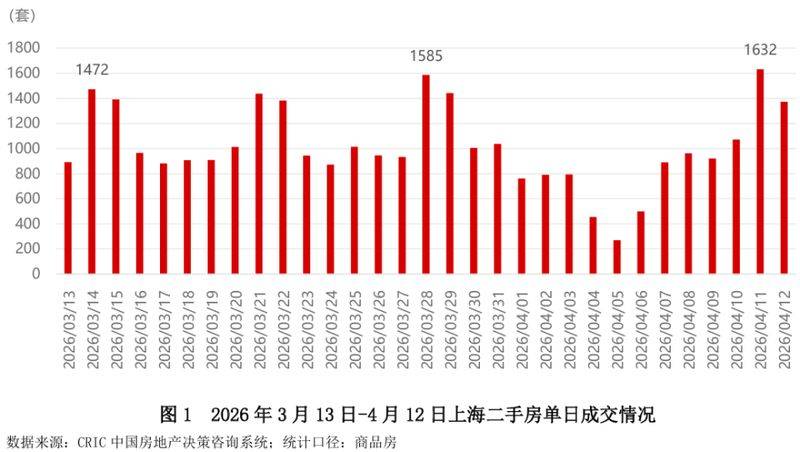

On 11 april, 1632 single-day nets were signed in shanghai, including commercial ones. This data not only updates the peaks of 1585 units on 28 march 2026 and 1472 units on 14 march, but also increases the number of single-day nets signed in shanghai for almost five years. From 1 to 12 april 2026, the used room in shanghai was put together on a network of 1,0409, an increase of over 2,000 over the same period last year。

Truth one: under the data sheet, “price-for-money” remains the core logic of the current market

The bursting growth of second-hand houses in shanghai during the current round is not a sign of a complete reversal of the market, but rather a result of the concentration of demand as a result of continued price adjustment, “price-for-money” being the core market feature。

According to kerry, in march 2026 the total number of second-hand houses in shanghai was 31436, of which 28,492 were second-hand, representing a significant increase of 178. 79 per cent in ring-to-rings, or 6. 0 per cent over the same period. However, the burgeoning turnover was accompanied by a continued downward trend in the average exchange price, which was $34429/m2 in march, a decline of 2. 85 per cent in the ring ratio and 16. 79 per cent in the same year, with a marked “price-for-money” pattern in the market。

Truth ii: just need to get to the bottom of it and improve transmission. Structural features are significant

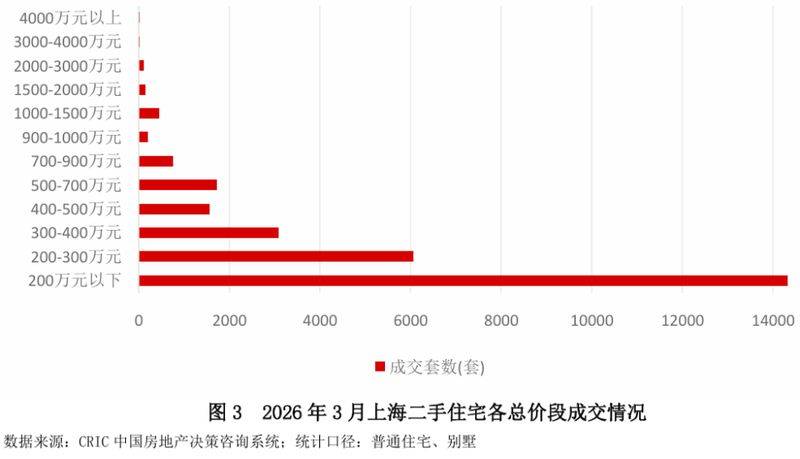

In terms of transaction structure, in march 2026, the largest number of second-hand homes in shanghai was sold at a total price of less than $2 million, at 14,326 units, or 50. 3 per cent, followed by 6058 units, or 21. 3 per cent, between 2 and 3 million yuan. Together, they account for more than 70 per cent of the total, with demand and change groups being the absolute mainstay of the current market。

Despite the initial need for basic disks, one sign of concern is that the trade-off ratio of high-end housing sources is increasing. Over the past two weeks, the trade-off ratio of high-end housing sources totalling more than $9 million has continued to rise, and the bargaining space for housing sources totalling between $7 million and $8 million has narrowed markedly. This suggests that, with the opening of the trade chain, part of the replacement funds began to be channelled to improved housing sources, and market heat was characterized by a bottom-up spread。

Truth iii: policy-driven super-supply contraction, and a phased rebalancing of supply and demand

The “seven” new deal, which landed on 25 february 2026, is a direct catalyst for the current situation. The reduction in the length of social security for non-resident housing from three years to one year, the increase in the amount of the provident fund loan line and the optimization of taxes and fees have precisely activated the suppressed demand and replacement demand. Following the fall of the policy, the mainstream brokering platform surged daily and doubled its visual value, with a backlog of rigid demands from the previous period being released centrally in march-april。

At the same time, continued contractions at the supply end have further amplified the condensation. The second-hand room in shanghai has been low nine months in a row, and the weekly number has been reduced by more than 20 per cent from last year's high point. On the one hand, the pre-existing stock sources were rapidly debilitated through price reductions; on the other hand, the upturn in the market caused some landlords to develop a sacrificial mentality and to suspend the listing. When the supply of quality housing is reduced and demand is concentrated in the market, supply and demand conflicts between the local core blocks are highlighted, thus contributing to high turnover。

Taken together, 1632 sets of used rooms in shanghai are sold on a daily basis, as a result of a combination of good policies, the release of demand, and the phased adjustment of supply and demand. It marks the restoration of market confidence and a return to liquidity, but it does not change the logic of long-term adjustment of the real estate market. In the short term, "quantitative parity" remains the dominant melody. Although the bargaining space for quality housing sources in some of the core blocks has narrowed, the market-wide average lacks the basis for a substantial increase. The market is still in the stocking phase, and the landlord's main claim remains rapid liquidity rather than a premium. For home buyers, the period of entry to the market remains, but the difficulty of “leaking” is increasing. At the same time, market segmentation will further intensify. Core sites, high-quality schools and sub-new housing sources will take the lead in stabilizing, or even making small increases, while non-core assets, such as remote suburbs, which are in short supply and no-school areas, will continue to face a longer cycle of decolonization。