Fixed assets are the key resources that underpin the practice of vocational education, scientific research and teaching activities. They are mainly assets whose duration of use exceeds one year (excluding one year), whose unit value exceeds the prescribed standard [1,000 yuan (inclusive), of which the unit value of specialized equipment is 1,500 yuan (inclusive) or more], and which, in the course of their use, essentially maintain their original material form. While the unit value does not meet the required standard, a large number of items of the same kind with a durable duration of more than one year (excluding one year) are similarly treated as fixed asset management. Government accounting standards are implemented in public vocational schools and are administered in accordance with the asset management system of administrative units. The fixed asset classification consists mainly of seven categories: houses and structures, equipment, antiquities and displays, books and archives, furniture and appliances, special flora and fauna, and materials。

I. Status of disposal of y college assets

The disposal of fixed assets is essential for the upgrading of asset equipment and the smooth operation of schools. In accordance with the regulations on the management of state assets in the administrative profession, the management of the assets of vocational colleges and colleges is competent to dispose of their own state assets in accordance with the law。

1. Conditions and manner of disposal of y college assets。

If one of the following conditions is satisfied: assets that are technically obsolete or unmaintainable or have no maintenance value; assets that involve losses, bad debts and abnormally lost; assets that have exceeded their useful life and cannot meet existing work needs; assets that have been damaged or lost as a result of force majeure, such as natural disasters; and the separation, consolidation, modification, revocation, change of affiliation or partial functional or operational adjustment of the respective state assets, they shall be subject to transfer and transfer procedures in accordance with the relevant national regulations。

2. Asset disposal process at y college。

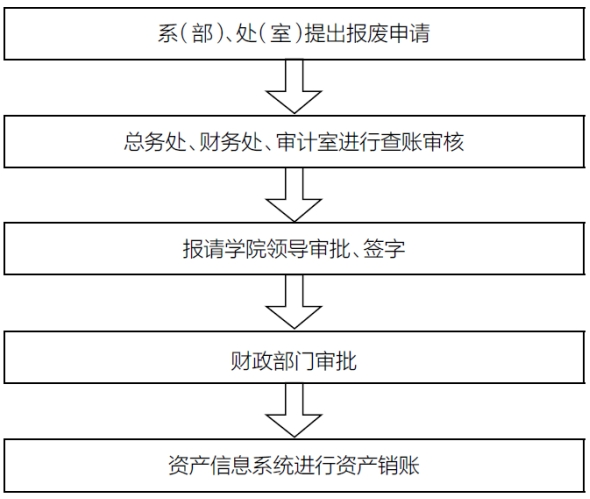

Figure 1 y college fixed assets end-of-life flow chart

The general services division is the functional asset management unit of the college and is responsible for the operation, management and supervision of the institute's state assets (figure 1). In the case of assets that have met the end-of-life criteria, after technical validation by the user department, the general services division, in conjunction with the treasury and the audit office, carries out an audit of the accounts, which is followed by a management study and approval by the college, which is followed by an asset information system for disposal. The full proceeds from the disposal of assets are paid to the treasury。

Ii. Disposition of y college assets and problems

The management of fixed asset disposal needs to be further strengthened in recent years as vocational colleges and colleges have grown significantly, with continuing innovations in management concepts and management models and the expansion of fixed assets. However, in practice, the management of fixed assets continues to be heavily procured and managed, as does the disposal of fixed assets。

1. Disposition of assets。

In 2020-2024, y college conducted 11 fixed asset disposals, as shown in table 1, four in 2020, all in november, with a total value of $4619,000; in 2021, four in april and july, with a total value of $121. 4 million; in 2022, no fixed asset disposal was carried out; in 2023, one in 2023, with a total value of $1,89. 19 million; and in october and december 2024, two fixed asset disposals with a total value of $298. 3 million。

Table 1y college: fixed asset disposals 2020-2024

(unit: items)

As can be seen from table 1, there were more fixed asset disposals in 2020 and 2023, most fixed assets in 2020 were used student tables, chairs, etc., and most fixed assets in 2023 were teaching, hands-on equipment, etc., which is related to teaching, scientific upgrading and frequent equipment upgrades。

