From november 2021 to date, the price of pigs has reached the “w” bottom stage and is stable. The average price of pork in 22 provinces rose from a low point of $18. 92/kg in april to $24. 21/kg on 1 july, an increase of 28. 0 per cent. The price of raw pigs also increased from $16,080 per ton at the end of april to $22,755 per ton on 4 july, an increase of 41. 5 per cent。

In our judgement, from the three-to-four-year cycle of pigs, the april 2022 cycle of pigs was built twice, and the current or new cycle of pigs is in its upper stages, as evidenced by the time pattern of denuclearization of production. It is expected that future price increases will be moderate, but without conditions for rapid and substantial upswing, and that future increases will depend on the degree of de-development of production capacity, owing to low and historically high levels of de-development。

1 pork cycle logic

1. 1 generation of pig cycles

The cycle of pigs is a cyclical fluctuation in prices during the production of raw pigs and the sale of pork. In particular, when the price of pork rises, farmers expand their capacity to produce, increase their capacity to produce sows, drive up the stock of pigs, increase the number of pigs produced when they mature, increase the supply of pork and decrease prices. Farmers have observed reduced pork prices, reduced production capacity, the phase-out of lively pigs, reduced pig storage and outlet, reduced pork supply and a resurgence of pork prices。

The production cycle of pigs determines a full cycle of pigs lasting three to four years, with minor periodic fluctuations during holidays and climate effects within one year. The production capacity of the pig can be increased, the stock of the pig is increased, and the supply of the pig is expanded first. It takes seven months for a pig to become a back-up pig to reach reproductive status, it takes about five months (114 days for pregnancy, 20 days for breastfeeding and 14 days for empty gestation) for a single pig to give birth, and it takes another one to two months for a single pig to be cared for and five to six months for to be fertile. It will take about 18 months to increase the supply of pig meat, from the refilling of the pig, so that the cycle of pigs will be about three to four years. The supply of raw pigs for the next six months can be extrapolated from the monthly pig stock。

The nature of the cycle of pigs is the supply-demand relationship, the demand-side is generally stable and key to supply. The country's environment, which is dominated by confederation farming, magnifies price volatility。

The demand side, which is long-term influenced by the income level of the population, population growth and consumption structure, is affected in the short term by seasonal eating habits, epidemics, food safety and alternative consumption effects. In recent years, the national average annual consumption of pork has been generally stable and has declined during the epidemic。

The supply side is characterized by cyclical fluctuations in pig farming, in addition to increased supply volatility due to policy interventions (environmental protection, financial subsidies, storage systems, natural disasters, etc.)。

The country's farming industry is predominantly agricultural, with a high level of homogeneity among producers, a low concentration of industries, a weak influence of individual producers on market prices and a greater likelihood of “up and down”, as well as anti-preventable techniques, insufficient funding and a higher degree of vulnerability, characterized by a more visible web cycle of pork prices。

In recent years, we have introduced a strategy of scale farming, which has encouraged the expansion of production capacity in farming plants, while at the same time reducing the size of the general farmer population, but the pattern of the relatively high share and low rate of scale farming has not changed. Scalable farming has a larger size effect than bulk farming and has greater managerial, technical and financial advantages, contributing to greater market stability and less blindness. As the process of urbanization accelerates, the rate of ageing increases, and there is a lack of financial resources and technology, so will the number of people in the diaspora shrink. According to the ministry of agriculture, the scale of pig production in 2020 was 57 per cent; the opinion on stabilizing the production of pigs for transformation upgrading, published by the state council office in september 2019, states that in 2022 and 2025, significant progress was made in the transformation of the pig production industry, with a marked improvement in the quality of the industry, with the rate of farm size reaching about 58 per cent and over 65 per cent, respectively。

Pork farming is in the middle of the chain, with the main upstream areas being cultivation, fodder, veterinary vaccine, etc. The downstream areas are mainly slaughterhouses and meat processing plants, with the total value of the chain exceeding $3 trillion, of which the value of farming is over trillion. There are currently two main models of pig farming, namely, “home-grown farming”, typical of the rangeland shares, and “corporate-farmers”, where the company provides support for pigs, feed, vaccine veterinary medicines and technicians, while the company is responsible for recycling the pig when it grows to the weight of the bar and for paying the farmers a surrogate price, such as the winge shares, the new hope, etc。

