I. Overall overview of the national pig market today

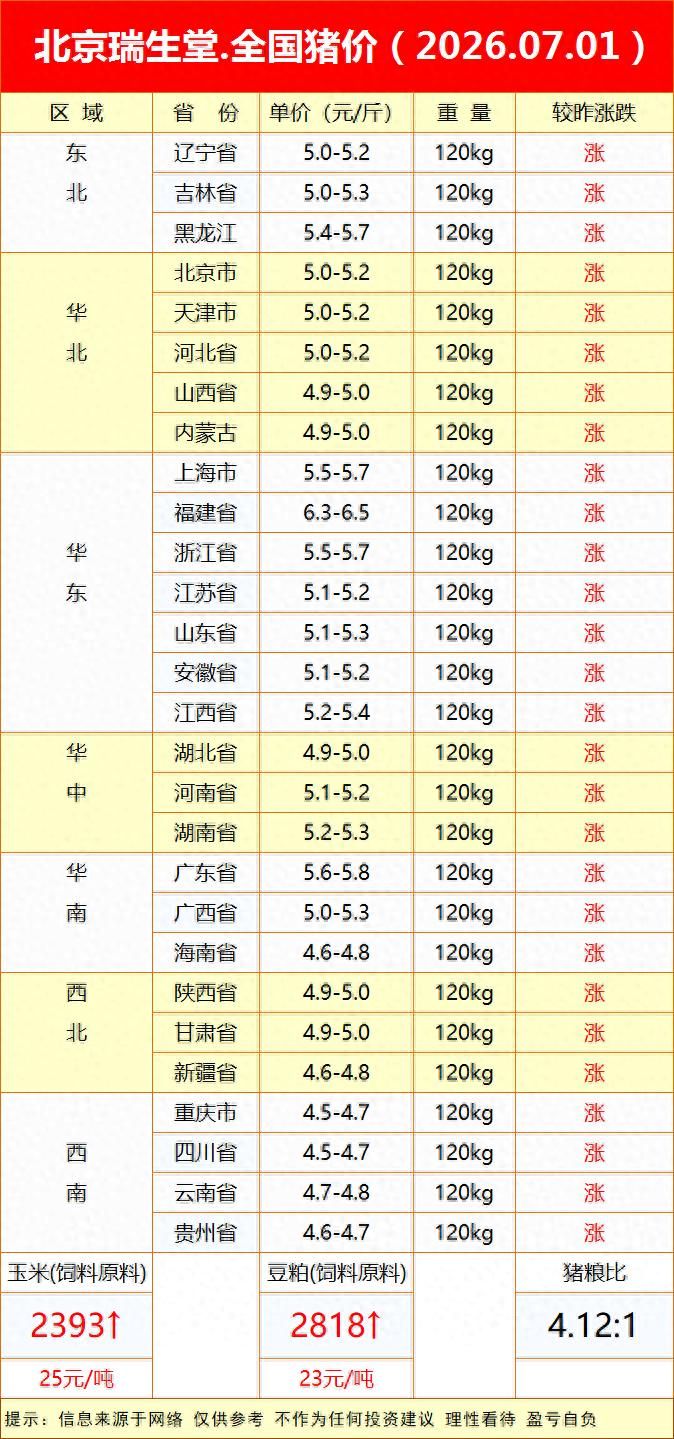

According to the latest national pig price figures of 1 july, the 120-kg standard for pig prices in the provinces and cities of the country are all red, with no regional price falling, covering the seven main sectors of the north-east, north-east, east-west, central, south-west, north-west and south-west, creating a market pattern of synchronized price increases across the country, with the current round of pig prices warming to a wide extent and regional connectivity。

The harmonized benchmark for this offer is 120 kg, which is expressed in dollar/snock, and the regional price differentials are mainly influenced by local consumer demand, liquidity adjustment, regional farming column structure, with clear rankings at higher and lower prices, and the overall market view of rising sentiment continues to warm。

Ii. Sub-regional price interpretation of raw pigs

(i) north-east region: lower floor prices are rising steadily and the whole line is rising

Liaoning pig offers $5. 0-5. 2 per pound, jilin $5. 0-5. 3 per pound, heilongjiang 5. 4-5. 7 per pound, rising simultaneously in the three provinces. The north-east, as a traditional raw pig, is out of the province, with demand for outward circulation continuing to support local pig prices, with the heilong river with a regional supply-and-demand balance at the highest level in the north-east region。

(ii) north china: main price levels are stable and small upscale

In beijing, tianjin and hebei, a flat offer of $5. 0-5. 2 per pound; in shanxi and inner mongolia, 4. 9-5. 0 per pound is on the rise. The demand for local fresh pork terminals in north china has been flat, the number of acquisitions by slaughtering enterprises has risen slightly, and the price of the farm has gone up simultaneously。

(iii) east china: high national prices, sufficient energy for growth

China has the highest cost of pigs in the country, and the provincial prices have risen simultaneously:

