In recent years, the share of new energy vehicles in passenger cars has been rising. According to press reports, by the end of 2024, the national holdings of new energy vehicles had reached 31. 4 million, with power cell loads leading globally for many years. Previously, as stipulated by the relevant departments, such as the ministry of industry and communications, since 2016, motor vehicle production enterprises have been required to provide at least 8 years or 120,000 kilometres of quality assurance for the core components of batteries, electric appliances and electrical controls。

This means that the first policy-enjoyed new energy vehicles have entered the “over-insurance period” and that more and more vehicle maintenance orders will be placed out of the official maintenance shop, and that the wind of new energy sales is coming with the “over-insured electric vehicles”。

The securities are believed to forecast that the market size of the new energy vehicle after sale will be $300 billion in 2025, of which “three electricity” will account for over 15 per cent and the corresponding market size is about $45 billion。

It's just that, in the face of the "overguarded tram, should the owner change the battery or the car? Who has control of the power to maintain the three powers? A shortage of service staff and the ability of the post-car market to catch the boe's “boiled wealth”

Year after year of insurance operations, supply and demand imbalances have increased

In the eight years from 2017 to 2024, there have been significant changes in the sales of new energy vehicles: the cumulative volume of 550,000 in 2017, 1. 05 million in 2018, 1. 08 million in 2019 and 1. 13 million in 2020 has been relatively flat。

In 2021, there was a dramatic shift, with sales jumping to 2. 91 million, which was more than 100 per cent over the same period of growth, thereby opening up a boom in the market. Over the following three years, 5. 31 million vehicles were sold in 2022, 7. 28 million in 2023 and climbed to 1,074 million in 2024。

Source: automobile services world

As can be seen, even if the warranty period were explicitly set at eight years, at least 500,000 new energy vehicles would be beyond the warranty coverage this year. Furthermore, it is expected that at least 1 million new energy vehicles will be insured each year thereafter. The year 2025 is expected to be a year of new energy insurance operations。

However, there is a growing contradiction between the rapid expansion of the size of the insured tram and the shortage of professional services。

According to the chinese association of automobile repairs, there are about 400,000 enterprises in the country that are involved in the maintenance of fuel cars, but only 20,000 to 30,000 new energy automobile repair businesses. A study by the f6 data research institute of 10,000 repair plants revealed further capacity gaps: only 2 per cent, or 200, of the repair plants with the capability to maintain the three electrical systems。

Thus, supply and demand imbalances directly push up maintenance costs。

For the time being, new energy maintenance operations are concentrated mainly on triple power maintenance, with a low rate of electrical failure and a central focus on software testing, electrical maintenance and battery maintenance. The current mainstream brand of new energy vehicles is known to vary significantly in battery costs, ranging from a minimum of 30 per cent to a maximum of 70 per cent and generally between 40 and 50 per cent。

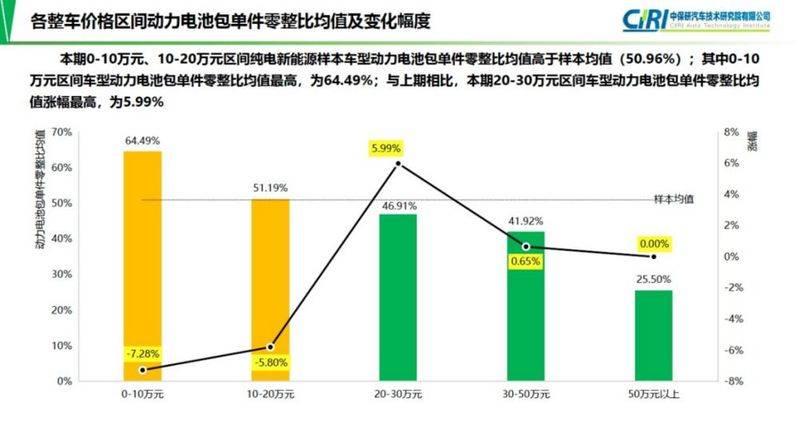

According to data from the central insurance institute, the average zero-sum ratio of new energy car-powered battery packages is 50. 96 per cent, which means that the price of a single unit is over half the value of the vehicle. In particular, the proportion of pure electric vehicles in the 0-100,000 dollar price zone is as high as 64. 49 per cent。

