The cost accounting of school canteens not only relates to operating gains and losses, but also affects the pricing of meals and the experience of teachers and students, at the core of which is the clear dismantling of “where money is spent and how much money is spent” and the control of costs through precision management. The following is a complete accounting logic based on cost composition, accounting steps, and practical skills, which will help the cafeteria to cost efficiently。

First understand: the four core components of school canteen costs

The cost of school canteens is not like an enterprise “buying raw materials for direct production”, but rather involves the “procurement-processing-services-operated” chain, which is divided into four main categories, each with a clear accounting breakdown, one of which cannot be:

(i) food cost: the highest proportion of “core expenditure” (usually 60-70 per cent of total cost)

This is the “big head” of the canteen cost, covering all raw materials directly used for the preparation of meals and accounting for them in detail to “class - specification - quantity - unit price”, avoiding general accounting。

Main foods: rice, flour, groceries (meat, maize, oats, etc.), noodles, buns, bun embryos, etc., are accounted for by “kg/chip”, e. G., “neast rice 1. 5/cick, purchase of 2,000 pounds per week, expenditure of 3000 pounds”。

2. By-catch:

(a) meat: pork (five flowers, skinny meat, steaks, etc., at unit price in parts), beef, chicken, duck, etc., with attention to the distinction between “freeze” / “fruit” (fresh is expensive but tastes good and frozen is more expensive)

Avian eggs: eggs, duck eggs, etc., accounted for by “one per pound”, e. G., “average eggs 0. 6 per pound, 500 purchased per day, 300 spent”

Aquatic species: fish, shrimp, shellfish, etc., accounted for by "kg" with a note for "fresh / frozen"

Vegetables: leaves and vegetables (creas, spinach, etc., perishable), root and root (tatoes, carrots, etc., durable storage), fungs and mushrooms (smocks, golden needles, etc.), calculated as “chips”, to calculate the “cleaning rate” (e. G., 7 pounds left after the pick-up of 10 pounds, 70 per cent of the netting rate, and the actual effective cost is based on 10 pounds of expenditure, 7 pounds of pure food)

Toner oils (soybean oils, vegetableseed oils, etc., by “litres/drums”), salt, sugar, sauce, vinegar, spices (octopus, cuisine, etc.), sauces (beans petals, ketchup, etc.), which, although low in unit price, are frequently used and are recorded by “bottles/bags/drums”, e. G., “5 litres of soybean oil, 60/drums, 3 barrels per week, with expenditure of 180 dollars”。

Semi-finished / completed products: e. G., prefabricated vegetables (red meat, fish fragrance packs), frozen dumplings, bread, etc., are accounted for as “packs/parts” and the purchase price is charged directly。

(ii) labour costs: “human costs” of stable expenditure (usually 15-25 per cent of total costs)

School canteens are manually related to “back cook-front-management” and are accounted for in detail by “post-pay structure”, avoiding the omission of “hidden human expenditure”。

Cooks: chefs (masters, sous-chefs, higher salaries), cooks (cutting, washing), noodles (conveys, buns), calculated as “monthly/daily salary”, e. G. “chef chefs, $8000/month, sous-chefs, $5,000/month, help cooks 3500/month”

Forepersons in the front hall: caterers, caterers, cleaning attendants, usually accounted for on the basis of “monthly salary” or “hour salary” (e. G. Students working part-time of $15 per hour)

Managers: cafeteria heads, procurement commissioners, financial accountants, calculated on the basis of “monthly pay + performance”

Implicit human expenditure: social security provident fund (unit share), overtime (sabbatical work), benefits (high temperature allowance, year-end award), such as “helping the kitchen social security unit to cover 800 yuan/month, with additional monthly cost”。

(iii) operating costs: operating “fixed + variable expenditure” (usually 10-15 per cent of total cost)

These cost elements, “fixed expenditure” (basically unchanged per month) and “changing expenditure” (with variations in usage), are to be accounted for separately from “optimal item” and “essential expenditure item”。

Fixed operating costs:

Rental of premises / property: rent may be free if the canteen is a school-owned site, subject to the calculation of “maintenance of the site” (e. G., wall repair, surface smoothing) and, in the case of off-site rental, the “monthly/annual rent” will be shared equally to the month

Depreciation of equipment: steam trucks, disinfectant cabinets, refrigerators, air conditioners, dining tables, etc., calculated as “total cost of equipment ÷ 12 months of service ÷” such as “10. 000 yuan steam carts 5 years of service, depreciation of $167 per month (10000 ÷ 5÷ 12≈167)”

Water (cleaning, cleaning), electricity (operation of equipment, lighting), gas (screw, steam) calculated on the basis of a monthly fee, e. G., “200 per month for electricity, 800 for water and 3000 for gas”

1. Change in operating costs:

(a) the cost of transportation of food: if the purchase is small, the supplier may add to the cost of freight; if taken, it is calculated as “oil + vehicle loss”, such as “two self-minings per week at a cost of $50 per fuel and $400 per transport per month”

