Attention all drivers! From june 1st, 2026, the biggest reform in 16 years! The fixed price of less than $950 for six cars, which has been in operation for many years, has become history, and the new system of prizes and penalties for bad and bad floating has been implemented uniformly throughout the country. Good and disciplined drivers receive a minimum discount of $475 in half, and the cost of insurance for the owner of the vehicle, who is exposed to frequent and serious offences, rises directly to $1,900, a full fourfold gap. It's not a price increase, it's a link between the premium and the driving behavior, and today we'll put the new rules in plain language, teach you how to save money, avoid pits, and don't wait to regret it

I. Eat three heart pills first: the three cores are unchanged, priceless and waterless

Many of the drivers panic as soon as they hear about the new rules, fearing higher prices and less security. According to the regulations of the general state financial monitoring authority, the ministry of public security and the ministry of transport and communications (2026) document no. 1, this reform only optimizes floating rules, with three core elements unchanged:

1. National harmonization of basic premiums, with no increase

The first year of the six and below (all sedans, suvs and new energy vehicles) was again $950; 6-9 cars were $1,100; non-operational minivans below 2 tons were $1,200; and ordinary two-wheeled motorcycles were $120. The national harmonization of standards and the fact that insurance companies do not have any power to raise their own prices are not overshadowed by rumours of “new energy vehicle price increases” and “regional price increases”。

2. Safeguards are increased at no price

The total liability limit was increased from $200,000 to $222,000, including $200,000 for death and disability, $20,000 for medical expenses and $2,000 for property losses; the total liability limit was adjusted to $19. 9 million simultaneously. This is equivalent to an additional $24,000 in guarantees to cover more losses in the event of an accident, less self-financing。

3. The insurance process remains unchanged and is not cumbersome

Whether it is mandatory or mandatory, it is impossible to go on the road without having to buy it; the basic process of reporting, assigning responsibility and settling claims is the same as before and does not have to be readapted to complex operations。

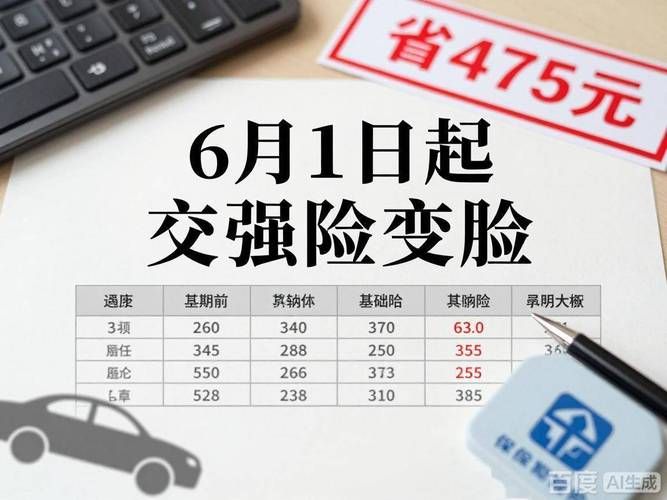

Ii. Core change: the fixed price of $950 ended, and what is the premium? A watch

The key aspect of the new regulation is the floating rule, whereby the final premium = the base premium x the no-compensation benefit factor x the regional coefficient x the traffic violation factor, is only linked to an accounting risk record, regional risk, serious breach of law, and is not related to the price of the vehicle, brand, commercial risk risk. For example, the most common **6 domestic vehicles (950 basic premiums)** are floated as follows:

Flow factor actual premium (approximately) core statement

A minimum of $ 0. 5,475 for 3 years and more without liability

Two consecutive years of no-account accidents 0. 8,760 national, 190 compared to original prices

One year in a row, without liability 0. 9,855 won, 95 won over the original price

The last year's no-account accident, $1. 0,950

One incident in the previous year, 1. 0,950

Two responsible accidents in the previous year, $1. 2,1140

Three responsible accidents in the previous year. 1. 5,1425

5 and above/responsible deaths 2. 0 1900 national maximum price, double direct

Three, two key details: don't step on these five faults, or you'll be busy

1. Regional coefficient: minimum premium varies by region

The country is divided into risk areas of a-e by traffic accident rate, with the lowest category a and the highest category e, with coefficients ranging from 0. 9 to 1. 1:

