I'm chen xiao, who brings you up to date every day

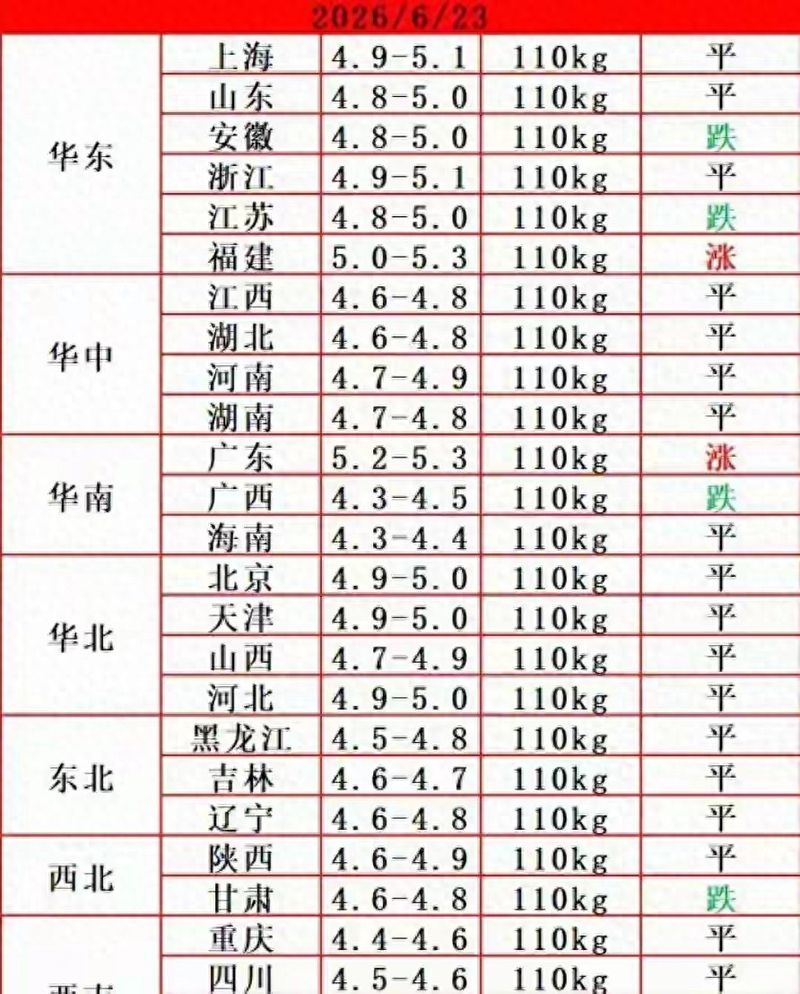

On 26 june, there was a marked split in the current situation in the pig industry throughout the country, completely breaking the expectations of raising prices after lunch. The national average price of the main pig is between $4. 7 and $5 per pound, with a small fall in the prices of pigs in china, north china and china's main production areas, with only a small rise in the demand for short-term transfers in the north-east and a cold-hot dichotomy in the region. A number of farmers and traders had hoped for a sustained recovery in their midday preparations and had been hoarding pigs for higher prices, and the market had now fully cashed out of a steady increase and had returned to a fragile shock pattern. This document is based on the monitoring of data by the ministry of agriculture and rural development, the purchase of bids for slaughtering enterprises, the production inventory, the objective dismantling of production capacity data, the identification of short-term shocks and medium- and long-term trends, the development of a three-pronged approach to the business of family breeders, scale farms and wholesalers of pigs, the non-subjective prediction of a sharp rise and fall, and an objective analysis of the underlying causes of the expected collapse of the current boom。

The difference between supply and demand behind regional differentiation is illustrated by the real changes in national pig prices today. According to the country's proposal for 26 priority provinces, the purchase price of raw pigs in more than 20 provinces has been flat or slightly lower, with a reduction of 0. 05 to 0. 12 yuan per pound per pound in the main areas of china's production in shandong, henan and hebei, and a clear willingness to collect pigs in slaughter plants; the two broad and two lakes in the south have been affected by the continued high temperature of plum rain, the speed of the movement of pork has slowed and the prices of the raw pigs have weakened simultaneously; only a small increase has occurred in the three provinces in the north-east, mainly in the concentration of slaughtering enterprises and the short-term digestion of local pigs, resulting in small price increases。

This partial increase is difficult to boost nationwide, owing to the fact that the price increases in the northeast are short-term supply-demand mismatches and do not alter the overall supply-to-demand environment in the country. The national pig production column has remained high, with large fats concentrated in the previous two-consumer hoardings, and the market is well populated, and single-region demand is not enough to reverse overall weakness. Many farmers saw price increases in individual areas, confirming that the national situation would improve at the same time, ignoring the overall data on production capacity, stock and consumption, and being a central incentive for the expected collapse of the increase。