/ supplement: broken supplements of dishes, chopsticks, spoons, etc., calculated as “one set”, e. G., “8 yuan per dish of ceramics, 20 dollars per month, 160 dollars spent”

Cleaning supplies: detergent, disinfectant, garbage bags, etc., calculated as “bottles/bags”, e. G., “10 pounds of detergent 25 dollars/barrel, 4 barrels per month, spent 100 dollars”。

(iv) other costs: neglectable “miscellaneous expenses” (usually within 5 per cent of total costs)

Such costs are small, but need to be recorded on a case-by-case basis in order to avoid the “less than a fraction” of total accounting。

The cost of food loss: vegetable decay, meat deterioration, expired staple foods, etc., calculated as “depletion × unit purchase price”, e. G. “10 chips of green vegetables are corrupted by improper storage, purchase price is 2 cilcas, loss cost is 20 dollars”

2. Administrative costs: cost of inspection of food items (e. G., weekly check-up of vegetable agricultural disability at 50 yuan each), processing of documents (health certificate, annual examination of food licence)

3. Contingency expenditure: equipment maintenance (e. G., refrigerator failure maintenance $300), temporary procurement (e. G., sudden salt shortage, emergency procurement expenditure $20)。

5 practical steps in cafeteria costing

When the cost composition is captured, it moves at the pace of the "day accounting - week summarization - month analysis" to ensure that the data are accurate and traceable, and that the newcomers are able to move quickly:

Step 1: establish a “base desk account” to record each expenditure

The core is that "who spends money, where spends money, how much" is recorded, and recommends "excel forms" or simple billing software (e. G. Nail approvals, graphite files) to avoid confusion in handwritten bookkeeping。

• procurement desk accounts: recorded as “date - name of foodstuff - specification - quantity - total price - vendor - receiving and inspectioner”, e. G., “2025. 8. 27, northeast rice, 2000 pound, 1. 5 yuan/chip, $3,000, vendor a, receiving and inspection master”

• manual billing: recorded as “month - job - name - pay - social security - overtime”, e. G. “2025. 8, chef, master li, $8,000, social security 800, overtime 500, total $9300”

• operating desk accounts: recorded as “date-cost type-value-note”, e. G., “2025. 8. 10, electricity, $2,000, august statement”

• depletion account: recorded as “date - depletion of food - quantity - unit price - cause of loss”, e. G., “2025. 8. 25, cabbage, 10 pounds, 2 yuan / pound, storage inappropriately decomposed”。

Step 2: daily accounting for “direct cost of food items” to control consumption on the day

The cafeterias purchase and use food items on a daily basis, and it is recommended that “costs of food items” be calculated after closed meals on that day and that the backlog of data be avoided。

• formula: direct cost of daily foods = total expenditure on daily foods purchased + amount of surplus foods from the previous day — amount of surplus foods from the current day — amount of daily foods lost

• for example: expenditure on the purchase of food items on 27 august for $5,000, the valuation of the remaining food items (rice, vegetables, etc.) on 26 august for $800, the valuation of the remaining food items after the closure on 27 august for $600 and the loss of $200 on that date for 27 daily food items for = 5000+800-600-200 = $5,000

• key: after a daily closed meal, the back cooker takes an inventory of “remaining foods” and is valued at purchase price (e. G. 50 pounds of rice, 1. 5 dollars/cick, valued 75 dollars) and losses are recognized on the same day (over-procurement or storage problems)。

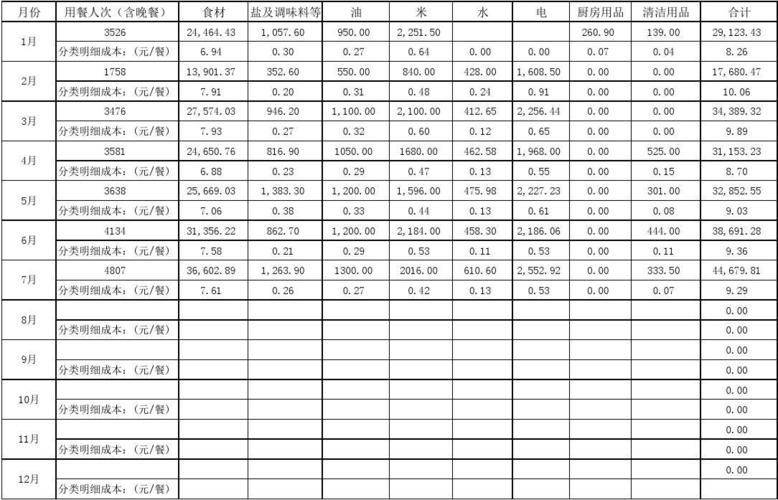

Step 3: a weekly summary of the “whole-class costs”, looking at trends and problems

On sunday or monday, a summary of the main types of costs for this week is presented, comparing the “data for last week” to see if there is any unusual fluctuations (e. G., if there was a sudden increase in labour costs this week, or if there was an increase in overtime)。

• matrix template (simplified version):

