In march 2023, a county tax authority proposed to liquidate land value added tax (vat) on real estate projects developed by a real estate development enterprise (general taxpayer) within the jurisdiction, which provided the following information:

(1) in september 2018, a land use title was obtained from the government in the amount of $360 million, and a tax on the payment of the deed was paid, with 50 per cent of the concession area being spent on the construction of the real estate project。

(2) construction started in april 2019, with a development cost of $60 million, which includes $6 million (invoices issued by the construction company) for the maintenance of the quality insurance fund that has not yet been paid to the construction enterprise, $9 million for the renovation and $5 million for the development of the supporting kindergarten, the ownership of which belongs to the owner。

(3) 30 million yuan (us$ 20 million at the same time rate of interest on loans of the same kind by commercial banks) for the interest of microcredit companies that can be apportioned on the basis of the transfer of real estate projects。

(4) the real estate project was completed and accepted in october 2022 and, as of february 2023, the project had sold 80 per cent of the marketable building area, with a total of $480 million in tax-free revenues, and 10 per cent of the marketable building area was donated to the good employees of the enterprise。

(5) the enterprise has paid an advance value added tax of $10. 8 million on land。

(other relevant information: 3 per cent tax rate applicable locally; 5 per cent deduction from real estate development costs by the local provincial government when interest expenditure can be certified as a loan from a financial institution; $3. 12 million tax and surcharges allowed in relation to the transfer of property

Requests:

On the basis of the above information, the answers to the questions are based on the following serial numbers and, if calculated, the totals。

(1) a brief statement of the reasons why the tax authorities may require taxpayers to settle the value added tax on land。

(2) calculates the amount of the acquisition of land tenure payments allowed in the liquidation of the enterprise。

(3) computes the sum of the value added tax (vat) that the enterprise is allowed to deduct from the project amount。

(4) the amount of taxable income to be recognized in the calculation of the enterprise's value added tax on the liquidation of land。

(5) land value added tax (vat) shall be added to the calculation of the value added tax (vat) on the liquidation of the enterprise。

(1) since 80 per cent of the project's marketable building area has been sold abroad and the remaining 10 per cent is given to employees, which is considered as a sale, equivalent to 90 per cent of the project's completion, the competent tax authorities may require the taxpayer to liquidate。

Note: cases in which the tax authorities may require taxpayers to liquidate the value added tax on land:

1 real estate development projects that have been completed and accepted, with the transferred real estate building area accounting for more than 85 per cent of the total project area available for sale, or not more than 85 per cent, but the remaining marketable building area has been leased or used for its own use。

2 sales (pre-sale) licences have not been sold for three years。

3 taxpayers apply for the cancellation of tax registrations without processing the liquidation of land value added tax。

4 other cases stipulated by the provincial tax authorities。

(2) the amount allowed to be deducted from the enterprise's land value-added tax = 36,000 x (1+3 per cent) x 50 per cent x 90 per cent = 166. 86 million yuan。

Note:

Taxes paid by real estate development enterprises to acquire land tenure should be included in the amount paid to acquire land tenure。

The amount paid for access to land needs to take into account the proportion of development (50 per cent) and sales (90 per cent)。

(3) real estate development costs allowed to be deducted = 6,000 x 90 per cent = 5. 4 million yuan。

Allowed deduction for real estate development costs = 2,000 + (16,686 + 5,400) x 5 per cent = 3,104. 3 million dollars)

Total amount allowed to deduct project amount = 16,686 + 5,400 + 3 104. 3 + 312. 12 + (16,686 + 5,400) x 20% = 29,919. 62 (millions of dollars)

Note:

1 where the construction construction firm invoiced the real estate development firm for quality assurance payments, deductions are made for the amounts contained in the invoices; no invoices are issued. Invoices have been issued and may be deducted。

(b) public facilities developed by the real estate development enterprise to accompany the liquidation project are owned by all owners and the costs and expenses may be deducted。

Taxpayers are allowed to deduct real estate development costs = interest + (the amount paid for acquisition of land tenure + the cost of real estate development) x 5 per cent if they are able to provide proof of loans from financial institutions for interest expenditures. The “interest” in the formula cannot exceed the amount calculated at the interest rate of the commercial bank for the same period. Since the interest charge is calculated at the same interest rate as the commercial bank's loan for the same period, at $20 million, less than $30 million, the formula is used at $20 million。

(4) amount of taxable income to be recognized in the liquidation of the enterprise's land value added tax = 48,000 ÷ 80% x 90% = 54,000

Note: ten per cent of gifts to employees of the enterprise also need to be treated as sales and as taxable income from land value added tax。

(5) value added = 54,000-29 919. 62 = 24 080. 38 (thousands of dollars)。

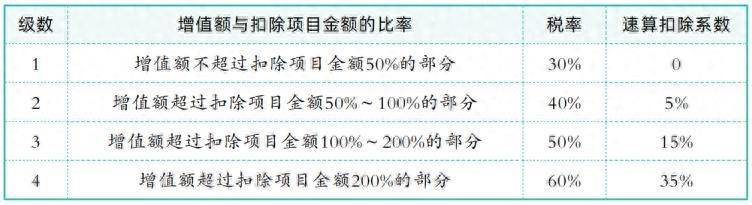

Value-added rate = 24 080. 38 ÷ 29 919. 62 x 100% = 80. 48% with applicable tax rate of 40% and speed deduction factor of 5%。

Land value added tax payable = 24 080. 38 x 40%-29 919. 62 x 5% - 1,080 = 7,056. 17 (millions of dollars)

Note: when land value added tax is liquidated, the amount of prepaid tax shall be deducted。

