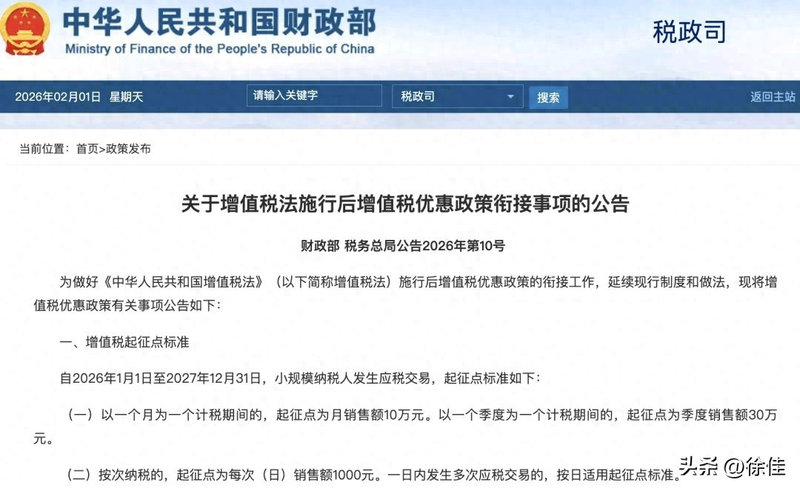

On 31 january 2026, the ministry of finance and the general state tax administration officially issued the proclamation on the post-vat policy convergence of vat preferences, which synchronizes the rules of operation for the administration of vat, clearly defining the point of entry, the scope of application and the calibre of implementation. This is not a temporary subsidy or a short-term adjustment, but rather a regularized reduction arrangement for small-scale taxpayers, self-employed businessmen and flexible workers following the formal introduction of the vat act, with a policy implementation period that is clear until the end of 2027, when it is given to micro-entrepreneurs。

Many people who heard of the “value-added tax starting point” felt that it was a professional fiscal vocabulary that had nothing to do with themselves, but that policy was directly related to the income of street shops, internet vendors, marketers and freelancers. To put it simply, the core of the new deal is that business earns less than $100,000 a month, less than $300,000 a quarter without vat, and that individuals occasionally take orders and work without paying less than $1,000 a month. In the most straightforward way, the policy leaves tax dividends to the lowest-level operators, making small businesses easier and flexible employment more secure。

This document is based on the official announcement and authoritative interpretation of 31 january 2026, in which the policy points, the population groups to be applied, the methods of operation are explained in great white language, not in terms, not in terms of exaggerating effects, not involving negative cases, but in the delivery of real and accessible information to help every common operator understand and use the new deal。

First, the most critical figures are the criteria that can be used directly by all. The new deal is clear that between 1 january 2026 and 31 december 2027, the vat entry point for small taxpayers is implemented in two cycles: monthly taxes with no vat on sales of up to $100,000 per month and quarterly taxes with no vat on sales of up to $300,000 per quarter. In the case of natural persons who do not do business regularly and occasionally provide services, the starting point for sub-taxation is raised to $1,000 per day, and the tax is not paid under the standard, depending on the combination of more than one day of income。

As a comparison of previous policies, the new deal is not simply a continuation, but rather a legal-level preference, with the inclusion of cost-cutting measures that have worked well in practice as part of the bridging rules, with more stable implementation and clearer expectations. In the past, many small businesses have feared a change in policy from one year to the next and are afraid to plan for the long term. It is now clear that for two years, the opening of businesses, the acquisition of goods and the expansion of businesses will be more robust。

In terms of population coverage, three groups have benefited most. The first category consists of individual businesses, including restaurants, convenience stores, garment shops, barber shops, repair shops, etc., which are not subject to vat as long as their monthly turnover is not over $100,000, and the money saved can be used for renovation, purchase, payment of wages and direct upgrading of their operations. The second category consists of small-scale enterprises, mainly micro-enterprises, consulting services, design studios, and small electronics stores, which are small-scale and less risk-resistant, and where exemption from vat can significantly reduce operating costs and channel funds towards business expansion. The third category consists of flexible employment and natural persons, including designers, photographers, tutors, repairers and part-time billers, who are exempt from taxes of less than $1,000 a day, so that the income from flexible employment is more effective and no extra taxes are levied on small incomes。