Step 4: monthly accounting of “unit cost of meals”, associated pricing

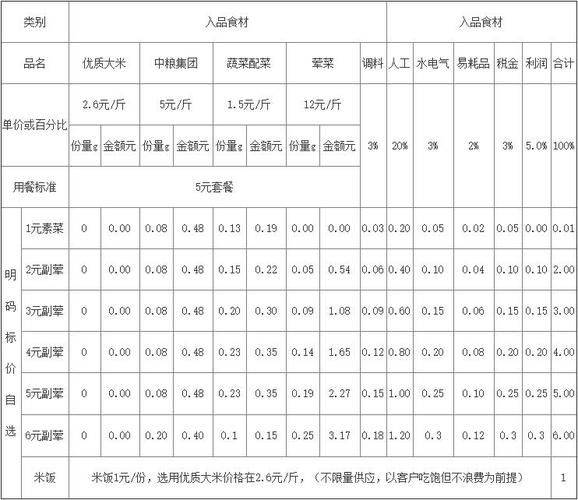

School canteens are usually priced on the basis of “sets / single items” and are calculated on a monthly basis at the “average cost of meals” to be reasonably priced (e. G. Cost $3/food, price $4, guaranteed micro-interest)。

• formula 1: average monthly per unit cost of meals = total monthly cost ÷ total monthly meals

For example, the total cost of august is $250,000, with a total of 80,000 meals (20,000 breakfasts, 40,000 lunches, 20,000 dinners) and the average cost per meal per month = 250,000 ÷ 80,000 ≈ 3. 13 / copies

• formula 2: single cost = single food consumption x unit cost of food + shared labour / operating cost (suitable for fine pricing, e. G. Accounting for tomato eggs)

For example, per tomato egg 0. 3 kg (us$ 2/chip, us$ 0. 6), egg 1 (us$ 0. 6), trim 0. 1, shared labour / operating cost 0. 2, single cost = 0. 6 + 0. 6 + 0. 1 + 0. 2 = 1. 5, priced by us$ 2。

Step 5: analysis "cost optimization points" to reduce waste

Accounting is not an end in itself, but a search for "where to save money" and 3 analyses per month combined with data:

1. Analysis of consumption of food products: the highest consumption of food products (e. G., 10 per cent for leaves and 3 per cent for root) and adjustments in the volume of purchases (fruit and bulk purchasing of roots)

Artificial efficiency analysis: to see if there is a “floating of people” (e. G., during a peak time for cookers who cannot afford to do anything during a peak period) and to adjust the schedule (peaks with additional staff, peaks with cleaning or pre-treatment of food products)

3. Operational energy consumption analysis: to see if hydropower gas is wasted (e. G. Air conditioners are not open and taps are open), and to develop energy saving systems (e. G. After-cooking check of equipment's power supply, air conditioning temperature set at 26°c)。

Iii. Pocket avoidance and techniques: making costs more accurate and cost-efficient heart

The school canteen accounts often step on the pits of "failure, estimation, data irrelevant" and share three practical techniques:

Purchase of food items: "accept and accept + library" double punt to avoid "shortness"

• the supplier is required to provide a “delivery order” at the time of the procurement to clear the specifications, quantity and unit price

• post-cooking arrangements are specially accepted (e. G., helper + chef) and weighed on the spot (e. G., suppliers say they delivered 100 pounds of green vegetables, which they actually claim to be 95 pounds and 95 pounds for purchases), and the receipt and inspection form is signed to confirm that it is “unconformity”

• entering the bank by “subdivisions of goods” (e. G., meat in the cold zone, frozen goods in the cold zone, cooking in the dry area), labeling “the date of purchase + the term of preservation” and reducing losses due to expiry。

Manpower costs: “designation of duties”, avoidance of “ineffective human expenditure”

• clarify the “work content + workload” for each post, such as “three windows for the caterer, 1,500 meals per day”, avoiding “the busy person”

Part-time work for students is calculated as “actual working hours”, such as “3 hours per day, 15 yuan per hour per day for part-time work and 45 yuan per day for expenditure, avoiding waste of costs due to “fixed daily pay”。

Data tools: replacement of " manual accounting" with simple tools to reduce errors

• small canteens: using excel as a “dynamic table”, setting formulae to calculate automatically (e. G., input the number of purchases and the unit price, calculate the total price; enter the total monthly cost and the total number of copies, calculate the unit cost)

• cafeteria: using a canteen management system (e. G. “three meals cloud” “wiss cafeteria”) to achieve a “procurement-entry-out-accounting” single-key connection, even allowing for the direct counting of the “number of meals” on campus to reduce manual statistical errors。

Summary

The centrepiece of cost accounting for school canteens is “substantial, precise and hard work”: “substantial” to the expenditure per pound per post; “quasi” to the data being traceable and accountable; and “work” to the daily count, weekly aggregation, monthly analysis. At first, it may be difficult, but after a period of one to two months, it will be possible to figure out the cost patterns, both to ensure the quality of food and to achieve a reasonable profit, to satisfy teachers and students and to manage schools。