tax authorities have the power to approve the basis of taxation when the transaction price is clearly low and unjustified。

The “only five” conditions establish that: the taxpayer is required to sign a notice of commitment to the tax certificate, which commits him and his family members to the relevant information, and authorizes the tax authorities to obtain information on the status of his or her marriage and on his or her family name from the civil administration, the home administration, etc., and to verify the marriage information obtained by the tax authorities through the above-mentioned channels, as well as information on his or her family name and family name。

Policy basis

1. Bulletin of the ministry of finance of the general directorate of taxes on the value-added tax policy for personal sales of housing (ministry of finance of the general directorate of taxes, 2025, no. 17)

2. Circular of the general state tax administration on matters relating to the collection of personal income tax on the transfer of personal housing (state tax) [2006] no. 108)

3. Circular of the ministry of housing, urban and rural construction on the continuation of the implementation of the individual income tax policy in support of residential renewal (ministry of finance, general directorate of taxation, ministry of housing, urban and rural construction, 2026, no. 3)

4. Ministry of finance, general directorate of taxation, ministry of housing, urban and rural construction, bulletin on tax policy for the smooth and healthy development of the real estate market (ministry of finance, general directorate of taxation, ministry of housing, urban and rural construction, 2024, no. 16)

5. Circular of the shanghai city people's government on the publication of the shanghai city interim scheme for the piloting of a housing tax on selected individual housings (shanghai city) no. 3)

Presented by choi win-chi wang

Production: jung min-woo