From the mba think tank encyclopedia (https://wiki. Mbalib. Com/)

Cost

The monetary expression of the value of the materialized work that enterprises consume to produce goods and provide services, or the work that is necessary for them, is an important component of the value of goods. Cost is an economic dimension of the commodity economy。

Economic nature of costs

Max had scientifically pointed out the economic nature of the costs: “the value of each commodity w produced in a capitalist manner is expressed as w=c+v+m. If we subtract the residual value m from the value of this product, then the remaining value of the commodity is the equivalent or compensatory value of the c+v capital value spent on the factors of production”. “this part of the value of the commodity, that is, the part that compensates the price of the means of production consumed and the price of the labour used, only compensates the capitalist for what the commodity consumes itself, so for the capitalist, it is the cost of the commodity” (capitals, vol. 3). Marx engles, vol. 25, people's press, 1974, p. 30. This statement by marx, first, points to the economic nature of the cost of the product rather than the cost in general; secondly, the economic nature of the cost of the product is indicated from the point of view of cost as c+v. Because the value of c+v cannot be measured, the cost that one can measure and manage is actually the price of c+v, or the price of the cost; and thirdly, what compensates for the cost of the production of the commodity, is actually an indication of the contribution of the cost to reproduction. In other words, the cost of the product is a measure of compensation for the maintenance of simple reproduction by the enterprise, and it can be seen that the high and low level of the product cost, under certain conditions of the product's sabbatical and marketing prices, constrains not only the survival of the enterprise, but also determines the residual value of m, or profit, thus limiting the possibility of reproduction expansion. Marx's examination of costs, both in terms of cost and compensation, is a complete understanding of the nature of costs. Under conditions of commodity production, consumption and compensation are uniform. Any cost is always a matter for individual producers, and compensation is a process for society. It is two different things to ask for compensation and whether compensation is available. This has forced commodity producers to focus on costs, to strive for maximum regulation, to seek compensation with less cost and to maximize profits。

It has also been argued that our country is in the early stages of socialism, allowing for the co-existence of production subjects with multiple ownership systems, and that the cost should be commensurate with the current economic system, using the following theoretical costs. The main producer is a small commodity, whose only means of production require the purchase of the means of production, and the labour required is the producer itself, which does not have to pay, and which can be used as a theoretical cost to c; the main producer is a state enterprise, with society as the main subject; the cost of materialized and active work in the production of goods can be regarded as a social cost, and as a cost to society, using c+v+m as a theoretical cost; and other producers generally use c+v as a theoretical cost。

Composition of costs

Cost components are subject to management needs and evolve as management develops. The components of the cost-setting by the state include, inter alia:

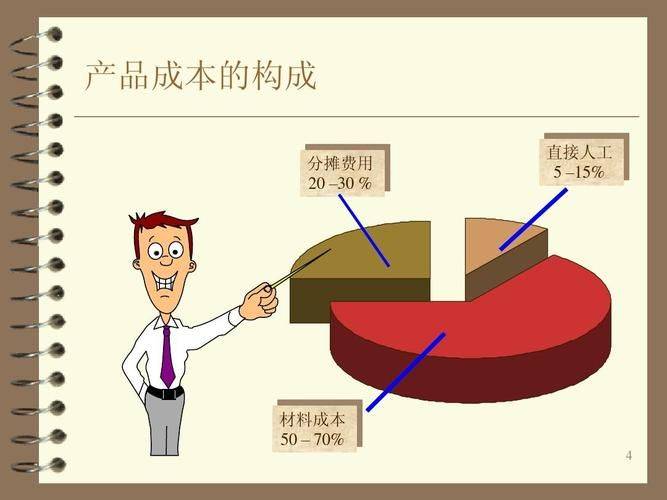

(a) the costs of raw materials, materials, fuel, etc., indicating the value of the labour objects consumed in the production of goods

2 depreciation, showing the value of the labour object consumed in the production of goods

3 wages, reflecting the value created by the necessary work of producers。

In practice, in order to promote economy, reduce losses and strengthen the economic responsibility of enterprises, loss of value in the form of lost goods in industrial enterprises, stoppages, etc. Are also included in the cost of products. In addition, certain components that should be distributed among the values created for society (such as the cost of insurance of property) are included in the cost of products. This illustrates the actual content of the cost of the product, requiring, on the one hand, the objective economic substance of the cost, and, on the other hand, the inclusion of certain elements that do not belong to c+v, in accordance with the country's allocation approach and financial management system, and, on the other hand, the inclusion of certain costs that are of a labour-intensive nature as out-of-service or out-of-pocket expenses。

