Accounting integrity library

Page1/numpages1

Accounts performed -- accounting entries for cash payments for travel claims

1. Operational definitions

Travel claims are for expenses incurred by staff on official business trips (e. G., commercial negotiations, project research) such as transportation, accommodation, food support, etc., which are reimbursed on a compliance note to the unit for cash payments (non-transfer/service card) operations, with the core being “instance compliance, within-standard reimbursement”, distinguishing between “reimbursement before loan” and “direct advance after reimbursement”。

2. Core scenario and processing process (business and government accounting, cash payments)

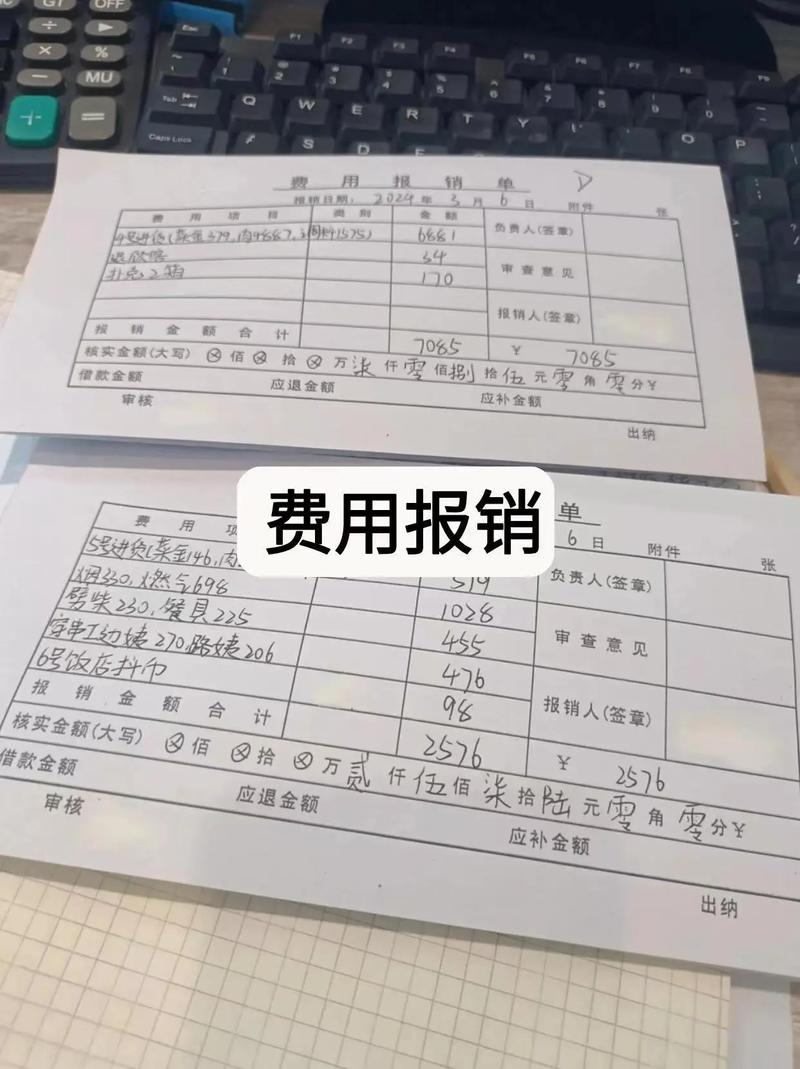

Scenario 1: company accounting (staff king on a business trip, pre-loaning $3,000 in cash, reimbursing $2,800 after a mission and returning $200 in cash)

Steps

Time of operation

Accounting entries

Remarks

On advance travel

Borrowing: other receivables - wang's loan: cash on hand

Advances are subject to approval by the enterprise's travel management system with the borrowing order

Upon return from mission, reimbursement of travel expenses (details: $1,500 for accommodation, $800 for transportation and $500 for catering, totalling $2,800)

Lending: management costs — travel costs — 2,800 (sale duty charged to “sale costs”) cash in hand of 200 (repatriation of surplus) loans: other receivables — wang 3,000

If the catering allowance is “no ticket subsidy”, it is subject to the deductions provided for in the tax code and a tax is paid for the excess

If the amount reimbursed exceeds the amount advanced (us$ 200 in cash if us$ 3,200 is reimbursed)

Loan: administrative costs - travel costs: 3,200

Refunds of cash are subject to the travel claims bill, indicating the amount of the replenishment and the reasons for it

Scenario 2: enterprise accounting (staff directly advance travel, cash received when reimbursed, amount