As an upstream raw material in the iron and steel industry, iron ore prices were high in 2023, and the relevant sector made a few “plugs”. At the thirteenth china international iron and steel congress, held recently, representatives of miners and industry experts concluded that the supply and demand base for iron ore in 2024 had shifted to easing. Price hubs are expected to move downward。

Sufficient iron ore supply

“the supply and demand situation for iron ore has been at a critical balance for some time now moving towards a more relaxed situation.” according to gao xiaoyu, deputy general manager, china mineral resources group ltd。

Two factors have led to a shift in iron ore fundamentals from tightening to easing: on the one hand, iron ore taps continue to drive production and higher volumes of transport; on the other hand, demand in the downstream steel sector has declined。

The production and volume of iron ore from the four major mines also show that the mining taps are working to boost the expansion. For the 2024 fiscal year (as of 30 june 2024), the amount of iron ore produced by pytosian australia was 287 million tons (100 per cent interest base), with a record production of iron ore; the volume of iron ore delivered by the fortes river reached 191. 6 million tons throughout the year。

In the first half of 2024, the production of iron ore in the freshwater valley was 151. 4 million metric tons, an increase of 4. 1 per cent over the same period. Production in the second quarter was the highest recorded since 2018; the volume of iron ore sold was 143. 6 million metric tons, an increase of 10. 4 per cent over the same period. In the first half of 2024, the production of iron ore from taupier para remained stable, with a volume of 158. 3 million tons (100 per cent interest base)。

“since the first shipment to china in 1973, the company has cumulatively exported more than 3 billion tons of iron ore to china.” the vice-president for marketing and marketing (little mines) of the brethren and brethren group, ruimin, indicated. The company's 2024 fiscal year performance bulletin indicates that the company is increasing its research into the expansion of iron ore in western australia, aimed at increasing its annual production to 330 million tons, which will be completed by 2025。

According to chen coon, the senior shanghai iron ore analyst, the global excess of iron ore is expected to exceed 60 million tons by 2024 and the domestic fundamentals will shift from a supply shortfall in 2023 to an excess of 41 million tons: on the one hand, the share of mineral shipments destined for china increased; on the other hand, domestic mines began to be regenerated after summer security checks, resulting in a sufficient supply of iron ore in 2024。

Iron ore prices are expected to decline in 2024

Chen chong expected domestic iron ore prices to operate in an area of us$ 80 to 110 per ton in the second half of 2024, down from 2023 levels. The shanghai steel union data condensation shows that domestic iron ore prices in qingdo in 2023 fluctuated within the range of $97. 3 to $141. 5/dryton (based on 62 per cent of the australian powdered mine forward spot price index) and were at historically high levels。

Weak supply and demand are a major reason for the market to judge that the price of iron ore is expected to decline. The chen cannon presentation resulted in an increase in the overall stock of steel end and an increase in the losses of downstream steel plants. The overall demand situation is weak, with domestic crude steel and raw iron production falling in comparison. According to the national statistical office, crude steel production in the country in january-july 2024 was 6. 137 million tons, a decrease of 12. 794 million tons, or 2. 2 per cent, over the same period. In january-july 2024, domestic production of raw iron was 5. 0968 million tons, a 3. 7 per cent decrease over the same period。

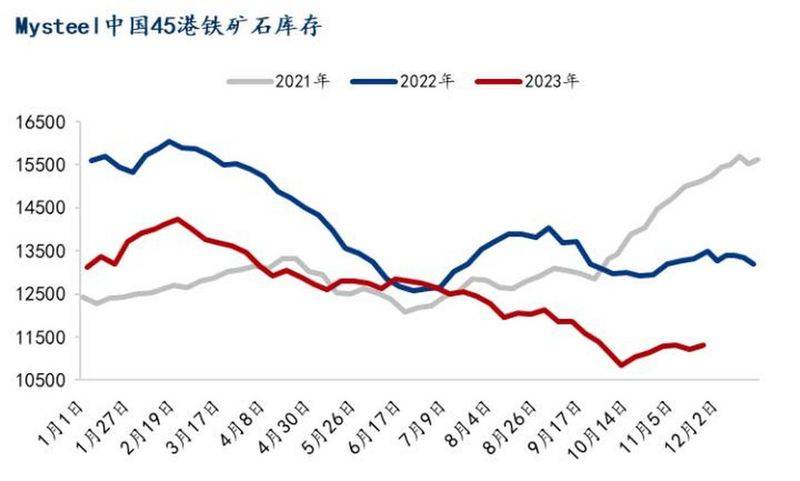

The weak operation of demand has led to the continued accumulation of iron ore in domestic ports. Chen quan stated that between january and july 2024, shanghai steel union counted 45 ports in the country where iron ore reached 72. 546 million tons, an increase of 5. 0120,000 tons, or 7. 4 per cent over the same period. In 2024, the domestic port iron ore will continue to accumulate, with imported ore stocks of 45 ports having a maximum value of 160 million tons or more。

According to gao xiaoyu, the current international raw materials pricing mechanism and the basics of supply and demand are exacerbated. Recently, a steel plant in the south went to qingdao port to purchase cash from the port and chartered boats to return to the steel plant. The rmb price system is more responsive to supply and demand because of differences between the dollar-pricing system for iron ore and the rmb-pricing system。

According to gao xiaowoo, the current dynamic is characterized by an increased imbalance in the distribution of value chains and a more unfavourable position for steel enterprises in terms of value distribution than at a more productive stage in the steel industry。