According to data from the national tax administration, the share of small-scale taxpayers in total vat is over 80 per cent nationwide, with a very high percentage of the total monthly sales of less than $100,000. This means that the vast majority of micro-entrepreneurs benefit from the tax-exempt dividend when the new deal landfalls, without having to calculate taxes and declare taxes for a small amount of income and with a marked reduction in operating pressure。

A lot of people would ask, "what's the sales? Do you think you'll get more than that?" the new deal gives a clear calibre, which is based on the amount of sales without taxes, that is, the actual income after the deduction of vat. In the case of partial deductions and deductions, the deduction is calculated on the basis of the balance, which is not duplicative and overestimated to ensure that the criteria are fair and reasonable. At the same time, the new deal makes it clear that all taxpayers who have multiple taxable transactions such as the sale of goods, the provision of services, etc., are exempt from taxation by combining sales, provided that the sum is not excessive。

There is also a practical detail that the new deal optimizes the rules applicable to natural persons. Whereas in the past, individual rentals, occasional sales of home-made products, etc., were only subject to the secondary 500 yuan standard, it is now clear that six specific categories of cases can be applied directly to the monthly rate of 100,000 yuan, e. G., personal rental property, sale of home-made agricultural by-products through a formal platform, etc., by reference to scheduled taxes. This adjustment allows long-term, stable natural persons to enjoy the same advantages as individual business owners and is more in line with the actual business situation。

The new deal also has humanized arrangements for operators who need to be billed. If a small taxpayer does not reach the starting point, it may choose to waive tax exemption and issue specific vat invoices to facilitate customer demand for credit; at the same time, it is made clear that a small taxpayer does not have a 36-month limit on the waiver of preferences and is flexible in the light of business needs, taking into account the need for tax exemption and without prejudice to normal business cooperation. This rule breaks the previous limitation that “abdication cannot be restored easily” and makes micro-entrepreneurs more autonomous and convenient。

In addition to entry-point preferences, the new deal simultaneously identified a number of preferential duty-free schemes, and the entry-point policy created a multiplier effect that further reduced the burden. For example, agricultural producers are directly exempt from vat for the sale of their own produce, academic education services, old-age care services, medical services, wholesale and retail books, and mass cultural sports services. Most of these areas are livelihood-related, micro-business-related, and tax-free policies have made the cost of livelihood services more stable and the income of operators more secure。

In the case of community-based old-age and nursing services, institutions provide services free of value-added tax, which can reduce operating costs and make fees more pro-people; farmers sell their own vegetables, fruits and foods free of value-added tax, which directly increases farmers ' income and contributes to rural industrial development; bookstores, cultural houses and sports stadiums are tax-free and can better provide public cultural services and enrich public life. Taxes on entry points plus on livelihood projects, with double dividends covering production, life and services, are truly productive and sustainable。

Another important aspect of the new deal is to achieve a smooth transition after the implementation of the vat act, maintaining tax stability and policy continuity. On 1 january 2026, the vat act entered into force, marking a new phase of rule of law and regularization of the vat system. At the key points of the new law, the ministry of finance and the directorate-general of tax administration have been quick to issue a bridging bulletin that clearly defines the continuity of preferences, the harmonization of calibres and the simplification of operations, avoids policy gaps, does not increase the burden on the operator, and reflects a steady expectation and the policy orientation of the subject。

