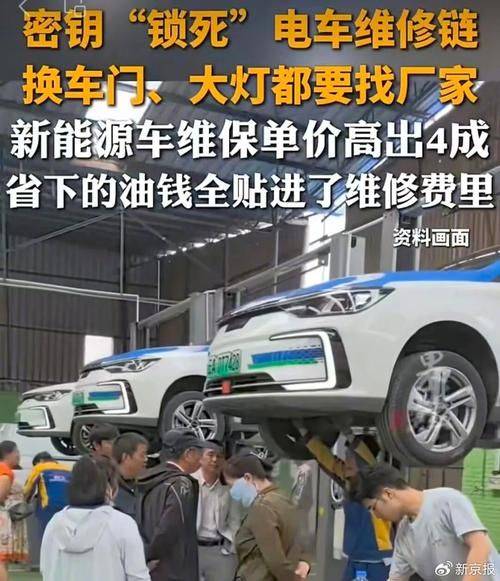

> many new energy car owners have experienced this experience: battery alarm lights are on, and the solution offered by 4s is usually “to change a whole battery package”, offering a price of 560,000, or even 100,000. The source of the problem, however, is not how expensive the battery itself is, but the monopolistic closure of the technology, parts and services surrounding battery maintenance. Behind this is a clear business account:** the company and 4s turned after-sales maintenance into a highly profitable “cash cow” rather than a technology-driven service business. ** dismantling the profit logic of “no fix”: the business in a battery bag, in order to understand the cost of repairing new energy vehicles, has to open the collection structure for battery maintenance. Prior to the introduction of the 2026 new regulations, ** more than 75 per cent of battery failure ** — e. G., ageing of individual cores, poor line contact — could be technically resolved through several hundred to thousands of dollars of electrical core level maintenance. However, after-sale models of “replacement only” have been introduced in a uniform fashion between the car company and the 4s store, which has forced the failure into tens of thousands or even hundreds of thousands of dollars for overhaul. The business logic of this model is very clear. According to the chinese association for car circulation, ** after the sale of new energy distributors in 2025, the māori contribution was as high as 37. 1 per cent**, much higher than 26. 5 per cent of new car sales. This means that the profits from the sale of vehicles are becoming less and that the real profits are at the core of the repair and distribution of spare parts, especially after the sale of the three power systems (batteries, electric appliances, electrical controls). It is more immediate and effective to hold this high-māori base disk than to enhance the technological competitiveness of the vehicle itself. Its cost model also implies amazing profit margins. The cost of battery packs in the mainstream pure-truck type is about 50 per cent of the total vehicle cost, but under the “replacement only” model, the overall replacement cost following the failure is almost equal to the total vehicle price. The difference behind this is essentially obtained through monopoly pricing. (blockview://markdown-image-tos-cn-i-tt/fc719114dfabf496295c2c5b5b51263db0) 4s store was able to require the owner to pay the entire package for a small module failure because it firmly controlled the entire chain from the supply of accessories to the maintenance of data. If the “technical barriers” to the three power systems are the result of “replacement only”, then the technological blockade of batteries, electric power and electrical control systems by the car companies is the moat that underpins this monopolistic business model. Three barriers have been built through closed inspection systems, locking technical clearances and encrypted data ports. ** during the period 2024-2025, there were even cases of car mechanics being considered “crimes against computer information systems” because of the modification of battery management systems (bms) to allow third-party car repairs to be considered “high-risk occupations”.** this set of barriers directly cut off normal competition in the market. In the country, there are approximately **4 million ** fuel vehicle protection enterprises, compared to only **20,000 to 30,000 **, of which only **2 to 3 per cent are closed shops that actually have the capacity to maintain the three power systems.** (blockview://markdown-image-tos-cn-i-t/2ff05205824a2bb2b9d4f4e74ccad0c1) at the same time, third-party manufacturers are reluctant to produce core parts because of insufficient market demand and high modelling costs, and the owners of closed-car companies are even caught in the “unofficial sale, non-compliant parts, no uniform standards”. New breaking bureau: business logic is being forced into the interim scheme for the recycling and integrated use of used and end-of-life power batteries in new energy vehicles, which became operational on 1 april 2026, as a forced breakdown of the above-mentioned commercial model. The core of the new regulations was not technological upgrading, but the opening of markets. It makes it compulsory for car operators to open battery dismantling parameters, maintenance manuals, core coded data to compliance third-party maintenance agencies, and allows for separate maintenance of the core and replacement of the failure module. This cuts off the huge profit space under the “repackage” model. Following the break-up of the “replacement only” model,** the cost of maintenance for minor malfunctions will be reduced from tens of thousands to hundreds of thousands of yuan, with a reduction of more than 80 per cent**. ! (blockview://markdown-image-tos-cn-i-t/909d96253f6b403591315fd39bf2116) for example, a battery bag of $80,000 would have to be replaced for damage to one of the power cores, and the new regulation would have to replace the failure module at a cost of only around $5,000. In addition, the new regulations specify that used batteries that have been replaced are owned by the owner of the vehicle, that the store is required to announce the recovery price, and that the owner may deduct the maintenance fee at market rates up to **50 per cent**. This means that part of the residual value of the old battery, which was originally monopolized by the 4s, returned to the owner. Post-market patterns have been reshaped: from “monopolization” to the fall of “precision” new rules, the new energy vehicle post-market will shift from a closed system that relies on technological barriers and a monopoly on accessories to an open market where compliance third parties participate and earn reasonable profits through fine-tuning maintenance and market-based competition. In the future, the industry will develop a pattern of competition between professional three-power maintenance centres and chains of brands, which will further reduce maintenance costs, according to guo hongbo, managing director, beijing energy management limited. At the same time, the power cell recycling industry has also embarked on the path of scale and standardization. ** the size of the formal power battery recycling market is projected to exceed $80 billion in 2026,** with a compound annual growth rate of over 25 per cent. Between april and june 2026, the five departments jointly launched a special overhaul exercise, which focused on the screening and clearance of a large number of non-compliant small workshops, ending the “dispersion, chaos and small” of the industry. **conclusion:** from a commercial point of view, the “maintenance” of the new energy vehicle is not technical in nature, but is due to the fact that, through the monopolization of technical data and spare parts, it creates a high-barrier and profitable “independent profit centre”. The implementation of the new regulations of 2026 was in essence the forced dismantling of the moat at the legal level, returning the maintenance market to the commercial nature of “technology creation”. For the owner, this means that the “affordable, unrepairable” dilemma is coming to an end; for the entire industrial chain, it is a profound shift from “monopoly” to “competence”。