Cost as capital consumption occurs in the production process, while the distribution of the output of the compensatory value falls within the area of distribution; the operator, who is the owner of the commodity, often lists some of the expenditures in the area of distribution as production costs, leading to inconsistencies between the actual compensatory value and the c+v++ already consumed。

Different implications of cost

(1) the cost is the economic value of producing and selling a certain variety and volume of products in resource-intensive monetary terms. The production of products by enterprises requires the consumption of means of production and labour, which is measured in monetary terms at cost, in terms of material costs, depreciation costs, salary costs, etc. The operating activities of the enterprise include not only production but also sales activities, and therefore costs incurred in the marketing activity should also be included. At the same time, costs incurred in managing production should also be included. At the same time, costs incurred in managing productive activities are of a cost-creating nature。

(2) the cost is the economic value of obtaining material resources. The price and cost paid by an enterprise for the purpose of carrying out its productive activities, acquiring various means of production or purchasing goods, is the cost of acquisition or purchase. As production operations continue, these costs translate into production and marketing costs。

(3) the cost is the value sacrifice of the resources made or to be paid for a given purpose, which can be measured in monetary units。

(4) the cost is the economic value sacrificed for the purpose of achieving one。

Classification of costs by different criteria based on different requirements for cost accounting and cost management。

The main methods of cost classification are:

(1) the conceptualization can be divided into theoretical and application costs。

(2) financial and administrative costs can be divided by application。

(3) actual and estimated costs can be divided on the basis of generation。

(4) the original and replacement costs can be divided according to the circumstances。

(5) the historical and future costs can be divided by the time of formation。

(6) the unit of measure can be divided into unit costs and total costs。

(7) the calculation is based on individual and average costs。

(8) the full cost and part of the cost can be divided by coverage。

(9) workshop and plant costs can be divided into the sequence of the production process。

(10) depending on the scope of production operations, it can be divided into production costs and marketing costs。

(11) costs can be divided into cost and unexpended costs in relation to benefits。

(12) associated and non-related costs may be classified in relation to decision-making。

(13) in relation to cash expenditure, it can be divided into cash and sunk costs。

(14) in relation to the plan, it can be divided into planned and projected costs。

(15) by volume change, these can be divided into marginal costs, incremental costs and differential costs。

