@all

The consolidation of personal income tax revenues is about to begin in 2024, and in the near future a number of comments have been received from netizens on issues related to the “one-time income” tax. The common “one-time income” consists of a one-time bonus throughout the year, a one-time indemnity for termination of employment contract, a one-time allowance for early retirement, etc. How do you pay a tax on these revenues? Do you need a remittance? What's the difference in tax treatment? Let's come and see the queen

One-time bonus income throughout the year

A one-time bonus for the whole year is a one-time bonus paid to an employee by the administrative agency, an enterprise or other person who withholds payment, depending on his or her annual economic efficiency and the comprehensive appraisal of the employee's performance throughout the year. The one-time bonus also includes the annual salary and the performance salary payable by the unit applying the system of annual salary and performance pay at the end of the year。

Method of calculation

Individual residents receive a one-time bonus throughout the year, in accordance with the circular of the general state tax administration on the methods of calculating personal income tax, such as adjusting the individual's entitlement to a one-time bonus throughout the year. As provided for in regulation no. 9, before 31 december 2027, the amount received by dividing by 12 months the income from the one-time bonus for the full year is not included in the consolidated income tax income for the current year, and the applicable tax rate and rate deduction are calculated separately on the basis of the monthly combined income tax rate scale (hereinafter referred to as the monthly rate scale). The formula is: taxable = one-time bonus income for the full year x applicable tax rate — speed deduction。

Individual residents receive a one-time bonus for the whole of the year, and may also opt to be taxed by combining the combined income for the current year。

Calculate cases

In 2024, chang received only a combined salary, with a full salary of 200,000 yuan, a one-time annual bonus of 24,000 yuan at the end of the year, a special deductible of 44,000 yuan, a special deduction of 44,000 yuan for the entire year, and no other deductions or exemptions, assuming that a separate tax is chosen for the annual exchange rate

1. Determination of applicable rates:

The amount received by dividing the income from the one-time bonus for the full year by 12 months is determined on the basis of the monthly scale of rates, the applicable tax rate and the quick deduction. 24000 ÷12 = 2000 dollars, corresponding to 3 per cent tax and zero speed deduction。

2. Calculation of taxable amounts:

Annual lump sum tax payable = 24,000 x 3 per cent = 720 yuan

Attention

1. For each taxpayer in a tax year, the preferential taxing of a one-time bonus for the entire year is allowed only once。

2. Employees receive a variety of prizes in addition to one-time bonuses throughout the year, such as semi-annual awards, quarterly awards, overtime awards, advanced awards, attendance awards, etc., which are combined with the current monthly salary, salary income and are subject to individual income tax in accordance with the tax laws。

3. Income from the one-time bonus for the whole year can be combined into the consolidated income for the annual remittances, or taxed separately under the one-time bonus policy for the entire year。

One-time indemnity for termination of employment contract

A lump sum compensation for termination of an employment contract is a lump sum of income (including financial compensation, subsistence allowance and other benefits paid by the employer) from the termination of the employment relationship。

Method of calculation

The lump-sum indemnity for the termination of an employment contract is exempt from personal income tax up to the amount of three times the average salary of the local employee in the previous year; the portion above three times is not included in the sum of the income received in the current year, and a comprehensive income tax scale is applied separately to calculate the tax。

Calculate cases

In 2024, company a received a one-time economic compensation of $370,000 for the loss of staff and the termination of zhang's employment contract. Assuming that the average salary of the local employees in the previous year was $80,000, how would the lump sum compensation for the termination of their employment be taxed

1. Determination of applicable rates:

370,000-80000 x 3 = $130,000

Based on the annual comprehensive income tax scale, the applicable tax rate is set at 10 per cent and the quick deduction at 2520。

2. Calculation of taxable amounts:

Taxable lump-sum indemnity for termination of employment contract = 130,000 x 10 per cent-2520 = 10480 yuan

Attention

1. The average wage of a local employee in the previous year is the average social wage of a municipal employee in the municipality directly under the authority of the former employer, the planned municipalities, the sub-provincial municipalities and the municipalities (districts, states, unions) in the previous year。

2. The termination of an employment relationship between an individual and an employer receives a one-time compensatory income without the need to include the combined proceeds for annual remittances。

One-time compensatory income for early retirement

One-time supplementary income earned by an individual following an early retirement procedure。

Method of calculation

The one-time compensatory income for early retirement shall be divided equally according to the actual number of years between the early retirement procedure and the statutory retirement age, the applicable tax rate and the quick deduction, and the combined income tax rate scale shall be applied separately to calculate the tax. Formula:

Formula: taxable amount = [(((as a result of one-time supplementary income processing the procedure of early retirement to the legal retirement age) – cost deduction) xx applicable tax rates - quick deductions}x actual years from early retirement to mandatory retirement age

Calculate cases

In january 2024, zhang filed for early retirement, two years after normal retirement, and received a lump sum of $180,000 in the same month, at a cost deduction rate of $60,000, and how is the lump sum of his early retirement income taxed

1. Determination of applicable rates:

180,000 ÷2-60000 = $30,000

The applicable tax rate is set at 3 per cent according to the annual comprehensive income tax scale。

2. Calculation of taxable amounts:

One-time compensatory income taxable for early retirement = 30,000 x 3 per cent x 2 = 1800 dollars

Attention

1. The number of assessed years is the actual number of years from early retirement to the mandatory retirement age。

2. A one-time supplementary income earned by an individual as a result of an early retirement procedure does not have to be included in the combined proceeds for annual remittances。

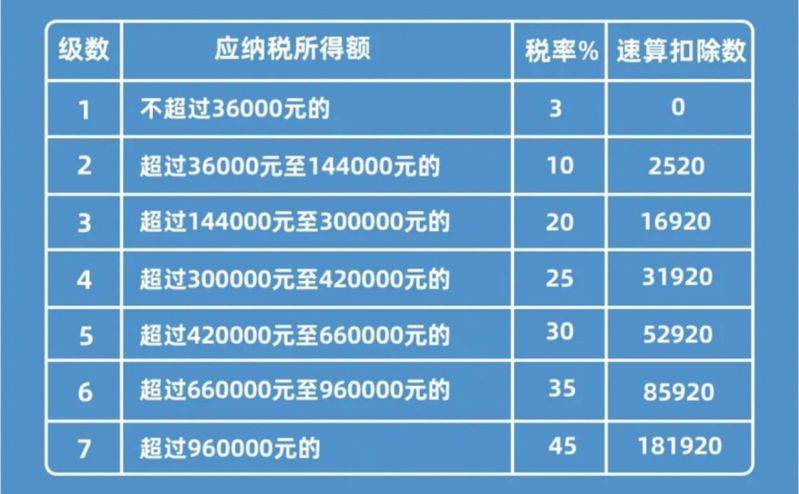

Relevant scale of rates

Annual comprehensive income tax scale

Combined monthly income tax scale

Policy basis

1. Circular of the general state tax administration on the adjustment of the method of calculating personal income tax for individuals, such as one-time bonuses for the entire year (state tax) [2005] no. 9)

2. Circular of the general tax administration of the ministry of finance on the interface between preferential policies as a result of the amendments to the personal income tax act (2018) no. 164)

3. Circular of the ministry of finance of the general directorate of taxation on the continuation of the individual income tax policy for a one-time bonus for the entire year (official gazette of the general directorate of taxation of the ministry of finance no. 30 of 2023)