Ladies and gentlemen, today we're talking about a real money-saving business. From june 1st, 2026, we've been paying a fixed price of $950 for more than a decade, and we're officially out of the stage

In the past, whether you were an old driver in a 10-year accident or a freshman who shaved several times a year, six cars under the age of six paid $950 at a price for a good or bad driver, and many old drivers threw up “the rules-abiding people are the losers”. It's not the same now. (no. 1) since june 1, a new floating mechanism has been implemented throughout the country to save $475 for safe driving, raising the maximum risk to $1,900, a fourfold difference

Today, the new rules are told in plain language, teaching people how to calculate premiums, how to avoid pits, how to take discounts, suggesting something to celebrate the collection, and using it when renewing the insurance。

Eat the pill first: 3 cores are the same. Don't panic

Many people are nervous when they listen to “reforms” and are afraid of rising prices and reducing their water security

1. The basic premium remains unchanged: for the first year, the following six domestic cars (cars, suvs, new energy sources) are again $950; for 6-9 domestic cars, $1,100; for the ordinary two-wheeled motorcycles, $120; for the non-operational truck, $1,200, up to 2 tons; and for the national unity, insurance companies cannot raise the price privately。

2. Increase in the level of guarantees: the total amount of compensation payable has been raised from 200,000 to 222,000, of which 200,000 are for death and disability, 20,000 for medical expenses and 2,000 for loss of property; the total amount of no liability has been increased at the same time and is more secure。

3. Compulsory insurance is the same: insurance is compulsory, or is it necessary to go on the road or to conduct an annual inspection; failure to buy a road is subject to arrest, double the premium, and the process does not have to be readapted as before。

Core change: a direct link between premiums and driving behaviour

The key part of the new rule is to break the one-size-fits-all and introduce rewards and penalties, with the final premium = base premium x floating factor, linked only to three things and not to the price, brand, age of the car:

1. Number of cases where liability has been incurred (core): only accidents for which the primary/full responsibility is attached are counted; accidents for which the other party is responsible are not counted, even if the settlement is made, without prejudice to the preference。

2. Serious traffic offences (minor): driving intoxicated, driving intoxicated, hit-and-run, speeding by more than 50 per cent, accounting for 12 points, etc., directly pushes up premiums。

3. Regional risk factors: the risk ratings vary slightly from one region to another, but the national uniform rules are not miscalculated。

How do you save a good driver? A watch knows how to save money

In the case of the six most common vehicles (950 basic premiums), the national uniform no-compensation benefit factor is used to calculate the amount of savings directly:

Discontinuation of life without liability, margin of preference

First year (new vehicle) 1. 0,950 0

1 year 0. 9 855 95

2 years 0. 8 760 190

3 years and above 0. 5 475 475 (half of province)

To give a real example, my neighbor zhang has been driving for eight years, has not had a responsible accident for three years, has paid only $475 last year, half of the initial year; and our colleague li has made three minor scratches this year, which has gone up to $1425 this year and spent $475 more a year。

Who's gonna raise the price? Don't touch them

There are two main categories of premium rises, which are easily ignored “mine-throwing”:

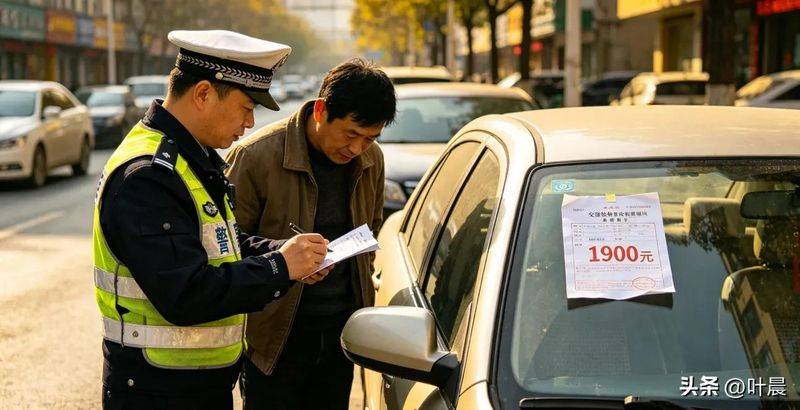

1. There was a high risk of liability: one incident in the previous year, with a premium of $950; two increases to $1140; three 1425; four 1662. 5; and five and above directly to $1900 (cap)。

2. Serious violations of the law: drunk driving, drunk driving, hit-and-run, speeding at more than 50 per cent, driving at a different rate than a car-a-car, etc., are directly added to the premium, not only by withholding points, but also by doubling the premium。

A special reminder: many of the drivers are gonna scrape their little scratches, and they don't think it's a risk if they don't go. However, if he leaves, even if he pays $300, he is liable for a single liability and the next year's premium is restored to $950。

Continue to ensure that the three details are not ignored

1. Time of renewal: renewal 30 days before expiry, implementation of old insurance policies effective before 1 june, automatic replacement of new rules with maturity renewals, without care。

2. Requiring records: prior to renewal of the insurance, the insurance company app, the offline point, or the telephone call for customer service may be made to check their own liability insurance records and serious violations and confirm the correct reinsurance。

3. Choice of formal channels: the network of insurance companies, apps, offline sites, and 12123 interfaces are insured, and no stranger intermediaries are approached to avoid leaking information or excessive charges。

At the end: safe driving is saving money

The essence of this risk-sharing reform is that it “rewards safe driving and pays more for high risks”. For our ordinary car owners, it is possible to save not only a large amount of insurance but also more solid security, provided that the rules are followed, the rules are not violated and the risks are minimal。

From 2006 onwards, the price of “big pot” for more than a decade has been optimized, which is both fair to safe drivers and a constraint on traffic violations. In the future, our driving behaviour is directly linked to the cost of travelling, and safe driving is not just about protecting ourselves and others, but about saving ourselves。

You haven't had an accident in years? How much is it gonna cost this year? It could be shared in the comment area, helping more drivers to clear premiums and save money from pits。

Compliance waiver: this document is based on the gold regulations issued jointly by the three departments on 30 march 2026 [2026] it is interpreted as policy guidance only and does not constitute a recommendation for insurance coverage. Specific premiums are systematically accounted for by insurance companies and regional rules are based on local regulatory requirements。