The next four layers of core logic, which explains why the expected increase after noon has not materialized, come from open industry data without subjective speculation。

First, the midday provision is a one-time short-term requirement, and demand drops directly after the holiday. In late may and early june, merchants, cuisine-processing plants and catering outlets concentrated on the preparation of lunch boxes, which increased the volume of pork purchases on a phased basis, and briefly pushed a small rebound in the price of pigs, while many farmers seized the space for sale and looked forward to continued high levels of activity. At the end of the lunch break, large quantities of procurement by processing companies were stopped, school canteens continued their summer holidays, stability was just about to disappear, high-temperature weather diets were defunct, daily consumption of pork shrunk, demand support was lost and the movement lost momentum. At the same time, there is a high stock of frozen goods in the market, and the storage of pork in cold storage continues to divert the demand for fresh meat, and slaughtering plants do not need to purchase raw pigs at high prices and at low prices。

Secondly, the supply of raw pigs in the market remains relaxed, with the concentration of pre-pressure pigs and persistent supply pressures. In the first quarter of this year, a large number of out-of-barrel pigs were produced by june, adding pre-farmers to their lineage, late-posting, second-fertilization accumulations of large-scale fat pigs, and concentrated at noon. According to official data, the country was able to keep a stock of 3. 904 million sows at the end of march. Compared to the 37. 5 million reasonable holdings, the total capacity redundancy is still 1. 54 million, the total amount of short-term pig production is unlikely to contract significantly, and the supply easing directly limits the price space. Using the beginning-of-month run-off tempo of high prices and end-of-month concentration, the concentration-out at the end of each month will further press off spot prices, exacerbating short-term weakness。

Third, farming losses have increased, but the farmers have not eliminated the sows on a large scale and lacked the incentive to take a proactive approach. At present, there is a loss of nearly 270 dollars per head of pig from a self-employed farmer, more than 230 dollars per pig from a foreign purchaser, and the industry as a whole is in a deep loss zone. However, there is sufficient cash flow from domestic-scale pig farms, and even long-term losses do not result in the bulk phase-out of the basic production of pigs, with only a small number of large-scale and small-scale farms phasing out low-yielding old pigs, and the slow pace at which production can decomposed and the rapid reduction of the supply of pigs in the market. As long as the market is full of pigs, the farmer, even if he loses, will be able to cash out normally, without uniform conditions for bottom-up, and without a bottom-up support。

Fourth, policy regulation continues to be applied to the ground, with tight controls on the fences and secondary fertility, to curb large price fluctuations. Recently, the ministry of agriculture and rural development organized a seminar on the regulation of pig production capacity, which called on the major farming enterprises to control the weights they weigh off, eliminate the accumulation of super-fatous pigs, regulate second-generation practices, conduct simultaneous monitoring of the circulation and slaughtering of pigs in various areas, and, if the price of pigs rises too fast, initiate the freezing of pork, increase market supplies, lock up large-scale increases in space at the policy level, making it very difficult to sustain unilateral movements。

The central concern of farmers now is the failure of short-term growth expectations and the lack of a year-long recovery. (c) distinguishing between short-, medium- and long-term objective measurements of three dimensions, distinguishing between the grinding of a shock and the turning point of the trend。

Short-term (late june to full july): low-level concussion, low-level growth is difficult to sustain and the expected surge will not occur in the short term. On the one hand, high summer temperatures continued, pork consumption reached its lowest level throughout the year, and end-to-end shipments were weak; on the other hand, the backlog of second-born pigs in the previous period continued to be out of the pipeline, market supply pressures remained unabated and high stocks of frozen goods continued to suppress spot prices. Even small price increases in local areas are short-term fluctuations of one or two days that are not sustainable and are at this stage in the standard grinding phase。

Mid-term (august-september): the first round of rehabilitation windows will be followed by a marginal improvement in supply and demand patterns. In accordance with the conductive cycle for the production of pigs, the production capacity of able-bodied pigs, which began slowly to decomposed in the fourth quarter of 2025, will gradually be reflected in the volume of commercial pigs coming out of the field in august, with a small contraction in the total volume of imported pigs in the market; at the end of august, the major food-processing plants launched mid-fall cakes, ready food products, seasonal demand increases will digest market stocks, and the price of pigs will emerge from a small round of warming, but the increase will be limited and it will be difficult to rebound significantly。