Shanghai, zhejiang, 5. 5-5. 7 yuan per pound; fujian, 6. 3-6. 5 yuan per pound, the highest price province for pigs in the country; jiangsu, anhui, 5. 1-5. 2 yuan per pound; shandong, 5. 1-5. 3 yuan per pound; jiangxi, 5. 2-5. 4 yuan per pound。

East china is densely populated, with a large consumption of fresh meat, limited subsistence of locally produced pigs and long-standing cross-regional transport demand, which supports the long-term nationalization of regional pig prices。

(iv) central china: moderate price bands with parallel warming

Hubei 4. 9-5. 0 per pound, henan 5. 1-5. 2 per pound, hunan 5. 2-5. 3 per pound, all three provinces increased their prices. China is in the middle of the north-south movement of pigs, and the north-south two-way transport dynamic market has led to a steady upturn in local exit prices。

(v) south china: significant regional price differentials, overall upwards

Guangdong 5. 6-$5. 8 per pound; guangxi 5. 0-$5. 3 per pound; and hainan 4. 6-$4. 8 per pound, all three lines rise. The market for consumption in guangdong is strong, and the price of pigs is stable at a high level in south china; hainan is subject to the cost of geographical circulation and has a relatively low base price。

(vi) northwest territories: low prices, synchronized increases

The prices of the zhuxi and gansu pigs were 4. 9-5. 0 per pound and those of xinjiang 4. 6-4. 8 per pound, all rising. Northwestern farming is fragmented, local consumption capacity is limited, there are limited outlets for the export of raw pigs, and overall prices are below the national average。

(vii) south-west: national floor concentration area, synchronized warming

Chongqing, sichuan 4. 5-4. 7 yuan per pound, guizhou 4. 6-4. 7 yuan per pound, yunnan 4. 7-4. 8 yuan per pound, and four provinces and cities with full-line price increases. In the south-west, where the farming base is large and the production of pigs is well supplied, it is the lowest-priced sector in the country, but during the course of this boom, it is also synchronized with the quotations that follow the country's general situation。

Iii. Cost of feedstock feed versus pig food reference

1. Cornline: the prevailing price of maize for feed is $2393/t, an increase of $25/t

Bean bean bean bean bean bean bean bean bean bean priced $2818/t, an increase of $23/t

The simultaneous small price increases for the two core feed raw materials imply a small increase in the cost of feed breeding for pig farming, which puts some pressure on the cost side of farming。

3. The pig grain ratio is 4. 12:1: the pig grain ratio intuitively reflects the balance of earnings and losses in pig farming. Under the current margin level, combined with the price of fielding, most ordinary farmers continue to be under pressure to operate, with small increases mitigating cost pressures, which have not yet completely reversed their profitability。

Iv. Multiplicity of factors influencing current market developments

Demand for final consumption heating-led acquisitions

The recent gradual improvement in the demand for fresh pork end-of-markets, the increase in the availability of goods for merchants, agricultural markets and catering outlets, the initiative of slaughtering processing enterprises to raise prices for pigs and the modest increase in bargaining power in farm farms have contributed to a large-scale increase in prices nationwide。

2. Regional boar circulation is active

There are significant regional price differentials for pigs, the spread of pigs in low-priced areas across regions to higher-priced consumer provinces, increased market flows, and the creation of a whole-of-a-kind market for pigs, leading to synchronized increases and increases in the regions, leading to a nationwide surge。

3. Minor adjustments to the outlier rhythm

Some farmers have a watch-and-see mentality, slowing the concentration of the bar, a small contraction in the short-term pig supply in the market, a folding of the supply requirements of slaughtering enterprises, and short-term changes in supply and demand that directly drive out-of-bar prices。

4. High feed costs to suppress profit margins

The prices of the two main feedstocks, maize and bean bean bean, have been rising simultaneously, and the cost of raising feed has continued to rise. Even though the price of pig-breeding has risen slightly and the real profitability of farmers has increased only marginally, the cost pressure remains a real problem at this stage。

V. Follow-up market rationality outlook

In the short term, the rise in national pig production is expected to sustain a small upswing, but the increase is regionalized: more resilient in consumer regions such as east china; and relatively limited scope for rising in low-cost areas in the south-west and north-west。

Long-term trends continue to depend on three core variables: one is the continuity of final pork consumption; the second is the total stock of raw pigs in the country as a whole; and the third is price fluctuations for raw materials such as maize and beans。

In the case of farmers, it is recommended that short-term price increases be viewed rationally, and that blindly concentrated columns or heavy railings be avoided, and that the rhythm of the columns be properly planned, taking into account the cost of raising themselves, the size of the columns; that day-to-day stock-raising management be managed in such a way as to deplete the controlled feed, and that the cost pressures on price increases for raw materials be dealt with in such a way as to smoothly respond to cyclical fluctuations in market prices。

Texttips

The data are derived from industry public offers, real-time dynamic adjustments of market prices, which are used only as reference points for industry exchanges, and do not constitute any farming, trading or investment proposals, and farming requires the self-consensual judgement of the operator。