On 17 may, the commission on environment, public health and food security (envi) of the european parliament adopted, by 49 votes to 33, with 5 abstentions, a report on the establishment of a carbon boundary adjustment mechanism (cbam)。

While this development does not mean that carbon tariffs are already in full-fledged legislative process in the eu, given the weight of the envi commission in the european parliament’s environmental legislation, it is generally certain that the bill is essentially a final text, at best with some detailed changes, and is not far from being finally adopted by the european parliament。

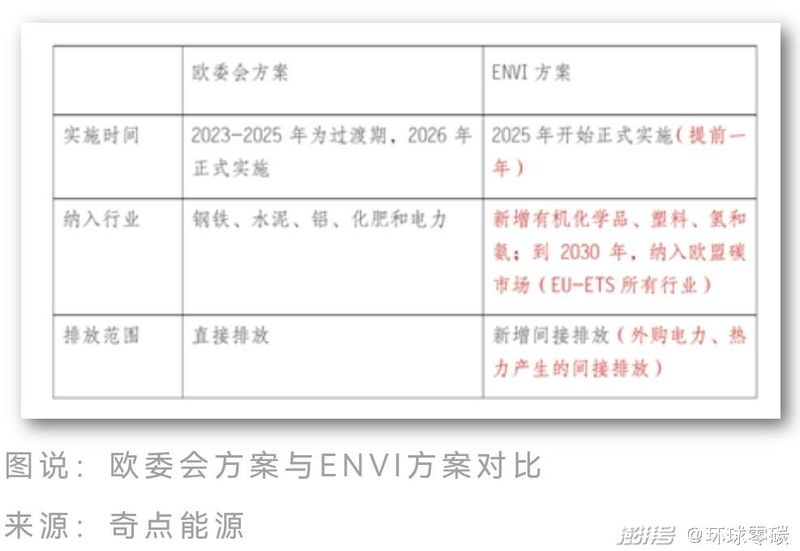

The envi programme is more radical than the previous ec and eu council programmes, has become more product-oriented and ahead of schedule, and has accelerated the convergence of carbon tariffs with the eu-ets, aimed at promoting faster and wider implementation of carbon tariffs。

As early as 14 july 2021, the european commission put forward a “fit for 55 package” package of proposals to address climate change, which aims to ensure that eu net greenhouse gas emissions by 2030 are 55 per cent lower than 1990 levels and to achieve climate neutrality by 2050. The eu carbon border adjustment mechanism, one of the core elements of the series, aims to reduce the risk of carbon leakage by imposing carbon tariffs on high carbon-intensive products imported from outside the eu, and the european commission issued more detailed regulatory proposals on the same day。

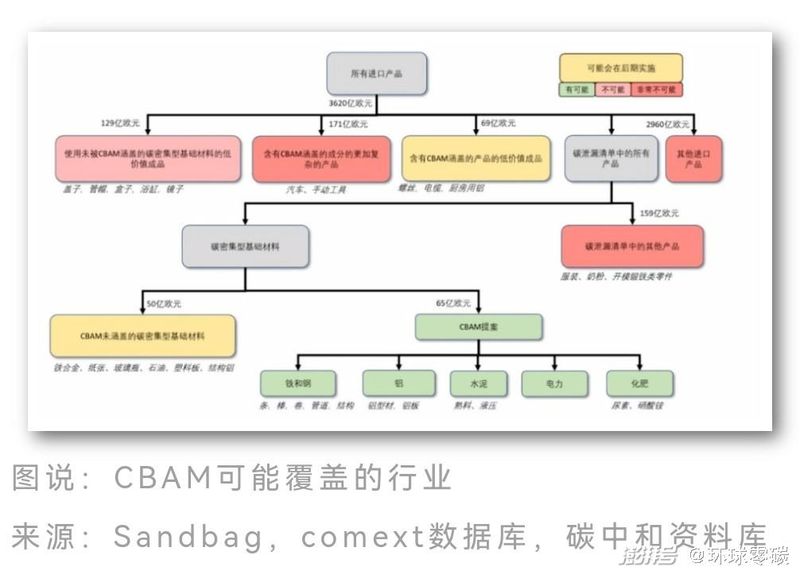

The five main product types covered by the original cbam proposal were the heavy industry, including electricity, all steel products (e. G. Flat steel, steel bars, steel bars, wire wires, except scrap iron, iron alloys), parts of steel (e. G. Steel pipes, tracks, containers, structures), aluminum products and products (e. G. Aluminium bars, aluminium bars, aluminium tubes), cement products (e. G. Clinkers, silicate cement), fertilizer-related products (e. G. Ammonia, ammonium nitrate, water-free ammonia, nitrate, urine)。