- category a (inner mongolia, hainan, qinghai, tibet): minimum of $475 for three consecutive years

- class b (shunxi, yunnan, guangxi): a minimum of $522. 5

- category c (gansu, guizhou, xinjiang): minimum $570

- category d (beijing, tianjin, hebei, ningxia): minimum $617. 5

- category e (liao ning, shanghai, jiangsu, zhejiang, guangdong, shandong, etc.): a minimum of $665

The regional coefficient is set by the state and the owner is unable to change it, but it does not affect the general direction — as long as it is safe to do so。

2. Traffic violation coefficient: only serious offences are punishable without prejudice to ordinary violations

Many are concerned that “a red light will raise the premium” and that the new regulations are only aimed at serious violations of the law, with no effect on ordinary violations of the law, the imposition of pressure lines, the absence of seat belts, etc.:

- dui: up 15%

- drunk driving, hit-and-run, unlicensed driving, full 12: 30% up

- over 50%, red lights three times and above: up 20%

- death-related accidents: 30 per cent increase

To give an extreme example: a car owner was exposed three times in the past year and was drunk once, and the premium = 950 x 1. 5 x 1. 3 = 1852. 5, close to the maximum price。

Iv. Guide to hole avoidance: do not step on these five faults, or be busy

1. Error zone 1: irresponsible accidents also affect premiums

The new rules explicitly exclude the number of accidents for which there is no liability! For example, being tailed and held to account without prejudice to the discount on the next year's premium, a regular car owner is no longer required to pay for another's fault。

2. Misdirection 2: a minor violation would also increase the premium

Only serious violations can trigger upwards, and ordinary violations (e. G. Violation of a stop and failure to wear a seat belt) do not affect the payment of insurance premiums and are not deceived by rumours of a “breeding 200” violation。

3. Mistake 3: new energy vehicle premium increases

Basic premiums are identical to fuel trucks, floating only by driving behaviour, and the owners of new energy vehicles do not worry about additional price increases。

4. Error area 4: renewal of insurance until 1 june, based on new rates

The insurance policy, which was implemented on 1 june at 0000 hours and renewed by 1 june, is still calculated in accordance with the old rules; all subsequent insurance coverage on 1 june is based on the new rates。

5. Error area 5: minimum discount for continuous absence of accidents

Not all non-accident-free owners receive a minimum of $475, depending on the risk level of the region, but only long-term irresponsible owners in category a low-risk areas。

V. Recommendations for exercise: how to drive with the least money

1. Maintaining a record of impunity: the longer the successive incidents of impunity take place, the greater the discount, the less liable for three years, the most direct cost-saving technique。

2. Stay away from serious violations: serious violations such as drunk driving, drunk driving and hit-and-run not only involve deductions of points, but also result in a direct doubling of premiums。

3. Collection of a certificate of liability: in the event of an incident for which there is no liability, it is essential that a certificate of liability issued by the traffic police be kept in order to avoid disputes over subsequent premiums。

4. Pre-renewal record: prior to the renewal of the guarantee on 1 june, check their own records of liability risk and serious violations to make sense。

Vi. Urgent reminder: from 1 june, these changes will take root remember

1. Time of implementation: from 0000 hours on 1 june 2026, there was no transition period。

Scope of application: all motor vehicles, including domestic vehicles, operating vehicles, motorcycles, etc。

3. Core logic: rewards and penalties, cost savings for safe driving, overpayment for risk of violation。

4. Protection of rights and interests: the basic premium, the amount of the guarantee, the process of insurance remains unchanged, and insurance is guaranteed。

The new rule of 2026, the most equitable reform in 16 years! It breaks the irrational pattern of “good and bad drivers at the same price” and allows safe drivers to enjoy real benefits, forcing people to follow the rules of engagement and travel civilized。

Friends of the family who have a car are quick to check their insurance records and violations, counting the amount of money to be paid next year. From now on, discipline and risk are both safe and free. Why not