I. Changes in new lease guidelines

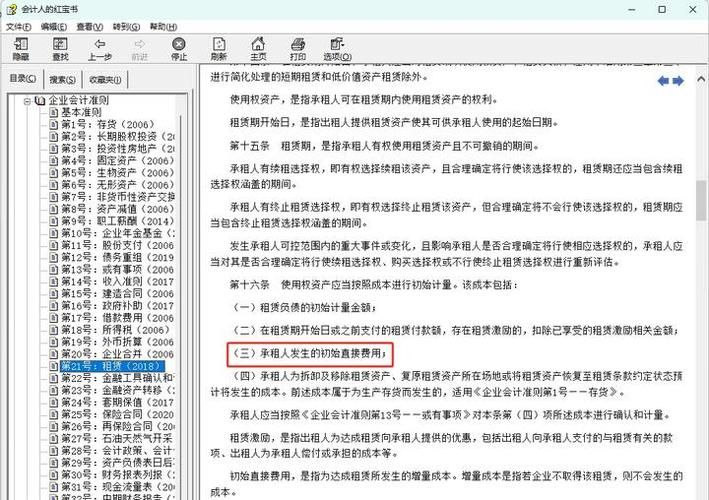

Ministry of finance revised and issued enterprise accounting standard 21 - leases (2018) in 2018 no. 35), fully implemented with effect from 1 january 2021 in all enterprises that implement eas. The most significant change in the new standards was the subversive adjustment of the lessee's accounting treatment: with the exception of short-term leases (not exceeding 12 months of lease) and low-value asset leases (with a lower full-time value of a single asset, usually less than $40,000), which may be treated in a simplified manner, the lessee no longer distinguishes between operating leases and financial leases, recognizing rights-of-occupancy assets and lease liabilities。

This “single accounting model” is designed essentially to recognize the right to use an asset leased by an enterprise as an asset in a schedule, and the future rental obligation to be paid as a liability that more accurately reflects the asset liability position and financial risk of the enterprise. Specifically:

• right-of-use assets: represents the enterprise's legitimate right to use leased assets over the lease period, with an entry value of the present value of future lease payments plus initial direct costs, restoration costs, etc., less lease incentives。

• lease liability: an initial measure based on the present value of outstanding lease payments at the beginning of the lease period, the difference from the total amount of future rentals payable is charged to “unrecognized financing costs” and amortized over the lease period at actual interest rates。

• subsequent measurement: right-of-use assets are depreciated by reference to the fixed asset guidelines, usually amortized over the lease period using a straight-line method; unrecognized financing costs are amortized on the basis of actual interest rates and are charged separately to the cost of current profits and losses or related assets。

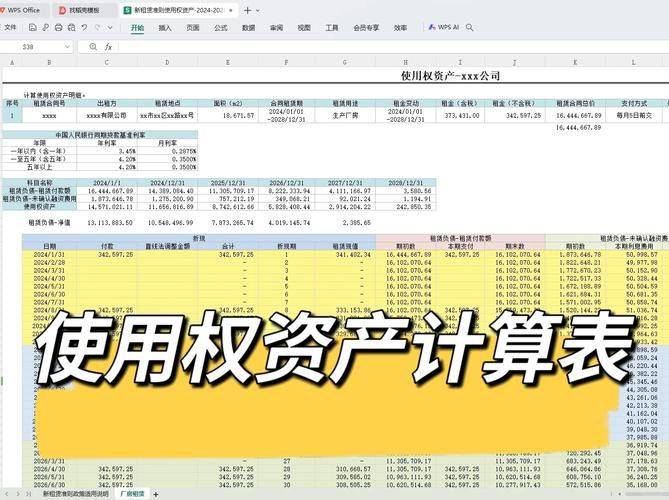

Typical examples of initial confirmation

An enterprise rents office accommodation for a six-year lease period and pays an annual rent of $150,000 at the end of the year at an interest rate of 6 per cent. Calculated through the present value of the annuity:

• right-of-use assets = $150,000 x (p/a, 6 per cent, 6) = $737. 6 million

• total future rental = 15 x 6 = $0. 9 million

• unrecognized financing costs = 90-73. 76 = $16. 24 million

The transactions are as follows:

Rules governing tax and accounting treatment

The concept of “right-of-use assets” is not currently introduced in our tax system, and the processing of income tax in rental operations continues to be governed by the original rules, based in particular on article 47 of the regulations implementing the income tax act:

1. Operating lease to a fixed asset: lease cost expenditure incurred, evenly deducted from the lease term

2. Financial lease lease to fixed assets: the portion of lease cost incurred that is required to constitute the value of the fixed asset leased to finance shall be charged as depreciation and deducted in instalments。

This logic of treatment, which is clearly at variance with the new norms, is the core source of the difference between the right-of-use asset tax:

Process dimensions

Accounting treatment rules

Rules governing tax treatment

Asset recognition

Right-of-use assets recognized and depreciated

Right-of-occupancy assets not recognized, no depreciation deduction calibre

Cost recognition

Depreciation of right-of-use assets + amortization of unrecognized financing costs

Equal deduction based on actual rental payments

Measurement basis

Accounting based on the present value of future rentals

Based on actual rental expenditure incurred

Following the above-mentioned case of rental of office premises: the current value logic of tax treatment of unacknowledged right-of-occupancy assets allows only $150,000 in real rents paid annually to be deducted prior to tax, regardless of depreciation and amortization of financing costs。

Iii. Structure and dynamics of tax differences

(i) core manifestations of differences

Accounting gains and losses are accounted for annually in the amount of “depreciation of right-of-use assets plus amortization of unrecognized financing costs”, while taxes allow only the deduction of rents actually paid, the difference being the difference between the taxes for the year:

• pre-lease period: higher amortization of unrecognized financing costs, accounting recognition that the total costs are usually greater than the rents allowed for tax deductions, resulting in deductible temporary differences, requiring an increase in taxable income

• later in the lease period: the unrecognized financing costs are reduced each year, the total accounting recognized costs are lower than tax deductions, the differences are gradually reversed and the taxable proceeds are reduced

• expiration of the lease: accumulated accounting costs are equal to the amount of the accumulated tax deduction, with the difference completely zero。

(ii) exercise cases: calculation and adjustment of variances

Case background: company a rents core production lines for eight years, pays $600,000 annually at the end of the year, and the company borrows at an incremental 7 per cent interest rate, with no residual value。

1. Initial recognition: right-of-use assets = 60 x (p/a, 7 per cent, 8) = $3. 58. 28 million, unrecognized financing costs = 480-358. 28 = $1,217. 2 million

2. Follow-up measure: annual depreciation = 358. 28 ÷ 8 ≈ 447. 9 million, first year amortization of unrecognized financing costs = 358. 28 x 7 per cent = 250. 8 million

Total first year accounting costs = 44. 79 + 25. 08 = $6,987 million, tax deduction allowed for rental costs of $600,000, variance of $987 million

First-year tax adjustment: if the accounting profit for the year is 1. 8 million yuan, the amount of taxable income will have to be increased by 987 million yuan, and the adjusted taxable income = 180+9. 87 = 1898. 7 million yuan。

Iv. Practising norms and filing forms for tax adjustments

(i) adjustment of basic principles

In carrying out an enterprise's income tax settlement, an enterprise is required to adjust its accounting profits to taxable income of the tax code, with the core being to adjust the two categories of differences separately:

1. Discrepancies in the depreciation of right-of-use assets: the difference between an accounting charge of depreciation and a tax deduction of depreciation (0 under an operating lease)

2. Unrecognized amortized differences in financing costs: the difference between the amortized amounts of accounting charged to financial costs and the taxable interest expenditures (0 under operating leases)。

(ii) guidelines for filing forms

In accordance with the current rules for the annual tax returns of enterprises on income tax, the following requirements are specified:

1. Depreciation adjustment for right-of-use assets: enter the corresponding column for "iv, long-term amortized costs" "(v) other" in the schedule to depreciation, amortization and tax adjustments (a10580). This is because the portion is leased and the accounting recognition of "right-of-use assets" is considered to be tax "long-term to-amortized expenses"。

Unrecognised amortization adjustment for financing costs: the accounting amount is reported in the schedule of tax adjustment projects (a10500), line 35 “iv, other” or a105000, line 30 (xvii) other, the current year amortization amount, the tax amount is zero and the balance tax is increased。

References

Enterprise accounting standard 21 — leases (customs (2018) number 35)

2. Regulations implementing the income tax act for enterprises

3. Information on filling in the bulletin of the national tax administration on matters relating to the annual tax returns of enterprises

4. Total analysis of the accounting and tax treatment of right-of-occupancy assets under the new lease standards (2026)