Long-term (fourth quarter, october-december): best-line window for the year, with demand-side resonance driving a marked recovery in prices. In mid-autumn and national days, the traditional consumption season of pickles in autumn and winter, the highest demand for pork is concentrated throughout the year in four quarters; after three quarters of continuous loss of capacity, the excess capacity of able-bodied pigs has increased, the volume of pig production has continued to decline, and the demand for supply has increased significantly, creating a trend pattern of repair, which is also the most suitable time this year。

A brief summary: short-term rising expectations did not materialize, june and july were dominated by low-level shocks, with no need for fast-growing expectations; the real heating window was high throughout the year in late august, with four quarters of the year, which was a stale rebound, rather than a continuous fall throughout the year。

In the context of the current market situation, three categories of practitioners offer direct landing practical programmes that combine the day-to-day operation of the family, the size of the business and the wholesaler。

Category i: rural farms, small- and medium-sized farms, with boars and fat pigs in their hands

1. To refrain from continuing to press the bar, while taking advantage of the current small quotes, to slow the increase in the weight of the high-temperature raw pig, and to keep the cost of fodder under constant consumption, and to avoid the risk of falling prices resulting from the subsequent concentration column losses

2. Standard 110 to 120 kg of pigworks are balanced, not a one-time total clean-up, and no price increases are charged, with a fixed weekly portion of the column, smoothing the working capital and avoiding a deep loss

3. Stop buying out of pigs second-generation fertilizer, at this stage of the supply and demand cycle, with limited space for subsequent increases and a high risk of loss in the farming of pigs

4. To phase out in batches five or more low-yield older pigs, to cooperate proactively with the decompositation of production capacity, to reduce the supply of later-stage pigs and to ease the pressure on their long-term operations。

Category ii: head size chemical farming enterprises, wholesale trade in professional pigs business

1. Adjusting the pace of the columns to balance the monthly entries and not concentrating at the end of the month to press down spot prices and reduce large fluctuations in market prices

2. Control of the flow of frozen stocks, taking advantage of short-term, small rebounds and modest exits, and reducing storage costs in cold storage to avoid subsequent price failures that could lead to the expected loss of inventory

3. There is no trendive rise in the short-term market, with large-scale hoarding taking over of liquidity and risk outweighing returns。

Category iii: ordinary residents, daily procurement of pork

1. At this stage, the low price of raw pigs is transmitted to the retail end of the year, and retail prices of pork are in the low range of the year, and can be purchased on a day-to-day basis, without large-scale hoarding of meat, and high-temperature storage is susceptible to deterioration

2. In the short term, there has been no significant price increase for pork, and no early accumulation of meat is required until the four-quarters of the consumption season are in full swing。

Turning to the logic behind this rotation, the whole new pig cycle runs in a clear difference from previous years, so that the wind can be avoided. In the lower stages of the previous cycling of pigs, with weak financial resources, the bulk phase-out of pigs after sustained losses, rapid production of capacity and short-term reversals; now the size of the domestic pig market has increased significantly, with head-run firms accounting for more than half of the market share, large firms having a strong capacity to resist losses, and the evaporation rhythm has been stretched, the cycle of bottom shocks has been longer than in the past, the surge and fall have largely disappeared, with inter-district shocks and small seasonal repairs taking the lead throughout the year, making it difficult to achieve a unilateral surge。

A number of farmers are now at a polarized mental level, with some suffering from frustration due to rising prices during the afternoon, panic and panic, while others are still holding onto the fence and waiting for a substantial increase in prices. There are clear disadvantages in both operations, panic sales concentrate losses at a low level, blind pressure columns continue to deplete feed funds, loss margins are increased, and balancing out and adjusting the storage column structure is the sound choice。

An objective view of the failure of the expectations of this increase is not that the market has no chance at all, but that the majority has miscalculated the short-term supply and demand tempo and seen the short-term rebound of the festival as a reversal of the trend. The small increase in the availability of midday goods is not sustainable in itself, and the combination of the three-fold factors of easing supply, consumption and freezing stocks is bound to be difficult to strengthen in the short term. It is not necessary that short-term shocks reverse the whole year, that supply and demand patterns gradually improve after august, that the four-quarters boom lead to clear heating windows, and that farmers rationalize the pace of the bars, so that the current grounding phase can be smoothed out。

Topical discussion

1. How much are the prices of pigs in your area now and have there been any recent increases or declines

2. At this stage, there are pig farmers in your hands, and do you think that the batch should go out or wait for august

The sharing of local practices and farming plans in the comment area was welcomed, and it was felt that the agricultural industry's dry products were useful and could be of some interest in continuously updating the factual interpretation of pig, corn and eggs。