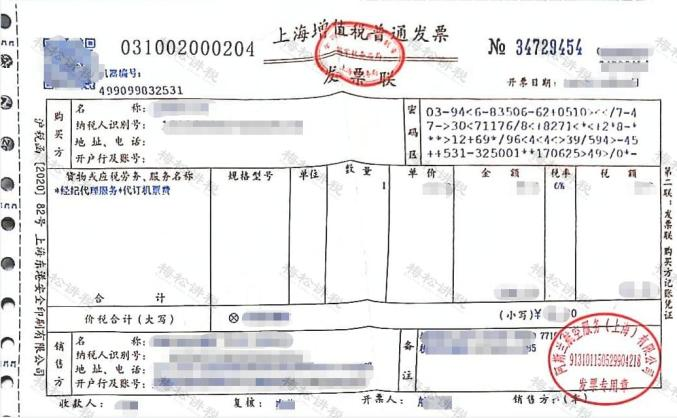

When qiu had recently processed his travel claims for operational staff, he turned around and couldn't find a flight ticket

He looks at this invoice, and he's got a lot on his mind. Carefully, there are at least two problems with this invoice:

(1) the name of the service is “brokering agency services”

(2) it is a paper invoice, not an electronic invoice。

Only electronic invoices for “domestic passenger transport services” are required to offset taxes! So, obviously, this invoice can't be deducted

What are the tax-related aspects of travel vouchers that require attention when travel costs are more or less the business involved? Today, the editor will make the best accounting, deductions, deductions, and suggest collection studies

01

What's travel

There is no clear definition of travel in the current accounting standards and tax laws. We now refer primarily to the relevant provisions。

02

How travel costs are accounted for

Depending on the purpose for which they are incurred, travel costs are charged to different cost categories:

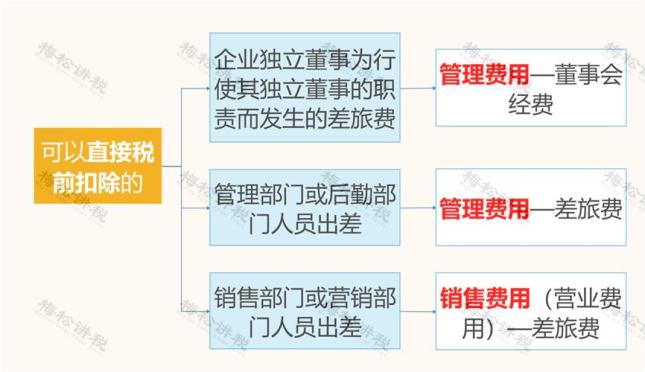

1. Costs incurred by management or logistics personnel on mission, including

Administrative costs - travel

2. Travel expenses incurred by sales personnel for the sale of products, including

Sales costs - travel

3. Travel expenses incurred by sales staff to promote and promote products, taking into account

Sales costs — operating advocacy costs

4. Business's travel expenses for clients, taken into account

Sales costs - business hospitality

5. Travel expenses incurred by directors or exclusives of an enterprise in the performance of their duties, taking into account

Administrative costs - board of trustees costs

6. Reimbursement of travel expenses incurred by enterprises to invite experts for training purposes

Administrative/sales costs - employee education

7. Travel costs incurred by manufacturing enterprises for commissioning production and assigning production technicians to the trustee site for technical guidance and on-site quality control, taking into account

Cost of manufacture - travel

Attention

Accounting should not be accompanied by only one invoice, but also by supporting documentation of the authenticity of travel expenses, including, but not limited to, the name, time and place of travel. Purpose of travel, payment vouchers, etc。