Source: central insurance institute

In this case, the cost of battery replacement is highly likely to exceed the residual value of the vehicle, resulting in a significant cost reversal. This also discourages many drivers from changing batteries。

Can the batteries be repaired? Industry engineers indicated that, with technological advances, the risk of repair itself had been significantly reduced. Successful maintenance, however, requires two key prerequisites: the need for the same type of spare parts to be replaced and the need to be carried out through regular professional maintenance channels。

This is due to the rapid and iterative technology of new energy vehicle batteries, and the differences in performance between old and new components may directly affect the overall performance of batteries. At the same time, battery maintenance has strict requirements for the operating environment, such as operating in a dustless workshop and accurately controlling the temperature and humidity of the workshop in order to prevent internal elements from corrosive after the battery has been wet and overloaded。

In this context, the market pattern of triple-dimensional protection is being reshaped and a diversified network of maintenance is being developed, focusing on mainframe plants, battery manufacturers, insurance companies and independent third parties。

Ii. The three equipment of the three equipment

Faced with the sale of hundreds of billions of new energy vehicles to protect the market, the four main factions competed to build technical barriers and commercial maps to try to gain core voice in the industrial transformation。

Specifically:

The mainframe plant maintains a technical closure: biadi constructs a nationwide “regional maintenance centre” that locks battery maintenance in its own system through a closed “replacement-replacement-recycling” chain; tesla and ideas bind users to the ultra-extension policy through a direct power centre。

This monopoly on core technology leaves the mainframe market in the market after sale, but also leads to a lack of bargaining power on the part of the owner when replacing or repairing battery modules, with a service premium much higher than that of third parties。

Battery manufacturers launched a reverse breakout: the ningde era, with 17 million installed units, introduced the “ninga service” level 3 system (direct camp centre - authorized shop - back-up centre). As of february 2025, there were 607 domestic networks in ninga services, of which 12 were battery rehabilitation centres covering major cities。

By virtue of its size, the ninde era is extending from b to c supply chains. However, the lack of uniform standards for re-manufacturing batteries has made it difficult to market and become a key bottleneck to their expansion。

Independent third-party growth: green start has quickly infiltrated the sinking market in the form of alliances, with over 1,000 outlets; rapid technology has been able to achieve the technological empowerment of 100 stores by self-studying diagnostic software; and assembling has been innovative in adopting the “shop-to-shop” model, embedding 4s stores, such as the medium-led group, for sharing spray resources。

However, although these agencies are keen to capture the need for expansive maintenance of the mainframe authorization system, they still face double constraints in terms of qualifications and technology。

In 2024, a case law of the district court of carting, shanghai, raised concern that masters of repairs, da liu and xiao liu, had been convicted of “breaching computer information systems” for “ unlocking” two locked new energy car batteries. This has further raised concerns among third-party after-sale agencies about the risks of new energy vehicle maintenance. In addition to legal risks, at the technical level, many new energy companies have limited vehicle maintenance at third-party workshops through technical means。

Unlike the first three active attacks, the insurance company is passive。

You know, high maintenance costs trigger a chain reaction, with the insurance market bearing the brunt. Data show that the average risk cost of new energy vehicles is 2. 2 times that of fuel trucks, with the combined cost rate industry average of about 107 per cent. In other words, insurance companies charge $100 to pay $107。

However, according to information published jointly by the chinese association of actuaries and the chinese bank of banks, in 2024 alone, our insurance industry has insured new energy vehicles with an overall loss of $5. 7 billion, with 137 departments with over 100 per cent payback. This means that it is almost impossible to earn money as long as the insurance company has insured the models in these systems。

Under the pressure of settlement costs, insurance giants had to build their own maintenance networks。