The relative original text covers only five sectors of steel, aluminium, cement, fertilizers and electricity, with new coverage of organic chemicals, plastics, hydrogen and ammonia。

Hydrogen and ammonia were included this time because europe used both as key fuels for decarbonization and as key clean energy sources in the energy sector as part of its energy transition and its move away from russian natural gas dependence. The eu countries are in the process of large-scale deployment and will have to import from abroad in the future。

Already in the early days of the carbon tariff, experts said:

The range of product collections appears to be five major industries, but actual implementation is likely to be greater。

The first is that the rules for the division of products have not been established and how the break-ups fall within these five product groups has not yet been determined. For example, how to determine whether steel products, steel bars or even bolt nuts are steel or not, is operational space. Low-value goods containing materials covered by the regulations (e. G. Steel screws or radiators, aluminium cans, etc.) may be included in cbam at a later stage and are currently unlikely to be candidates for cbam。

Commodities involving processes covered by the carbon leak list involve some degree of trade exposure that may not be covered by cbam (e. G. Pharmaceutical chemicals, other non-ferrous metals, textiles, etc.)。

Low-value commodities for carbon-intensive materials not covered by the proposal (e. G. Plastic packaging, ceramic tanks and flour basins) are likely to be covered under the envi proposal。

In comparison to the ec programme, the envi programme advanced the formal implementation of cbam to 2025 (one year earlier) and proposed the inclusion of all sectors of the eu carbon market (eu-ets) in the cbam mechanism by 2030 - five years earlier than proposed by the european commission。

In addition, in order to avoid double protection, any free quota granted to eu industries to address the risk of carbon leakage in the absence of a level playing field should be completely phased out of protected industries by 2030 when cbm is fully launched。

The members of the european parliament stressed that coherence between cbam and eu ets is essential to respect the principles of the world trade organization and that cbam must not be misused as a tool to strengthen protectionism。

Of even greater concern is the expansion of the envi programme to include carbon emissions. Unlike the ec programme, which only accounts for direct emissions, the envi programme includes indirect emissions, i. E., emissions from out-of-pocket electricity purchases, heat generation used by manufacturers, to better reflect co2 emission costs in industrial production。

Once adopted, this cbam programme will undoubtedly have an impact on our exports in the high carbon sector. This is because of the fact that 85 per cent of the 44 industries identified by the eu as most in need of carbon reduction are related to materials, energy and raw materials for industrial production processes。

According to the relevant research models, once implemented, china's carbon tax costs for steel, aluminium, fertilizers and cement will reach 17, 20, 17 and 31 per cent of exports, respectively. The current envi programme is subject to a vote by the plenary in june。

In addition, industries such as chemical products, essential metals, paper products and non-metallic mineral products, which are relatively less dependent on trade, are directly affected by high carbon emission intensity. In the steel industry, for example, china's carbon peak target for the steel industry was in 2025, in accordance with the guidance for the promotion of quality development in the steel industry issued this year by the ministry of industry and communications, among others. However, china's steel industry uses high furnaces and oxygen-top-blowing furnaces to make steel, with relatively high carbon emission intensity. Thus, the implementation of the eu cbam will place some constraints on exports of chinese steel products to the eu。

Senior engineer zhang jianhong, china international engineering consulting ltd., stated that the text of the new version of the bill on carbon border regulation mechanisms, the expansion of the industry, the addition of organic chemicals, plastics and hydrogen, and the inclusion of indirect emissions (emissions from out-of-pocket electricity) in tax collection, had significantly increased the negative impact on chinese exports and that my country could be one of the countries most affected by trade. If the european union were to extend the application of carbon border regulation mechanisms to all sectors in the future, the impact on china and the world would increase significantly。

Zhang jianhong said that for china, it was important to do its part and to steadily advance its carbon-capture work. Promote a green low-carbon transformation and accelerate the construction of modern energy systems. Manufacturing enterprises should strengthen energy-saving technologies and clean technologies and increase the proportion of clean energy use. At the same time, the development of carbon footprint accounting methodologies, standards and assessment and certification systems has been accelerated to enhance international voice. Fostering the development of the national assessment certification body brand, promoting multilateral recognition of international assessment certification and accelerating the upgrading of the international voice of our carbon footprint assessment certification. Actively involved in carbon tariff rule-making, bringing together large-scale carbon tariff losers, particularly developing countries, to actively defend their interests, advocate and uphold the principle of “common but differentiated responsibilities”, and actively participate in international coordination mechanisms and the development of international standards for the relevant industries。

Faced with the need for domestic green transformation and the challenge of “green barriers” to international markets, low carbon will become a mandatory requirement for a growing number of buyers。

(for more information)

--

For us: