What is the tariff on imported vehicles?

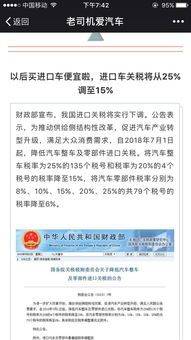

The tariff on imported cars is 15 per cent. According to the declaration of the state council committee on tariffs and tariffs on the reduction of tariffs on imports of whole vehicles and parts and components, the tax commission issues [2018] 3. Reduction of import duties on whole vehicles and spare parts. The vehicle rate was revised downwards to 15 per cent from 135 of 25 per cent and from 4 of 20 per cent

The rates of 8 per cent, 10 per cent, 15 per cent, 20 per cent and 25 per cent for vehicle spare parts were revised downwards to 6 per cent. The excretion of cars directly determines the excise tax of cars. The higher the car turnover, the higher the excise tax rate. There is a huge gap between excise taxes on large and small-scale vehicles. Tariff = expiry price x tariff rate; automotive import = basic tariff (15%) + consumption tax (3%-20%) + value added tax (13%)。

Import duties are duties levied by the customs of a country on imported goods and articles. Tariffs on imported cars increase the cost of imported cars, raise market prices for imported vehicles and affect the volume of foreign goods imported. As a result, countries impose tariffs on imported cars as a means of restricting imports of foreign vehicles。

What's the chinese auto tariff

[legal analysis]: china's motor vehicle import tariff is between 3 and 25 per cent. The tax price for imported vehicles is equal to 10 per cent of the tariff value for customs clearance, customs duties and excise taxes. The excise tax payable on imported vehicles is levied once at the time of import and is based on the excise tax as a tax price. Import duties are duties levied by the customs of a country on imported goods and goods and are a means of increasing government revenues and protecting the production of domestic goods. The imposition of import tariffs can increase the cost of imported goods and raise the market price of imported goods, thereby affecting the volume of imported foreign goods, so that countries use import tariffs as a means of restricting the import of foreign goods。

[legal basis]: article 36 of the regulations of the people's republic of china on tariffs and tariffs on imports and exports. Tariffs on imports and exports are levied in ad valorem, in quantitative or otherwise prescribed by the state. The ave formula is: taxable = taxable price x tariff rate, and the ave formula is: taxable = quantity of goods x unit tax

Tariffs on imported vehicles

[legal analysis]:

The vehicle import tax is 25 per cent as per our legislation。

[legal basis]:

In accordance with the provisions of the provisional consumer tax regulations of the people's republic of china, only four categories of goods are currently subject to excise taxes。

Category i: special consumer goods, such as tobacco, alcohol, firecrackers, fireworks, etc., which are harmful to health, social order and the environment。

Category ii: non-living necessities such as luxury goods, such as precious jewellery and jewellery stones, cosmetics and skin protection。

Category iii: high-energy consumption of high-end consumer goods such as sedans, motorcycles。

Category iv: non-renewable and alternative consumer petroleum products such as petrol, diesel。

Regulations of the people's republic of china on import and export tariffs

Article 2. Goods and goods imported or exported by the people's republic of china shall be subject to customs duties and customs duties in accordance with the provisions of these regulations, except as otherwise provided in laws and administrative regulations。

"sweet tip."

The answer is that the current information is based only on my own understanding of the law

If you still have questions about this issue, please collate the relevant information and communicate with professionals in detail。

Tariffs on imported vehicles

Calculation of the rate of tax on imported vehicles: tax-based price = tariff-completed price, customs duty, excise tax-based price x 10 per cent. Acquisition tax = tax rate x tax rate (which is lower than the lowest tax rate issued by the state tax administration and is charged at the minimum tax price established by the state tax administration). Self-utility rate: iff x 10 per cent, in which iat is not included。

Article 4 of the vehicle acquisition tax act

The rate for vehicle acquisition tax is 10 per cent。

Article 5

Taxable taxes on the acquisition of vehicles are calculated at the tax rate multiplied by the tax rate of the taxable vehicle。

Article 6

The taxable vehicle price is determined in accordance with the following provisions:

(i) the taxable price of the taxpayer's own taxable vehicle, the full price actually paid by the taxpayer to the seller, excluding vat

(ii) the taxable price of the taxpayer's own vehicle imported for tax purposes, plus customs duties and excise duties for the price of customs duties

(iii) the tax price of the taxpayer's own taxable vehicle is determined on the basis of the sale price of the taxpayer's own taxable vehicle, excluding vat

(iv) the taxpayer obtains, by gift, award or otherwise, the taxable price of his own vehicle, which is determined on the basis of the price specified in the certificate at the time of acquisition of the taxable vehicle, excluding vat tax。

"sweet tip."

The answer is that the current information is based only on my own understanding of the law

If you still have questions about this issue, please collate the relevant information and communicate with professionals in detail。

What's the rate on imported cars

Legal analysis: i. Tariff on imported vehicles at 15 per cent

According to the ministry of finance, from 1 july 2018 on 1 july 2018, duties on the import of automobiles and spare parts were reduced. Reduced the tax rate to 15 per cent for 4 tax points with a total rate of 25 per cent and 135 tax numbers and 20 per cent. Tax rates for vehicle spare parts were reduced to 6 per cent for a total of 79 tariff lines of 8 per cent, 10 per cent, 15 per cent, 20 per cent and 25 per cent, respectively。

Value added tax at 13 per cent

The country's earliest vat was 17 per cent, which was revised to 16 per cent in 2018, and from 1 april 2019, the vat was reduced from 16 per cent to 13 per cent。

The excise tax shall be:

1 1 per cent of emissions below 1. 0 litres (including 1. 0 litres)

2. 3 per cent of emissions of more than 1. 0 litres to 1. 5 litres, including 1. 5 litres

3. 5 per cent of emissions above 1. 5 litres to 2. 0 litres, including 2. 0 litres

4. Emissions of more than 2. 0 litres to 9 per cent of 2. 5 litres (including 2. 5 litres)

Emissions above 2. 5 litres to 12 per cent of 3. 0 litres, including 3. 0 litres

6. 25 per cent of emissions above 3. 0 litres to 4. 0 litres, including 4. 0 litres

7. 40 per cent above 4. 0 litres。

Legal basis: customs law of the people's republic of china

Article 56 goods imported or exported, goods imported or exported, reduced or exempted from customs duties as follows:

(i) advertisements and samples of no commercial value

(ii) material made free of charge by foreign governments and international organizations

(iii) goods damaged or lost before customs release

(iv) items up to a specified amount

(v) other goods, goods and services which are subject to reduced and exempt from customs duties by law

(vi) goods and goods which are subject to reduction or exemption from customs duties under international treaties concluded by or to which the people's republic of china is a party。

Article 57. Imports and exports of goods in specific areas, enterprises or for specific purposes may be reduced or exempted from customs duties. The scope and methods of specific tax deductions or exemptions are determined by the state council。

Goods imported in accordance with the preceding paragraph, which are subject to reduction or exemption from customs duties, may only be used in specific areas, enterprises or for specific purposes, and may not be diverted without customs authorization and payment of customs duties。

Article 58. Temporary reduction or exemption from duty beyond those provided for in articles 56 and 57, paragraph 1, of this law shall be decided by the state council。

Article 59 goods imported or temporarily exported by customs with the approval of the customs authorities, as well as specially authorized bonded goods, are granted a temporary exemption from customs duties after the shipper of the goods has paid a bond equivalent to tax or provided guarantees to the customs authorities。