The end of the year

Choose which tax method is more cost-effective

Look down

What's the year-end award

Our commonly known end-of-year award is the one-time bonus paid to employees throughout the year, i. E., a one-time bonus paid to employees by the executive, enterprises, etc., on the basis of annual economic benefits and a comprehensive appraisal of their performance throughout the year. The one-time bonus also includes an end-of-year salary increment, which is paid on the basis of an examination and paid on the basis of performance。

How to calculate taxes

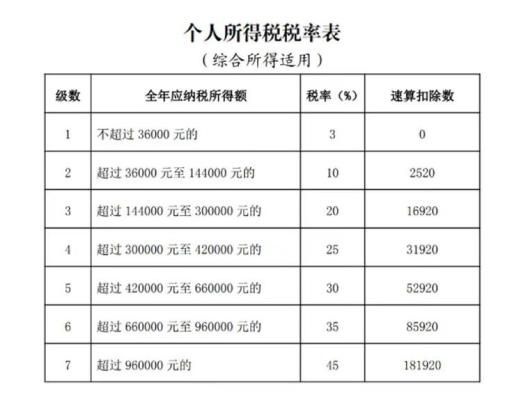

Method i: tax collection based on consolidation of income

The year-round lump-sum bonus is incorporated into the consolidated income received for the year, and the total amounts are based on the comprehensive income tax scale, which determines the applicable tax rate and the quick-calculation deduction, and combines tax payments。

Calculation formula: combined taxable income = {cumulative combined income (including one-time annual bonus)—cumulative cost deduction—cumulative earmarked deduction—cumulative earmarked deduction—cumulatively determined other deductions—contributions} × applicable tax rate—facing deductions

Method ii: individual calculation of taxes

According to the circular of the general tax administration of the ministry of finance on the continuation of the individual income tax policy for the full-year lump sum (official gazette of the general tax administration department of the ministry of finance no. 30 of 2023), by 31 december 2027, the resident individual received a full-year lump-sum bonus, which is in accordance with the requirements and is not incorporated into the consolidated income for the current year, divided by 12 months the income received for the full-year lump-sum bonus income, and determined the applicable tax rate and quick-calculation deductions, which are calculated separately on the basis of the consolidated income tax rate scale based on monthly conversions。

Formula: taxable = total one-time bonus income x applicable tax rate — speed deduction

Note: for each taxpayer in a tax year, a separate tax measure is allowed only once。