At the macro level, steady micro-businesses are employment, livelihood and consumption. Individual entrepreneurs and micro-enterprises are important vehicles for employment, with more than 300 million people being employed by individual entrepreneurs nationwide. Reducing operating costs through vat tax exemptions allows small businesses to survive and live well, thereby stabilizing jobs, increasing income for the population, boosting consumption and creating a virtuous cycle. The new deal, which appears to be a tax adjustment, is the foundation for a stable economy and a livelihood, the effects of which are felt directly in every shop and every operator。

The new deal also achieved negative efficiency gains for grass-roots administration. Increases in the number of entry points and exemptions have resulted in a large number of small taxpayers not having to make vat declarations, pay taxes and reduce the cost of completing statements, sending information and running legs. The tax authorities simultaneously optimize the functions of the e-tax office, the mobile phone tax app, the automatic identification of systems eligible for tax exemption, and the automatic simplification of the process so that the tax is as simple as payment for mobile phones. Policies both reduce the burden on operators and reduce the cost of regulation to achieve win-win results。

Many operators care how to make sure they can enjoy it or not. The official rules of administration provide a clear answer: small, eligible taxpayers are automatically granted tax exemptions at the time of filing, and are entitled to a normal declaration without additional approval or documentation. In the case of sub-taxed natural persons, at the time of billing or declaration, the system is automatically awarded at the rate of $1,000, without direct exemption from taxation at the point of entry, and can be completed on a full-way basis and in a few minutes。

In order to make the policy more effective, local tax authorities provide targeted counselling, bringing the policy to the door of a small shop and to the operator through community announcements, business twitter groups, guidelines for tax halls, short video presentations, etc. There is no need for complex fiscal knowledge, but it is a matter of keeping in mind that “up to 100,000 per month, less than 1,000 per month, are exempt” and enjoy a dividend。

In the long term, vat systems will be fairer, simpler and more inclusive. The steady continuation of the policy of entry points reflects the firm attitude of the state in favour of micro-business and the protection of grass-roots entrepreneurship. In the future, as the level of digitization increases, the tax processing process will be simpler, more accessible and more accurate in terms of policy implementation, allowing every man who does business to be less concerned and more profitable。

For ordinary people, the benefits of this policy are visible and felt. Small businesses have less expenditure per month and more profitable profits; part-time jobs, small incomes are tax-free and labour returns are more real; when they are consumed, commercial costs are lower and prices of goods and services are more stable. Policies do not only target operators, but ultimately benefit every consumer, every family。

Market dynamics are gradually emerging after the new deal has landed. Many small businesses indicated that the tax exemption policy provided them with more funds to upgrade equipment, upgrade services and recruit staff, while flexible workers said that small-scale payments were tax-free, making part-time income more secure and more willing to try and increase income. These minor changes have brought together a strong force for market warming and improved livelihoods。

The temperature of the tax policy is no less, no more, no more. The start-up value added tax (vat) is linked to the new deal, with no complex provisions, no stringent conditions, and the simplest criteria and the most direct way to leave the dividends to the groups most in need. It tells every grass-roots operator that the state sees your efforts, that the policy supports your insistence, that you operate with security and that you develop with security。

The year 2026 was the first year in which vat rule of law was implemented and the critical year in which the efficiency gains from micro-business were reduced. The policy of entry points is clear and is only part of a series of pro-business policies. As more accompanying measures are put on the ground, the micro-business environment will be more relaxed, the entrepreneurial employment climate will be stronger and the livelihood security will be strengthened。

Whether it be a small shop or a part-time job, every effort deserves to be respected and every income protected. The new vat new deal uses the most straightforward rules, the most stable expectations, the protection of grass-roots businesses, the promise of small businesses, the security of flexible employment and the occasion for ordinary people's lives。

Have you ever enjoyed this tax exemption in any small store or self-employed person around you? What more do you want to know about the vat new deal? Exchanges and sharing in the comment area are welcome。

This document is based on the bulletin of the ministry of finance, the general tax administration and official interpretations of 31 january 2026, and is based on the most recent national policy and the requirements of local tax authorities; it is a personal point of view and does not constitute a professional financial advice。