Core definitions of exchange rates and pricing 1

The exchange rate (foreign exchange rate) is the rate of exchange between the two currencies and can also be understood as the price of one currency expressed in another currency, which essentially reflects the purchasing power of the different currencies and is the basic price indicator for international financial transactions。

2. Two main basic methods of bid (the global core rules) (1) direct bid (2) indirect bid

Supplement: cross-exchange rate - the exchange rate between two currencies (e. G., united states dollars) is calculated by extrapolating the exchange rate between the two currencies, for example, usd/cny = 7. 2, usd/jpy = 145, which can be derived from cny/jpy = 145/7. 2≈20. 14 (rmb 20. 14)。

Classification of exchange rates (by different dimensions, approximation of different analytical scenarios) 1. Extent of movement by exchange rate: fixed exchange rate vs floating exchange rate (core classification, corresponding to subsequent exchange rate regime) 2. Transaction time: spot exchange rate vs forward exchange rate 3. Rates by market subject: official exchange rate vs market exchange rate 4. Scope of application by exchange rate: single exchange rate vs double exchange rate iii. Decision theory of exchange rate (core basis of financial science, explanation of underlying logic of exchange rate formation) 1. Purchasing power parity theory (ppp) - most basic exchange rate theory

Core logic: the exchange rate is determined by the ratio of the purchasing power of the currencies of the two countries, i. E., the “one price law” - the same commodity should be priced equally in the same currency in different countries (exclusion of transaction costs such as transport, tariffs, etc.)。

Interest rate parity (irp) - core theory linking exchange and interest rates

Core logic: interest rate differentials between the two countries determine the upswing of the forward exchange rate, and capital flows from low to high interest rate countries ultimately eliminate risk-free arbitrage (the core basis for international capital flows)。

Balance of payments — interpretation of exchange rates in terms of supply and demand

Core logic: the exchange rate is the price of foreign exchange, determined by the supply-demand relationship in the foreign exchange market, while the supply-demand of foreign exchange originates from a country's balance of payments (the bop is the core basis)。

Asset markets say - modern exchange rate decision theory (integrated multiple factors)

Core logic: treating both local and foreign currency assets as financial assets, with exchange rates determined by the balance of supply and demand in the asset markets of the two countries, taking into account not only prices, interest rates, but also expectations, monetary policy, economic growth, etc., and more appropriate for short-term exchange rate analysis (contain with current international financial markets)。

Iv. Main factors affecting exchange rate movements (short-term + long-term, backbone analysis)

Changes in exchange rates are the result of a combination of factors, the impact of which varies in time and intensity, and the core factors can be grouped into long-term and short-term:

1. Long-term factors (determinating fundamental trends in exchange rates) 2. Short-term factors (leading to short-term fluctuations in exchange rates, with more significant effects) are complemented by: inverse effects of changes in exchange rates (exchange rate economy, two-way transfer)

Exchange rates are not determined solely by economic factors, but their variations are also counterproductive to a country's economy, as reflected in:

V. Typologies and core features of exchange rate regimes (core composition of the international monetary system)

Exchange rate regimes (exchange rate regime) are a series of institutional arrangements made by a country's monetary authorities for the formation, volatility and mode of intervention of exchange rates. The international monetary fund (imf) is the principal classification and oversight body for the global exchange rate regime, with the core classification being fixed and floating exchange rate regimes, with various transitional exchange rate regimes in place。

1. Fixed-exchange-rate regime

Definition: the monetary authority fixes the exchange rate of the currency with a base currency (e. G. The united states dollar, the euro) or a basket of currencies at a certain level, and maintains exchange rate fluctuations at a very small level (usually within ±1 per cent) by means of foreign exchange intervention, exchange control, etc。

(1) major type (2) core strength (3) core impairment 2. Floating exchange rate system

Definitions: exchange rates are determined by the supply-demand relationship in the foreign exchange market, monetary authorities are not committed to maintaining fixed exchange rates and only intervene in cases of extreme exchange rate fluctuations (e. G., financial instability caused by large devaluations), and exchange rate fluctuations are not limited by fixed ranges。

(1) main type (2) core advantage (3) core weakness 3. Transitional exchange rate regime (intermediate rate system)

The exchange rate regime between fixed and floating, taking into account exchange rate stability and a certain degree of monetary policy independence, applies to countries with medium-sized economies where financial markets are not yet fully open

Imf classification of the latest exchange rate system (simplified version, 2024)

The imf divides the exchange rate system into hard nails, soft nails, floating, and other four main categories, with core equivalents:

Hard nails: monetary agency system, dollarization (e. G., use of the united states dollar in ecuador); soft nails: single currency / basket of currency, creeping nails; floating: managing floating, free floating; other: exchange rate target, mixed system. Vi. Basis for the selection of exchange rate regimes (core considerations for a country to develop an exchange rate regime)

