The recent bulletin of the general state tax administration (dgi) on the full implementation of the new personal income tax law on certain lines of administration (dgi bulletin no. 56 of 2018) defines the method of calculation of the withholding of personal wages, salaries, remuneration for labour, remuneration received, withholding of royalties from royalties and withholding of personal income tax from non-residents. This paper tries to show you how to calculate through four small cases。

Case i

Mr. Zhang joined company a in 2021 and since 1 january 2021 the company has paid a monthly wage of $20,000 (before tax). Mr. Zhang's taxes are subject to a special deduction of 1,000 yuan/month and to a special deduction of 1,000 yuan/month; mr. Zhang has no other income, no other relief and no special matters other than his salary. Please calculate the amount of the specific tax withheld per month by company a as a withholding obligation from january to march 2021。

Answer:

In the event of the withholding of wages and salaries from the duty-bearer to the individual resident, the withholding tax shall be calculated on the basis of the cumulative withholding method and the full monthly payment of the full amount of the claim shall be processed. The calculation process is as follows:

January 2021:

Step 1:

Cumulative withholding of taxable proceeds

= cumulative income - cumulative tax-exempt income - cumulative cost deduction - cumulative special deduction - cumulative special deduction - cumulative other legally determined deduction = 2000-0-500-100-100-0 = $13,000

Step 2:

According to annex ii, table i of the state tax administration bulletin, no. 56 of 2018, the rate of withholding is 3 per cent for the month, with zero deductions

Step three:

Tax withholding due in the current period

= (cumulative withholding of taxable income x rate of withholding - speed deduction) - cumulative deduction - accumulated withholding of tax deduction

= (13,000 x 3 per cent-0)-0-0 = 390。

February 2021:

Step 1:

Cumulative withholding of taxable proceeds

= cumulative income - cumulative tax-exempt income - cumulative cost deduction - cumulative special deduction - cumulative special deduction - cumulative special deduction - cumulative other legally determined deductions

= 20000x2-0-5,000x2-10000x2-100x2-0=26,000 yuan

Step 2:

According to annex ii, table i of the state tax administration bulletin, no. 56 of 2018, the rate of withholding is 3 per cent for the month, with zero deductions

Step three:

Tax withholding due in the current period

= (cumulative withholding of taxable income x rate of withholding - speed deduction) - cumulative deduction - accumulated withholding of tax deduction

= (26,000 x 3 per cent-0)-0-390 = 390。

Note: of this amount, $390 represents the withholding of taxes in january。

March 2021:

Step 1:

Cumulative withholding of taxable proceeds

= cumulative income - cumulative tax-exempt income - cumulative cost deduction - cumulative special deduction - cumulative special deduction - cumulative special deduction - cumulative other legally determined deductions

= 20000x3-5,000x3-10000x3-100x3-0=39000 ($)

Step 2:

In comparison to annex ii, table i of the state tax administration bulletin, no. 56 of 2018, the rate of withholding is 10 per cent for the month, with a speed deduction of 2520

Step three:

Tax withholding due in the current period

= (cumulative withholding of taxable income x rate of withholding - speed deduction) - cumulative deduction - accumulated withholding of tax deduction

= (39,000 x 10%-2520)-0-390 = 600 yuan。

Note: in step iii (390 + 390), the withholding of taxes was made in january and february, respectively。

Synchronising folder

1. The withholding of the monthly withholding and withholding tax shall be paid to the state treasury within 15 days of the following month, and the individual income tax withholding declaration shall be submitted to the tax authorities。

2. If the amount of the annual withholding tax is not consistent with the amount of the annual tax payable, the annual consolidated income is paid by the individual resident to the competent tax authorities between 1 march and 30 june of the following year, with the tax refund being paid in full。

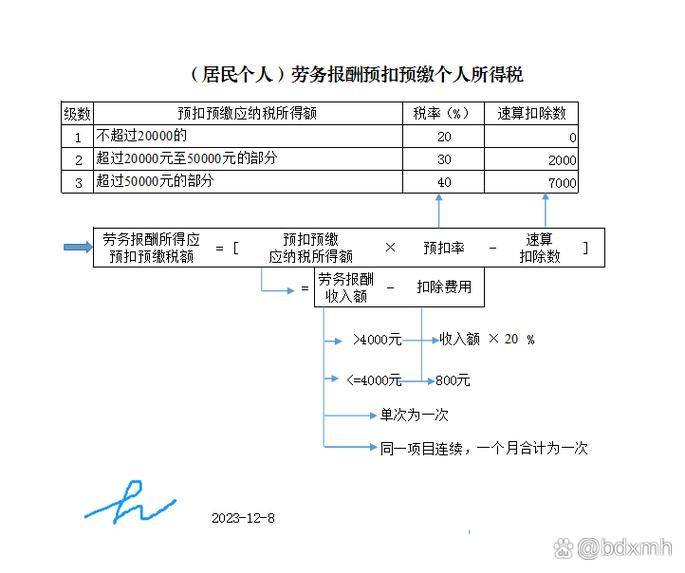

Case ii

In may 2021, mr. Lee took part in business activities at company b (non-employed) and received a lump sum of $20,000 (before tax) from company b. Assuming that mr. Lee is an individual resident, there are no other exemptions or special circumstances. Please calculate that in may 2021 company b, as a withholding duty, should withhold the amount of a specific tax paid in advance。