1. 2 volatility of pork prices is highly correlated with cpi

Historical data show the high correlation between the price volatility of pork in our country and cpi volatility, which is a key indicator for examining and predicting cpi fluctuations. From 2008 to date, the relevant coefficients for pork prices and the cpi index have been over 0. 8, much higher than for other commodities in the cpi basket。

The trend in the price of pork and its high correlation with the cpi is mainly due to the fact that pork accounts for a higher portion of the cpi basket. The share of pork in the cpi basket is currently about 2 per cent, and the share of pork as a single commodity is significant given that the total share of food commodities in the cci basket is about 30 per cent and that there are a large variety of commodities in the cpi basket. In addition, commodity prices for some commodities in the cpi basket, such as clothing and household appliances, are generally stable and less cyclical than for pork; other commodities, such as housing rental costs, have more volatile cycles than pork prices, making cyclical changes in pork prices more visible in the cpi and become important variables affecting the cpi。

The price of pigs in may 2022 was -21. 1 per cent per year, and the drag on the cpi is gradually diminishing, affecting cpi 0. 34 percentage points. After removing the price of pigs, the cpi stood at 2. 9 per cent。

1. 3 review of the four rounds of the pig cycle since 2006

Since 2006, the country has undergone approximately four rounds of the “pig cycle”, with the following main features: first, the length of the cycle is essentially three to four years, and the downtime is slightly longer than the lead time, with the main profit going down, but the willingness of the breeder to withdraw is weak as long as there is no loss; second, the per-pig cycle is accompanied by disease; and third, the reduction in the need for the availability of the high-capacity and fertile food column as a result of size and technological progress, will result in lower levels of storage than in the previous period。

The first round of the “pig cycle” lasted four years, from mid-2006 to may 2010, with an increase of 132. 6 per cent for the first two years and 2 for the next. The price of pork continued to be low at the beginning of 2006, leaving the pig farming industry at a loss. Some farmers suffered serious losses and were permanently withdrawn and a large number of pigs were eliminated. There was a 3. 6 per cent decrease in the number of piglets in 2006 and a 2. 6 per cent decrease in the number of piglets in 2006. After large-scale production was cleared, the number of raw pigs began to gradually reach the end of the pork supply. In 2007, there was a nationwide outbreak of highly pathogenic pig blue ear disease, slowing down the pace of refilling. As a result, the price of pork rose steadily from mid-2006 to an average of $18. 8 per kilogram in 2007 in 22 provinces and cities nationwide, an increase of 41 per cent over the previous year; combined with short-term factors such as spring festivals, the price of pork reached a high of $25. 9 per kilogram in march 2008. Since then, pork prices have begun to enter the lower lane. The outbreak of h1n1 in 2009 and food safety incidents such as thin meat and watered pork in 2010 have undermined public confidence in consumption, reduced demand in stages and further suppressed pork prices. In june 2010, the average price of pork fell to a low of $15. 5 per kg in 22 provinces and municipalities。

The second round of the "pig cycle" was held from june 2010 to april 2014 for approximately four years, with the first cycle from june 2010 to september 2011 being 15 months, with an increase of 98 per cent, and the next cycle from september 2011 to may 2014, with 32 months. This cycle is a relatively classic one for pigs, with prices driven mainly by during the cycle, with fewer external disruptions. Under the influence of the previous cycle, the stock of able-bodied pigs began to decline in 2009 and into 2010, with the impact on the availability of pork gradually beginning to appear and the price of pork starting to climb. In august 2010, the number of capable pigs dropped to 45. 8 million, a low point in the cycle. After 13 months, the price of pork rose to 30. 4 yuan/kg in september 2011. As the price of pork has risen, growing households have increased their stock of able-bodied pigs, and pork prices have again entered the lower road, continuing until the first half of 2013. To stabilize pork prices, in may 2013, three ministries, including the ministry of commerce, jointly launched a collection of frozen pork, boosting market confidence and restoring short-term prices. The price of pork went down again in 2014。