03

Vat processing for travel

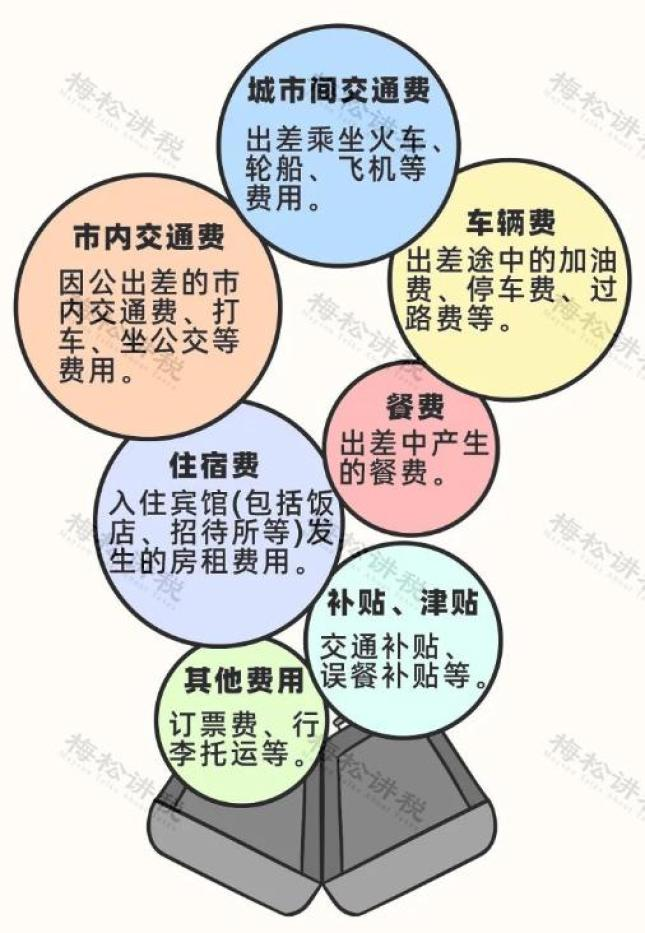

Travel costs relate to value added tax (vat) revenue credits and mainly cover the three main categories of transportation, vehicle and accommodation. (invoices for catering costs are in no way offset against taxes)

I. Transport

At present, electronic tickets have also been introduced in some areas:

The taxes are shown directly in the tickets, and when the train fare is reimbursed later, there is no need to calculate the value-added tax deduction, so just tick the credit

Ii. Vehicle costs

(1) own vehicles: expenses incurred in the course of a mission, such as refuelling, maintenance, etc., may be offset by pre-tax and non-premise tickets if they are invoiced exclusively for vat。

(2) public use of private vehicles: specific invoices for fuel costs incurred while on mission may be certified as credit. However, the company must enter into a rental agreement and must expressly agree that the company will bear the costs of oil, parking, etc., otherwise there will be no credit。

(3) car rental costs: vat-specific invoices obtained as required may be offset。

Iii. Accommodation

Accommodation costs incurred while on mission are allowed only if they are sufficient to obtain a specific invoice for vat up to the company. However, crediting is not permitted in the following cases:

(1) in the case of collective benefits, such as reimbursement of expenses incurred by employees for travel, family visits, etc.

(2) be of personal consumption, such as shareholders or employees of the company

(3) accommodation costs incurred by the preparers of the enterprise's tax-exempt or simple tax collection projects on mission。

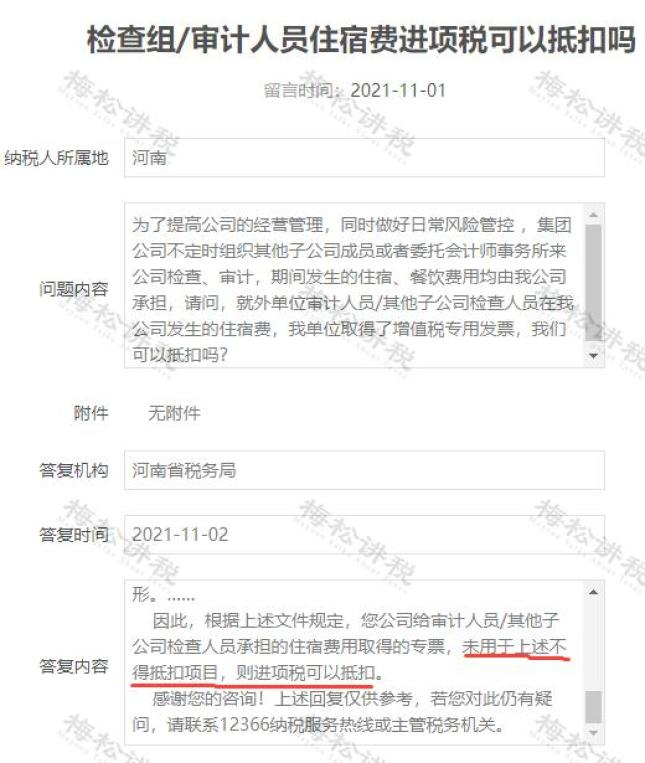

As we mentioned earlier, the reimbursement of airline tickets, train tickets, etc. By an enterprise to outsiders cannot be offset by taxes, so what about accommodation costs for outsiders

According to the directorate-general's reply, the receipt of a specific invoice for vat is deductible to the extent that the cost of the accommodation incurred by the enterprise is related to the production operation and is not used for non-deductible items such as collective benefits, tax exemption, etc。

Annex: value added tax deduction process

I. Those instruments (spot, equip)

Access to local [the integrated services platform for value added tax invoices] allows for normal selection. For electronic general and other electronic tickets, a selection of the corresponding type in the [invoice type] is required to be checked。

Ii. Calculated deductions (airfares, train tickets, etc.)