(16) exemptions may be divided into avoidable and unavoidable costs。

(17) postponements, if any, can be classified into deferred and projected costs。

(18) controllable versus uncontrollable costs depending on whether they occur。

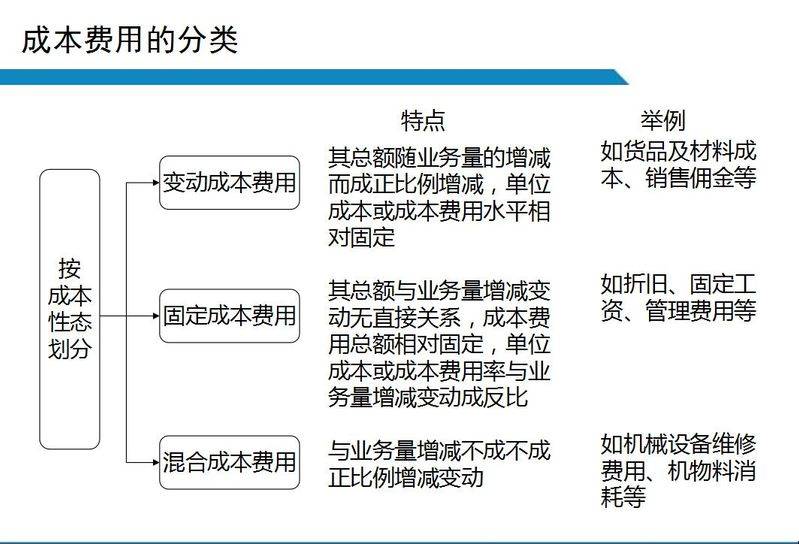

(19) by sex, can be divided into variable and fixed costs。

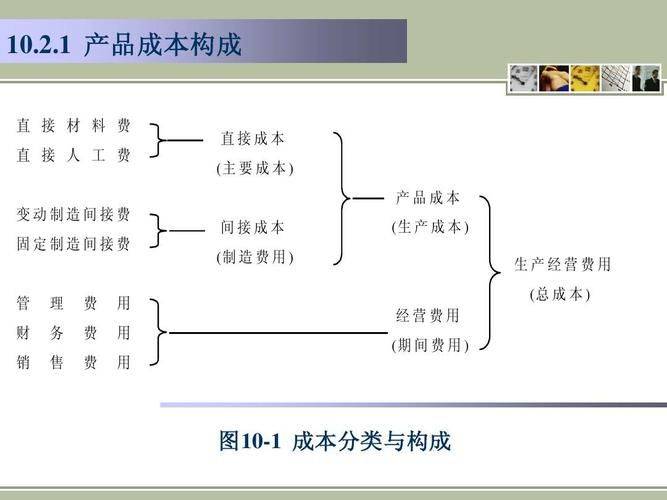

(20) direct and indirect costs, depending on the relationship to product production。

(21) the main costs and processing costs can be classified according to the composition of product costs。

Other cost classification concepts such as opportunity costs, liability costs, flat costs, target costs, standard costs, etc. Could be used to facilitate cost management。

The important role of costs in economic activities

(1) cost is the measure to compensate for production costs. In order to ensure continuity of production, enterprises must compensate for production costs, i. E. Financial costs. Enterprises are self-sustaining producers and operators of commodities whose production costs are compensated by their own production, i. E., sales revenues. Reproduction by enterprises is maintained on the same scale. The cost is the measure of the size of this compensation share。

(2) cost is the basis for setting product prices. Product prices are the monetary expression of the value of the product. At this stage, however, the value of the product cannot be calculated directly and precisely, but only at cost. As a major component of the value component, costs reflect the size of the value of the product, so that the cost of production of the product becomes an important basis for setting the price of the product. It is also true that costs need to be correctly accounted for in order for prices to be close to value by maximizing the level of consumption of socially necessary labour. The pricing of products is, of course, a complex process, and other factors should be taken into account, such as the state's price policy and other economic policy decrees, the supply-demand relationship of products in the market and the dynamics of market competition。

(3) cost is the basis for calculating the enterprise's earnings and losses. An enterprise is profitable only if its income exceeds what it incurs to earn. Costs are also the basis for the division of production and business costs and net income. Since costs set a minimum economic threshold for the price of the product to be sold, the lower the share of the cost in a given sales income, the more the net income of the enterprise。

(4) cost is the basis for the enterprise's decision-making. Enterprises need to strive to improve their competitiveness and economic efficiency in the market. First and foremost, sound and viable production and business decisions must be made, and cost is a very important factor. Costs, as a major component of prices, are key to determining the competitiveness of enterprises. For under market economy conditions, market competition is to a large extent price competition, whereas the actual content of price competition is cost competition. Only by working to reduce costs can enterprises make their products more competitive in the market。

(5) cost is an important indicator of an enterprise's performance in an integrated manner. The performance of all aspects of enterprise management can be reflected, directly or indirectly, in costs, such as the design of the product, the soundness of the production process, the quality of the product, the magnitude of the cost, the increase or decrease in the production of the product, and the coordination of the work done in the various sectors. That is why enterprises can be encouraged to strengthen economic accounting through forecasting, decision-making, planning, control, accounting, analysis and evaluation of costs, working to improve management, keep costs down and improve economic efficiency。

Ways and means to reduce costs

(1) savings in material consumption and lower direct material costs。

(2) increasing labour productivity and reducing direct labour costs。

(3) introduction of quota management to reduce manufacturing costs。

(4) strengthen budget controls and reduce costs over time。

(5) implementation of comprehensive cost management to reduce overall cost levels。

Methodology for cost review

Basic methodology for cost review:

1. Evaluate whether internal controls relating to cost costs exist, are effective and consistently complied with。

2. Obtain a breakdown of the relevant costs, review the correctness of the calculations and reconcile them with the relevant general ledger, ledger, accounting statement and related declaration。

3. Reviews the correctness of the recording and aggregation of the breakdown of costs。

4. Check the ratio of income and expenditure for large operations and review whether there are any under- or over-counting of operating expenses。

5. Review the correctness of accounting treatment and note differences in cost recognition between accounting systems and tax provisions。

(i) audit of main operating costs (as in the case of industrial production costs)

(ii) audit of other operating expenses

(iii) audit of sales costs as such

(iv) audit of out-of-service expenditures

(v) consideration of other costs to be recognized in taxes nuclear

(vi) audit of sales (business) costs

(vii) audit of management costs

(viii) audit of financial costs

From "https://wiki. Mbalib. Com/wiki/%e6%88%e6%9c%ac"