On 1 november 2022, a pharmaceutical plant transferred an office building located in the city, receiving $252 million in taxable revenue. When the building was built in 2011, a sum of $60 million was paid for land tenure, at a cost of $80 million. Following an assessment by the real estate assessment body approved by the government at the time of the transfer, the replacement cost of the building was determined to be $160 million, representing a 60 per cent depreciation rate。

(other relevant information: the stamp duty rate on which the transfer of title is based is 0. 5 per 1,000; the local government provides for additional deductions for local education; and the transfer of office buildings is subject to simple taxation

Requests:

On the basis of the above information, the answers to the questions are based on the following serial numbers and, if calculated, the totals。

(1) the assessed price of the enterprise's office building when calculating the land value added tax。

(2) indicate the reason why the plant may choose a simple tax method。

(3) the tax deductions allowed for the calculation of the land value added tax and the surcharges。

(4) the total amount of the project amount is allowed to be deducted when calculating the land value added tax。

(5) calculation of land value added tax due on the transfer of office buildings。

(6) reply to the time period within which the pharmaceutical plant may file a tax on land value added tax。

(1) evaluation price of the enterprise's office building = replacement cost x discount rate = 16,000 x 60 per cent = 96 million yuan

(2) the general taxpayer transfers his own immovable property built before 30 april 2016, with the option of a simple tax method, which was built in 2011 as an old real estate project and is applicable。

(3) vat tax payable = 25,200 ÷ (1+ 5%) x 5% = 12 million。

Urban maintenance tax payable = 1,200 x 7 per cent = 84 (million)

Payable for education plus local education plus = 1,200 x (3 + 2 %) = 60 (million)

Stamp duty payable = 25,200 x 0. 5 per thousand = 12. 6 per thousand dollars

Allowed tax deductions and attachments = 84+60+12. 6 = 156. 6 (millions of dollars)

Note:

1 the general taxpayer sells self-built real estate in order to obtain the full price and extra-price costs as sales。

Since the building is located in the urban area, the applicable municipal maintenance tax is 7 per cent。

(4) total amount allowed to deduct the amount of the project = 6,000 + 9,600 + 156. 6 = 15,756. 6 (thousands of dollars)。

Note: deduction items for transfer of storage units include:

1 estimating prices of houses and buildings。

2 amount paid for acquisition of land tenure。

3 tax payments at the transfer chain。

The cost of construction is not subject to deduction, which is a condition of interference。

(5) value added = 25 200-1 200-15 756. 6 = 8,243. 4 (millions of dollars)。

Value added = 8,243. 4 ÷15,756. 6 x 100 per cent = 52. 32 per cent, with applicable tax rate of 40 per cent and speed deduction factor of 5 per cent。

Land value-added tax due on transferred office buildings = 8,243. 4 x 40 per cent 15,756. 6 per cent = 2,509. 53 (millions of dollars)

(6) within seven days of the conclusion of the contract for the assignment of real estate, the taxpayer shall file a tax declaration with the competent tax authority in the place where the real estate is located。

An industrial enterprise located in the city is a general vat taxpayer and owns an office building purchased in march 2016 within the city. It is known that the building was purchased without a separate payment of the land price, with an office price of $30 million (including turnover tax) indicated on the purchase invoice and a tax amount of $1. 5 million indicated on the tax clearance certificate. The assessed price, now confirmed by the local tax authorities, is $35 million. In march 2023, the industrial enterprise sold the building for the purpose of collecting funds, obtaining a total price tax of $61. 5 million, at which time the value added tax and surcharges were paid, and the local government provided for an additional deduction for local education。

(other relevant information: it is known that the enterprise sells office buildings on a simple tax basis, regardless of stamp duty and other unspecified taxes

Requests:

On the basis of the above information, the answers to the questions are based on the following serial numbers and, if calculated, the totals。

(1) value added tax (vat) payable by the enterprise for the sale of the office building。

(2) the calculation of taxes relating to the transfer of real estate is permitted when the office building is sold。

(3) when calculating the sale of office buildings, deductions are allowed for the total amount of the project。

(4) calculation of land value added tax due on the sale of office buildings。

(1) vat tax payable = (6,150-3000) ÷ (1+5%) x 5% = 1. 5 million。

Note: where taxpayers transfer real estate acquired before 30 april 2016, using a simple tax method, vat uses a differential tax method to allow deduction of the price at the time of acquisition of real estate。

(2) urban maintenance tax, education fee surcharge and local education fee surcharge = 150 x (7 + 3 + 2 %) for the transfer of real estate = 18 (million)。

Deductible tax related to transfer of real estate = $18 000

Note: in the case of transfers of real estate stock, where price assessment cannot be obtained, the amount of tax paid on the purchase of the property is granted to be deducted as “tax related to the transfer of real estate”. The transfer of old houses in this topic has been evaluated at an assessed price, which in fact includes the amount of the tax, and is therefore no longer subject to deduction。

(3) the transfer of old office buildings allows the deduction of old buildings and buildings at an assessment price of $35 million。

Total permitted deduction = 18 + 3,500 = 3,518 (million)

(4) value added = 6,150-150-3 518 = 2482 (million dollars)。

Value-added = 2,482÷3,518 x 100% = 70. 55% and applicable tax rate of 40% and speed deduction factor of 5%。

Land value added tax payable = 2,482 x 40 per cent - 3,518 x 5 per cent = $816. 9 (million)

Note: taxpayers who transfer old houses are unable to obtain evaluated prices, but who are able to provide an invoice for the purchase of the house may be deducted by adding 5 per cent per year from the date of purchase to the year of transfer. The assessed price has been obtained in this issue and is therefore not subject to deductions based on the amounts contained in the invoices。