Air tickets, train tickets, etc., obtained require crediting to the tax to be entered in [e-tax office], and the calculated tax is to be filled in under “8b” and “10” in [vat tax returns (table 2)。

04

Tax-related treatment of enterprise income taxes on travel

Business income tax treatment for travel costs is simpler than vat. According to article 8 of the income tax act for enterprises:

Reasonable expenses, including costs, costs, taxes, losses and other expenses actually incurred by the enterprise in connection with the acquisition of income, are allowed to be deducted in the calculation of the taxable income。

In other words, travel costs may be deducted before taxes as long as they are related to the enterprise's production operations and are reasonable. But the point that needs to be noted here is that not all of them can be deducted in full, and we need to divide them according to the purpose of travel。

I. Amounts deductible before direct taxation

Ii. Amounts deducted prior to tax limit

Iii. Required to access the assessment of assets

05

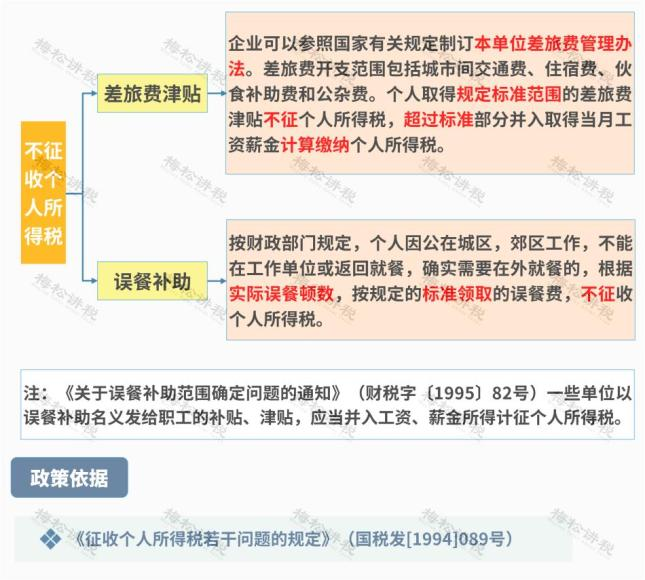

Personal income tax treatment for travel

For a tax, the first thought was travel allowance, food subsidy, and many people were vague about it. In this regard, under the current tax legislation, two explicit individual income taxes are not levied:

But we'll always see this:

An individual's income tax is levied on the basis of the payment of transport, meal allowance and, in cash, personal income tax, but the personal income tax may not be levied as personal income if the unit is reimbursed on the basis of the actual cost of transportation and food invoice incurred by the official, in accordance with certain national standards。

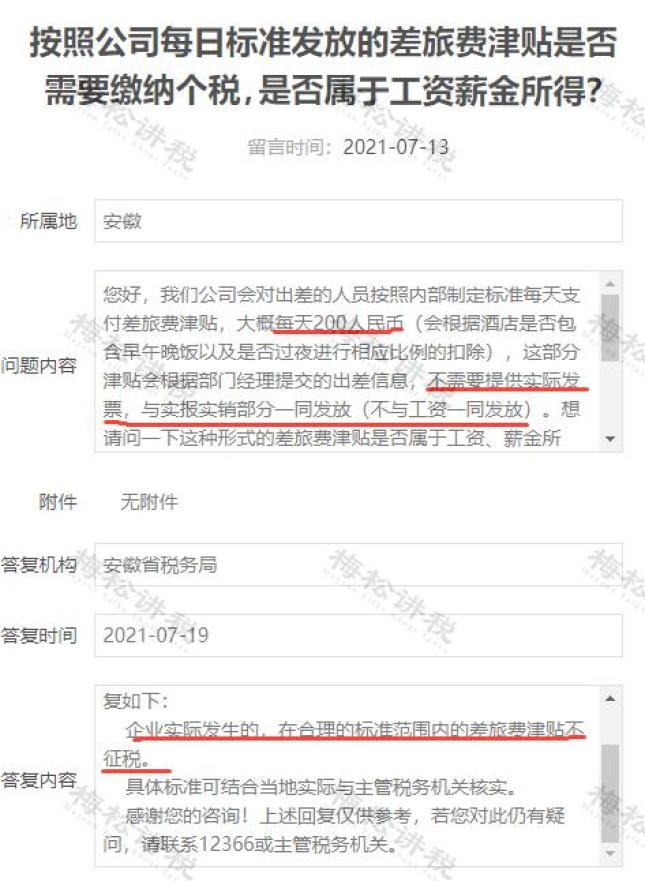

There is no specific description of the “cash mode” of distribution here, while on the 12366 platform of the directorate-general a similar answer was found to be close to here:

In answer, no personal income tax is required as long as it meets local standards. In the case of local standards, which are generally directed at public officials, in the case of enterprises, no personal income tax is required as long as it meets the standards of the enterprise's internal system. (of course, specific criteria would still need to be approved with the local tax authorities