Answer:

The income derived from the payment of wages, wages and royalties to the individual resident is withheld from the individual, and the personal income tax is paid in the second or monthly withholding. The calculation process is as follows:

Step 1:

Income from labour remuneration

= income-cost

= 2000-20000 x 20% = 16,000 yuan

(the income from this labour remuneration exceeds 4,000, so the deduction is calculated at 20 per cent

Step 2:

Deduction of taxable proceeds

= labour remuneration income = $16,000

Step three:

In comparison to annex ii of the state tax administration bulletin no. 56 of 2018, table ii on individual income tax rates, the rate of the monthly withholding rate is 20 per cent, with a speed deduction of 0

Step 4:

Deductions due = withholding of taxable income x withholding rate — speed deductions

= 16,000 x 20-0 = 3200 yuan

Synchronising folder

1. The withholding of taxes from the obligated person shall take place within 15 days of the following month and shall submit to the tax authorities the individual income tax withholding declaration。

2. In the case of annual consolidated income payments by individual residents, the amount of income derived from remuneration for labour, remuneration and royalties shall be calculated in accordance with the law and incorporated into the annual combined income, calculated as taxable and paid in full。

Case iii

Between january and february 2021, mr. Lee worked for company c in china, which paid $10,000 a month (before tax). Assuming that mr. Lee is a non-resident individual, there are no other exemptions and no special matters. Please calculate the amount of tax paid by company c as withholding duty in january and february 2021。

Answer:

January 2021:

Step 1:

Income from non-resident personal salary = income = offset by cost

= 10,000-5,000 = 5,000 yuan

Step 2:

According to schedule iii of the personal income tax rate, issued by the state tax administration in annex ii to circular no. 56 of 2018, the monthly rate of withholding was 10 per cent, with a speed deduction of 210

Step three:

Deductions = taxable income x tax rate — quick deduction

= 5000*10% - 210 = 290 yuan

February 2021:

Step 1:

Income from non-resident personal salary = income = offset by cost

= 10,000-5,000 = 5,000 yuan

Step 2:

According to schedule iii of the personal income tax rate, issued by the state tax administration in annex ii to circular no. 56 of 2018, the monthly rate of withholding was 10 per cent, with a speed deduction of 210

Step three:

Deductions = taxable income x tax rate — quick deduction

= 5000*10% - 210 = 290 yuan

Synchronising folder

1. Non-resident individuals receive wages and salaries less the amount of their monthly income, the balance of which after the cost of 5,000 yuan, as taxable income, unlike the cumulative withholding method adopted by resident individuals。

2. Non-resident individuals shall be informed of changes in the basic information of the person who has withheld the tax during a tax year, when the personal conditions of the resident have been met, and shall, after the end of the year, be paid in accordance with the relevant rules of the resident individual。

Case iv

In january 2021, mr. Lee was involved in business activities with company c in china, which paid a lump sum of $10,000 (before tax). Assuming that mr. Lee is a non-resident individual, there are no other exemptions and no special matters. Please calculate the amount of tax paid in january 2021 by company c as a withholding agent。

Answer:

Step 1:

Non-resident personal labour remuneration

= income-cost

= income-income x 20% = 10,000-10,000 x 20% = 8,000 yuan

Step 2:

According to schedule iii of the personal income tax rate, issued by the state tax administration in annex ii to circular no. 56 of 2018, the monthly rate of withholding was 10 per cent, with a speed deduction of 210

Step three:

Deductions = taxable income x tax rate — quick deduction

= 8,000*10% - 210 = 590 yuan

Reminder: the balance of income earned by non-resident individuals on remuneration for their labour, remuneration earned on their work and royalties less 20 per cent of the cost。

The amount of income derived from such work is reduced by 70 per cent。

Non-residents ' personal wages, salaries, remuneration for labour, remuneration for work, taxable tax on royalties = taxable income x tax rate — quick deduction

Policy basis

1. Personal income tax law of the people's republic of china

2. Bulletin of the general state tax administration on the full implementation of certain aspects of the new personal income tax law (official gazette no. 56 of 2018)

3. Report of the state tax administration on the publication

Official gazette no. 61 of 2018