A country's choice of exchange rate regime, without uniform criteria, needs to be combined with factors such as its economic fundamentals, economic structure, financial market openness, and core considerations:

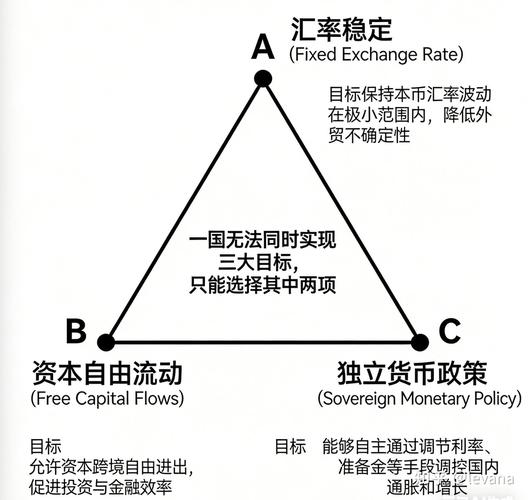

Economic size and openness: countries with small economies and high levels of openness (e. G. Small trading countries), suitable for fixed exchange rate regimes (exchange rate stability for trade); countries with large and medium economies (e. G., central, united states, europe), suitable for floating exchange rate regimes (higher demand for independent monetary policy); inflation: countries with high inflation rates and high volatility, suitable for fixed exchange rate regimes (which binds monetary policy to contain inflation); countries with stable rates, suitable for floating exchange rate regimes; financial market level development: countries with underdeveloped financial markets, with incomplete capital projects, suitable for fixed or intermediate exchange rate regimes (preventing capital movements from capital flows), suitable for floating exchange rate regimes; balance-of-payments situation: countries with small balance-of-payments fluctuations, suitable for fixed exchange rates; countries with large balance-of-payments fluctuations, suitable for floating exchange rates (by automatic exchange-rate reconciliation of income and expenditure); foreign exchange reserve size: countries with sufficient foreign-exchange reserves to support fixed exchange-rate regimes; countries with limited foreign-exchange reserves, difficult to maintain fixed exchange rates and vulnerable to currency crises. Classic theory: the "triple paradox" of the monder-flaming model (core guideline)

Core conclusion: the independence of a country's monetary policy, the free flow of capital and the fixed-exchange-rate regime cannot be achieved simultaneously, and only two of them can be chosen and one (the “iron law” chosen by the exchange-rate regime) abandoned。

Vii. Evolution of the global exchange rate regime (from fixation to floating, the evolution of the international monetary system) gold standard (1880-1914): classical fixed exchange rates, determined by gold parity, stability of the global exchange rate system, contributing to the first economic globalization; during the two world wars (1914-1944): exchange rate disruptions, countries applying floating exchange rates or strict foreign exchange controls, hampering international economic interaction; bretton woods (1944-1973): adjustable exchange rates, the dollar becoming the international core currency, and a stable post-war international monetary system, contributing to post-war economic recovery; jamaican system (1973-1914): after the collapse of the bretton woods system, the global move to a floating exchange rate system is the dominant phase of multiple exchange rate regimes, the dollar remains the core international currency, the gold is demonetaryized, and the imf allows countries to choose their own exchange rate system, which is the basic pattern of the current global exchange rate system. Viii. China's exchange rate regime (rmn-formation mechanism)

China has adopted a system of managed floating exchange rates based on market demand and supply, with reference to a basket of currencies (established in july 2005 after the readjustment of the remittances, subsequent refinements), with core features:

Market supply and demand are based on market demand: supply and demand in foreign exchange markets are central factors in determining the renminbi exchange rate and central banks reduce direct intervention; reference is made to a basket of currencies: not a single dollar, but a basket of currencies consisting of trading partner currencies (such as the united states dollar, the euro, the yen, the korean won, etc.), the exchange rate adjusts with a basket of currencies to avoid fluctuations in the single currency; managed fluctuations: central banks, through foreign exchange intervention, adjustment of reserves in foreign exchange, counter-cyclical factors, etc., reduce excessive fluctuations in the renminbi exchange rate and maintain the fundamental stability of the exchange rate at a reasonable level of equilibrium; and inter-bank exchange rate fluctuations: the median price of the inter-bank exchange market national currency against the united states dollar has fluctuated by £2 per cent, and the non-dollar to the national currency exchange rate is more volatile, giving the market greater pricing power. Core objectives of china's exchange rate regime

A balance between exchange-rate stabilization and market-based reforms that avoid large exchange-rate fluctuations that lead to financial instability, affect economic stability and gradually advance the marketization of the renminbi and contribute to the internationalization of the renminbi (which becomes an international settlement, investment, reserve currency)。

Welcome to me and learn to progress together