For example, under the chinese flag, the bang bang suit has introduced the “china psychiatry” chain, providing a one-stop service such as three power repairs and accident maintenance, and is now operational at the beijing flagship shop. In addition, the human security branch, in collaboration with the local 4s group, the sindar national trading automobile group, has also established a new energy car customer service centre for three charge maintenance, an integrated blow-out centre and a defined loss centre。

In addition, it is worth mentioning that the serial brands of “cats and dogs” (cats, troughs, kyotos) and “scrambling” are setting up three power lines in the “1+n” model. At this stage, however, these chains are generally based on the “burning one” model, with new energy operations more geared towards providing tires, washing light and protection services to c-end clients, and three electrical specializeds still waiting to be scaled down。

Iii. Multiple contradictions remain to be resolved, and the road to “freezing the car” is a long one

As we mentioned earlier, the high cost of maintenance of new energy vehicles has led many new energy owners to wish to retain the option of a maintenance channel。

One is to avoid price discrimination resulting from a monopoly on services. If repairs are made only by car operators, then consumers lose their bargaining space, and owners fear that even a small scratch may be forced to pay high fees at official maintenance points。

On the other hand, under pressure from competition in third-party maintenance channels, 4s stores are forced to improve the quality of their prices and services. Once the owner has no other option, it remains doubtful whether reasonable expectations of the length of maintenance, quality of service, etc. Will be taken into account by the company。

In addition to economic considerations, there are concerns about the risk of liability, given the fact that new energy vehicles are not open to third-party maintenance because of their technical barriers。

It is important to know that the “freezing of cars” of fuel trucks results from mechanical generality, i. E. That parts such as engines, gear tanks, etc. Can be dismantled and tested without the authorization of the enterprise, and that experienced third-party maintenance personnel need not rely on back-office data from the company or be able to be accurate。

New energy vehicles, on the other hand, are dominated by electronics and appliances, with different triple power systems and specific requirements for inspection equipment. For example, the electrical control unit requires a back-office authorization to unlock parameters, and unauthorized rewrites may trigger charge protection; battery bag dismantling must be decoded by the plant's equipment, otherwise the heat management security logic is compromised。

In other words, the operation of unofficial channels could undermine the original security logic of the system. In the event of an accident, the vehicle would have to prove itself to be defective in design. However, it would be impossible to distinguish between battery defects, data miscalculation or inadequate maintenance if left to third parties。

Thus, the multiplicity of claims by owners, firms, third-party repair plants and so forth, the “scramble” competition in the new energy vehicle maintenance market and the “freezing of cars” of the owners seem to have stalled。

Fortunately, at the policy level, efforts have been made to solve this dilemma。

In january this year, the general financial supervisory authority, the ministry of industry and information technology, the ministry of transport and commerce jointly issued the guidance on deepening reforms and strengthening regulation for the promotion of high-quality development of new energy vehicle risks (hereinafter referred to as the guidance), which focuses on reducing the cost of new energy vehicle maintenance。

The guidance notes the need to promote lower maintenance costs, to enrich the supply channels and types of parts and components for the maintenance of new energy vehicles, and to encourage the opening up of new energy automobiles and power cell enterprises to improve the maintenance economy of power batteries through technology. At the same time, capacity-building of new energy vehicle maintenance enterprises will be strengthened, maintenance and compensation standards will be improved and vehicle maintenance and compensation will be standardized。

In addition, in an interview with the media, zhang xuhui, secretary-general of the information branch of the chinese association for automotive maintenance, stated that the “hegemonic clause” was used by a car company to restrict the right of the owner to maintain the car by means of user agreement clauses (e. G., “blasting batteries is considered to be a waiver of quality assurance”). It was also argued that cars were often justified by “security” and “technical compliance”, but that the antimonopoly act prohibited abuse of market dominance to restrict competition。

In short, the current market for new energy maintenance is not fully into the dividend period, so neither battery plants nor mainframe plants nor third-party maintenance stores or insurance companies have yet developed a clear development system. However, it is foreseeable that this will be a vexing resort for multiple interests。