The third cycle runs from may 2014 to may 2018 and lasts for four years, with may 2014 to may 2016 as the first cycle, with an increase of 76. 6 per cent for two years, and may 2016 to may 2018 as the next cycle, with two years. At the end of 2014, the price of pork went beyond the bottom of the w-type and began to enter the rising zone. As a result of the strict environmental ban introduced in 2014 and the effort made to scale up the pig farming industry, a large number of scattered farmers have withdrawn from the market, and the storage of raw and fertile pigs has begun to enter a continuous downward pathway. The outbreak of the swine disease in the first half of 2015 has led to a reduction in the supply of pork and the price of pork up to may 2016. The cycle of pigs is characterized by environmental and scalding effects, and the price of pork does not lead to significant supplementation of the raw pigs. As a result of environmental repression and increased industrial efficiency as a result of large-scale farming, the single weight of pig production has been raised, while the number of pigs that can be provided by the pig can be increased, so there has been a steady decline in the pig's storage column, a slight 3 per cent increase in the second half of the pigting column in 2016, with no significant impact on the slaughter of the pig. The price of pork began to decline in mid-2016 and was completed in 2018。

The fourth cycle, mid-2022, spanning nearly four years, now has the “w” bottom. The current round of pork prices, influenced by a combination of factors such as african swine plague, environmentally limited production policies, increased kinetic energy within the pig cycle, and scalding, are characterized by large and fast increases, with prices rising at the highest level of successive pig cycles, or “super pig cycles”. Since the end of 2018, our stock of raw pigs has been declining steadily, reaching a historical low of -40 per cent in 2019 and driving a sustained rise in pork prices. The price of pork rose from $16/kg in 2018 to $56/kg at the end of 2019, representing a 250 per cent increase, the largest increase in successive pig cycles. At the beginning of 2021, pork prices continued to decline, with both “w” bottoms appearing, with the first detection of the “w” bottom of the current round in october 2021 and the second in april 2022。

2 outlook for the future: the pig cycle or the bottoming phase is in progress, and future increases depend on the degree of evaporation of production capacity

In our judgement, the second bottoming of the pig cycle in april 2022 is now, or has entered, the bottoming of the new pig cycle, as evidenced by the time pattern of denuclearization of production. It is expected that future price increases will be moderate, but without conditions for rapid and substantial upswing, and that future increases will depend on the degree of de-development of production capacity, owing to low and historically high levels of de-development。

From november 2021 to date, the price of pigs has reached the “w” bottom stage, with a steady margin and a narrow pull of the same negative. The average price of pork in 22 provinces rose from a low point of $18. 92/kg in april to $24. 21/kg on 1 july, an increase of 28. 0 per cent. The price of raw pigs also increased from $16,080 per ton at the end of april to $22,755 per ton on 4 july, an increase of 41. 5 per cent. In may, the price of pigs in the cpc was -21. 1 per cent per year, affecting cpc 0. 34 percentage points, the drag on the cpi is gradually decreasing, and the subsequent drag on the cpi is expected to continue to decrease。

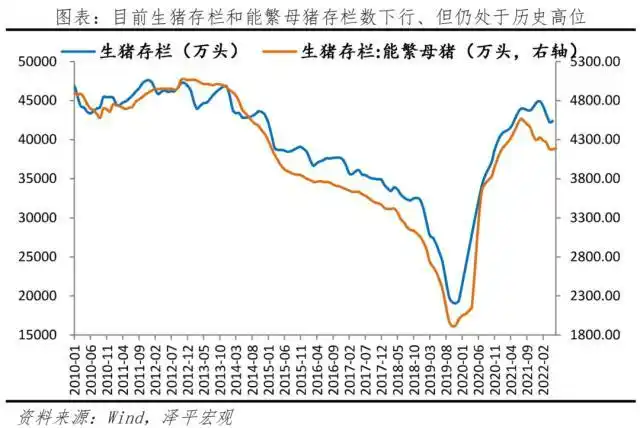

The production capacity is in the process of being decontaminated. The storage of raw and capable pigs has been at an all-time high since june 2021 and december 2022, respectively。

