Twenty-seven years of implementation of the cost-accounting methodology for state-owned industrial enterprises would be historic。

Recently, the ministry of finance issued the enterprise cost accounting system for products (pilot) with a view to further regulating the accounting of the cost of the products of enterprises in the new context of economic development, improving the quality of information on the costs of products and providing services to microeconomic agents. The system will be fully operational as of 1 january 2014。

Indeed, as early as april 2010, china’s accounting journal reported on the difficulties encountered in accounting for the products of domestic enterprises on the basis of the “fine fees” of metallurgical mining companies, and called for the establishment of a unified system of accounting for the costs of the products of enterprises as soon as possible. Three years later, the system finally emerged。

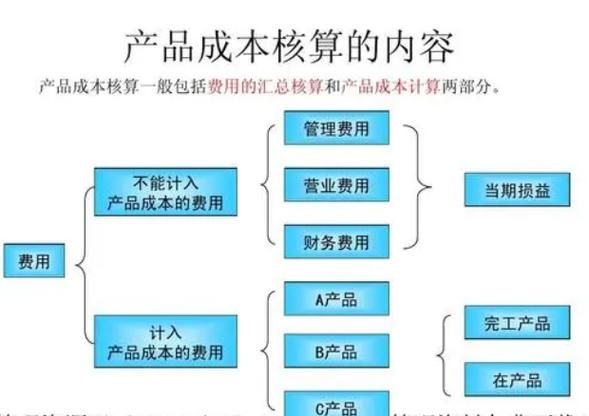

The new system defines the objects, scope and aggregation of accounting for the products of enterprises and covers enterprises in 10 industries, including mining enterprises. Mining enterprises, for example, will have systems to follow thereafter, and “facilitation fees” are no longer a problem for product cost accounting。

It is noteworthy that the new system also reflects many cutting-edge management accounting practices and experiences. From the point of view of management accounting, the introduction of the new system will result in more detailed accounting of the cost of the products of the enterprise。

Cost information is becoming more and more complete

Cost information is a direct reflection of the results of the enterprise's market transactions, and the results of the enterprise's operations can be accurately reflected in standardized and complete cost data。

However, prior to the release of the new system, the authenticity and completeness of enterprise cost information needed to be improved owing to the absence of a uniform product cost accounting system in the country. This has led to numerous disputes, particularly the increasing number of anti-dumping cases against some of our exports from abroad。

Professor of accounting at the south university school of management, hu tamaki, is the key to the issue. In his view, the main reason for the current incompleteness of information on enterprise costs was the arbitrariness of the enterprise cost accounting exercise. “the different industries and enterprises often carry out product cost accounting based on their `management needs'. Over the years, there has been widespread interest in surplus management, but there has been a lack of due attention to surplus management through product cost accounting。

The new system will effectively curb the arbitrariness of enterprise product costing. Private wang, professor of accounting at the beijing university of commerce and industry school of commerce and industry, told journalists that the promulgation of the system of accounting for the cost of business products (preliminary) would result in a uniform system of rules that would be binding on business accountants throughout the country. By organically integrating the elements of product cost elements in specific guidelines, such as inventory, fixed assets, borrowing costs, intangible assets, and employee remuneration, the system further refines cost accounting methods and harmonizes cost accounting projects, thereby reducing the arbitrariness of enterprise product cost accounting。

Improving the authenticity and completeness of information on the costs of enterprises through the design of the system is of great importance in the view of the financial inspector of china sea petrochemicals. He said that real and complete cost information facilitated the refinement of product cost analysis, budgeting, evaluation, helping enterprises reduce efficiency gains and increase their market competitiveness. At the same time, cost information under the harmonized system would enable enterprises to conduct international and domestic cross-reference analysis and reduce international anti-dumping pressures on exports。

We're going to take the line of "compatibility"

Externally, the lack of integrity of information on enterprise costs is due to the “discretionary” nature of cost accounting. However, from an internal management point of view, the process of accounting for the cost of the enterprise's products encountered some bottlenecks that were difficult to break。

The most important bottlenecks encountered by enterprises in cost accounting for their products, according to zhou, are the lack of uniformity and precision in the content, level of cost accounting and dimensions of accounting by different enterprises for the same product. He gave an example to journalists: “for the same cost as a refined product, some enterprises account for the cost of the product and others for the cost of the period. In addition, the level of accounting by enterprises is fairly broad and the responsibility is not specifically assigned to departments, workshops and classes.”

For its part, wang believed that one of the more obvious bottlenecks in accounting for the cost of the enterprise's products was uncertainty about the object of accounting. He explained, for example, that the coal industry had two views on the subject of cost accounting: one is for the original coal and the other for the coal products sold as commodities. Clearly, the latter has a much larger cost scope than the former. This has a direct impact on product unit costing, product cost analysis content and methodology, and product pricing。

“the lack of clarity in the definition of product cost-accounting objects can have serious consequences, which can affect the assessment of resource allocation efficiency in enterprises, i. E. The mismatch between the investment of the enterprise's resources and the output of the specific product.” according to private wang。

The above-mentioned issues may be only the tip of the iceberg in terms of the difficulties faced by enterprises in accounting for the cost of their products, and the new system is clear about them. There is no doubt, however, that enterprises will face more problems in their development。

In a deeper sense, the provisions of the new system provide domestic firms with a long-standing and well-established management idea that the cost-accounting of the enterprise's products must be built around cost management and serve cost management purposes. “in a popular saying, the cost of the enterprise's products must be accounted for in a `comparison of accounting'.”。

If an enterprise's work on product cost accounting is confined to the accounting level and does not extend to the cost management level, there is no way in which an enterprise can adequately rely on data-aided management or speak digitally. The cost-accounting of the products of an enterprise transforms the management of some of the original technical content into a problem of arithmetic with little technical content。

“it is clear that this is not the purpose of the enterprise cost accounting exercise.” according to hu, “the cost-accounting of an enterprise's products certainly requires the calculation of the cost of the product, but from a deeper perspective, the cost-accounting of an enterprise's products is the process of combing the enterprise's business processes, and the aggregation, collation and analysis of cost data is the analysis of business processes, which are behind each cost-project data.”

Behind the “harmonization” route is the concept of management accounting. According to hu, the most important inspiration for chinese enterprises to strengthen their internal management and enhance the value of their businesses is to build a holistic, full-time, and process-wide thinking on cost management。

Cost is a compensatory value, and an enterprise can determine the amount of cost compensation only if it has a reasonable accounting for the cost of the product。

According to ho yuming, compensation for the costs of the enterprise also preserves value, which is created on the premise that the costs are reasonably compensated. More importantly, through its cost-accounting work on products, strengthening cost-management thinking and “compatibility”, enterprises maintain low-cost advantages and become more competitive in order to generate value on a sustainable basis. Thus, the new system is important for both enterprise creation and preservation。

Looks forward to further rules

It now appears that, while the new system covers most industries in the country, different industries can continue to disaggregate different types of enterprises。

In his view, if the new system is to be truly solid, further rules will be needed. He told reporters: “each enterprise has its own ways and means for cost management, and the new system provides guidance for cost management. However, as the rules have not yet been issued, they do not reflect the full picture of the industry.”

The perspective of kong changdong was supported by experts. The wang jun stated that the authorities concerned should evaluate the effectiveness of the system after a certain period of effective implementation and then refine its contents selectively. Examples include cost plans based on a product cost-accounting system, cost-assessment and cost-analysis provisions; and the development of a product cost-accounting system in the context of enterprise information。

Reporter liu antxian