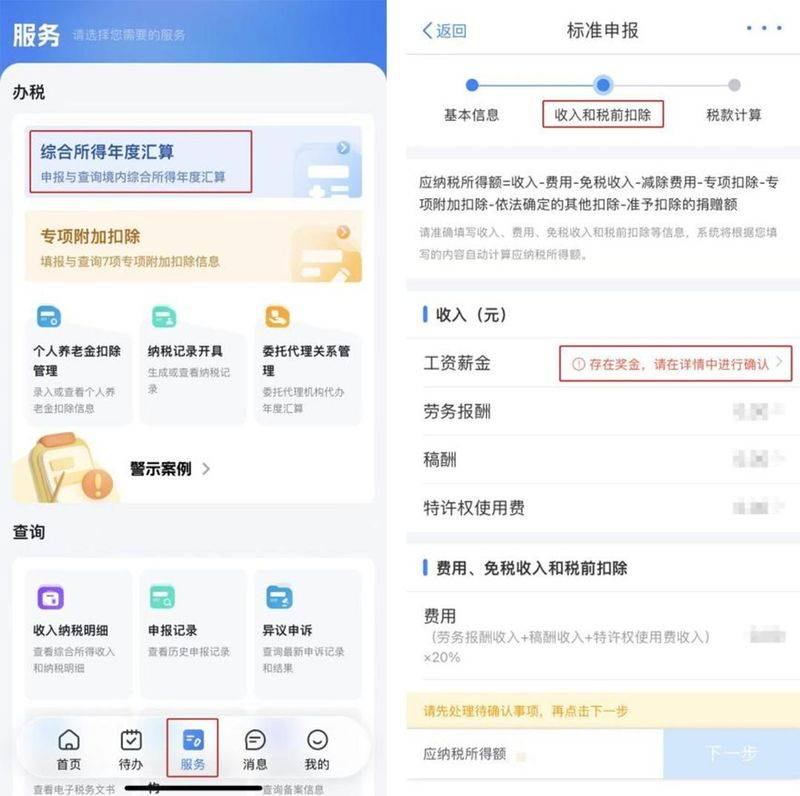

Personal income tax app

It doesn't matter if you do not count. When you do a tax year, you can log in the personal income tax app, click on [services] - [comprehensive annual income account], deduct the interface before tax, click on the right-hand reminder box in the “salary pay” column, choose the one-time bonus tax for the entire year, and the system automatically calculates the amount of the refund (salary) tax under two tax schemes, comparing which is the preferred one。

Example

Example 1:

The annual salary is $120,000 per week, the end-of-year prize is $60,000, and the total deduction for the year is $30,000。

1. In the event of an election to combine the combined proceeds to calculate tax:

The end-of-year award of $60,000 and the salary of $120,000 are taxed, net of costs of $60,000 and other deductions of $30,000。

Taxable income = 60,000 + 120,000 - 60 000 - 30000 = 90,000 yuan, applicable tax rate 10 per cent and speed deduction 2520。

Personal income tax due throughout the year = 90,000 x 10%-2520 = 6480 yuan。

2. If a separate calculation is chosen:

(1) calculation of the end-of-year taxable amount:

The annual lump-sum bonus income is divided by 12 months = 60,000 ÷ 12 = 5,000 yuan, with the applicable tax rate of 10 per cent and a quick deduction of 210。

End-of-year award tax payable = 60,000 x 10 per cent - 210 = $5790。

(2) calculate the taxable amount of other combined proceeds:

After deducting the cost of $60,000 and other deductions of $30,000, the taxable income = $30,000, the applicable tax rate is 3 per cent and the quick deduction is 0。

Other combined income taxable = 30,000 x 3 per cent-0 = 900 yuan。

(3) the amount of personal income tax due for the full year = the amount of the year-end award + the amount of other combined income = 5790 + 900 = 6690。

By contrast, it is known that a tax of $6,480 is required for a small week of combined earnings and $6,690 for a separate calculation. Thus, it would be more cost-effective for small weeks to opt for a combined income calculation。

Example 2:

Wang's annual salary is $20,000, the year-end award is $50,000, and special deductions such as the “three risks, one money” and special deductions amount to $30,000。

1. In the event of an election to combine the combined proceeds to calculate tax:

The end-of-year award of $50,000 and the salary of $20,000 are taxed, less the cost of $60,000 and other deductions of $30,000。

Taxable income = 50,000+20000-60000-30000 = $160,000, applicable tax rate of 20%, quick deduction of 16920。

Individual income tax due throughout the year = 160000 x 20% - 16920 = 15080。

2. If a separate calculation is chosen:

(1) calculation of the end-of-year taxable amount:

The annual lump-sum bonus income is divided by 12 months = 50,000 ÷ 12 = 4166. 67, with the applicable tax rate of 10 per cent and a quick deduction of 210. The end-of-year tax payable = 50,000 x 10 per cent - 210 = 4790。

(2) calculate the taxable amount of other combined proceeds:

The deduction of $ 200000 is after deduction of $ 60,000 and other deduction of $ 30,000。

Taxable income = 2000-60000-30000 = $110,000, applicable tax rate 10 per cent, speed deduction 2520。

Other combined income taxable = 110 000 x 10%-2520 = $8480。

The amount of personal income tax due for the full year = the amount of the year-end award + the amount of other combined income = 4790 + 8480 = $13270。

By contrast, it is known that the king is required to pay a tax of $15080 for the calculation of his combined earnings and a tax of $13270 for the calculation of his tax separately. Thus, it would be more cost-effective for wang to opt for a separate calculation of taxes。

Sweet tip:

The choice of a more cost-effective form of taxation, given the differences in the size and composition of each person's salary, requires a specific analysis and the choice of the most cost-effective method of calculation based on the actual situation。