On the one hand, according to the time pattern of the pig cycle, it takes about 10 months to transfer the pig price to the pig price, which is mutually confirmed by the double-checking of the pork price in april this year. The pool of capable pigs fell from a high of 4. 56 million in june 2021 to 41. 92 million in may 2022 and to 8. 2 per cent in may. From 450 million head in december 2021 to 420 million head in april 2022, the ratio was -0. 2 per cent in april。

On the other hand, over a long time span, there has been a rapid recovery in the number of raw pigs in the last two years, reflecting historically high levels of capacity. The cumulative number of pigs produced in our country before 2018 was close to 700 million per year, with only 540 million and 520 million, respectively, in 2019 and 2020 under the influence of the african swine plague, leaving a gap of approximately 200 million. With the impact of a combination of factors such as the gradual alleviation of the african swine plague, the easing of environmental production restrictions, the increase in the price of the cycling of pigs, and the promotion of increased domestic farming, as well as the acceleration of capacity for large-scale mechanized farming, a total of 670 million pigs were born in 2021 and the annual gap was significantly reduced。

Over the coming period, the price of raw pigs will be observed mainly in the following three key variables:

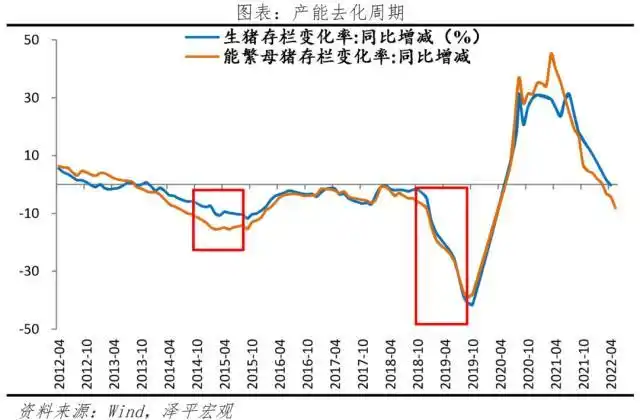

First, production capacity accelerates de-desired expectations. The current absolute amount of pig production capacity is at historical heights; both the absolute value of the field of pig production and the absolute value of the field of femininity are close to historical heights. There are currently about 420 million boars in storage (april) and 41. 92 million capable of keeping the pigs in storage (may), which is still close to the 2014 - 2015 height of the previous round。

In terms of historical pig cycles, the two rounds of pig cycles, which began in 2014 and 2018, have gone through a rapid decline in production capacity over two to three quarters before opening up prices. The year-on-year reduction in the capacity to produce the mother pig has been maintained for more than 20 per cent of the year, and the rapid evaporation of the capacity has created space for pig prices。

Two is the price of pig food. In spite of the current increase in pig grains, they remain low or have suppressed the willingness to expand productive capacity. In june 2021, the pig food ratio fell to 5 and entered the first warning zone. The subsequent low-level shock reached a minimum of 3. 93 (october 2021). As at 1 july 2022, the ratio of pig grains to 6. 63 had decreased, but remained at historically low levels. The relatively low food ratio of pigs erodes farm profits and is wary of the continued expansion of their production capacity。

Thirdly, the profits of large enterprises, the amount of pork sold, etc. Large enterprises such as the maharahara shares, the new hopes, the winnese shares and others are more viable in the pig cycle because of their own quantitative and technological advantages. In recent years, there has been an increase in the concentration of the pig farming industry over the previous round, with the ministry of agriculture showing a 57 per cent increase in pig farming by 2020. According to publicly collated data, the country's top 20 pig market share in 2021 was around 20 per cent。

At present, there is a new desire for the sale of 1,045,600 pigs, compared to 50. 8 per cent in the same year; the sale of 1,323,400 boars, compared to 38. 3 per cent in the same year; and the sale of 5,863,000 boars, compared to 89. 3 per cent in the same year。