2. Problems and analysis。

(1) low awareness of fixed asset management and weak implementation of the system. On the one hand, fixed assets are usually managed by asset-use departments, most teaching staff are not professionals and management knowledge and management capacity are relatively inadequate. At the same time, there are fewer asset managers who are unable to detect, declare and process ageing and damaged teaching equipment in a timely manner. In addition, there is a financial and physical overload in asset-using departments. Generic assets, such as desks and chairs, are not managed after they have been used, with flexible transfers between departments, but their movements are not adjusted in a timely manner in the asset system, which makes it difficult to determine the attribution of assets when they are disposed of. On the other hand, since the time of disposal of fixed assets at the college is irregular, it is always in practice

Surplus, resulting in the long-term accumulation of idle assets or unserviceable equipment in warehouses。

(2) the delay in the development of information. The y college is still in its traditional static management model for fixed asset management, and the existing fixed asset management system supports single-person single-man operation, does not allow real-time dynamic management and makes it difficult to meet current information-based management requirements. In addition, the asset management system and the financial system operated independently and did not allow for data interconnection, and during the fixed asset disposal process, the reconciliation of asset accounts with the treasury relied only on manual data entry, resulting in inefficiencies。

(3) defining the end-of-life of the asset is difficult. Compared to the general administrative service, most of the fixed assets of vocational colleges are used mainly for teaching and practical training. As a result, the utilization and depreciation rates of these assets in the course of their operations depend heavily on their quality and frequency of use. Moreover, the y college students, aged 15 to 18 years, are less aware of the management and maintenance of fixed assets, and some equipment is idle or out of use before reaching the end of its useful life, affecting the quality of teaching and squeezing the college's asset quota, which has long been detrimental to the healthy development of vocational colleges。

(4) poor communication of information. When fixed assets are assigned to each user department, responsibility for maintenance and management rests with each user department, while accounting for and integration of fixed assets is the responsibility of the general services branch. Assets that have reached the end of their useful life but are of continuing value are redeployed to the general services. However, due to the relative independence of asset management and asset-use units, the relative independence of asset users and asset managers, the timely declaration and redeployment of fixed assets that have continued to have a useful life has resulted in some fixed assets being idle. This may lead to a disconnect between asset management and accounting, and the actual condition of fixed assets is not consistent with the bookkeeping。

Iii. Resolution of the disposal of assets

1. Strengthen asset information systems to achieve information-sharing。

The management of fixed assets at vocational colleges should actively explore information technologies such as artificial intelligence, big data, etc

Internet+” governance model to enhance real-time management and information-sharing between asset management and user departments to achieve an effective combination of asset dynamic and static management. Clarify the responsibility for the management of fixed assets, implement them and improve the precision, standardization and sharing of information resources。

2. Increased awareness of asset management and strengthened management。

Increased awareness of asset management, rejection of the concept of procurement and less management, strengthening of internal controls, improved oversight of the entire asset management process, and proposed improvements to improve the utilization of fixed assets. In particular, fixed asset disposal management needs to focus on prior work, including receiving and inspection, warehousing, use and maintenance, to ensure normative and accurate asset management. In addition, it is necessary to strengthen the asset management workforce, establish a sound management structure, optimize staffing levels, sensitize more teaching staff to the asset situation, enable asset management to allocate and dispose of fixed assets in a timely manner and ensure that fixed asset management is efficient。

3. Regulate the fixed assets disposal process and simplify the approval process。

Professional colleges and universities should continuously improve the process of disposal of fixed assets and specify the timing of disposal of fixed assets. Untimely disposal leads to the accumulation of scrap fixed assets, creates safety risks and is detrimental to campus management and resource utilization. At the same time, given the multiplicity of fixed assets and, in particular, the generation of solid-trained waste in the course of teaching, disposal patterns also need to be disaggregated, and subject to strict compliance with the asset end-of-life disposal system, appropriate delegation of authority should be delegated to the user department, with a view to further strengthening the coordinated management function of the asset management department in order to increase the efficiency of asset disposal。

Concluding remarks

In the face of delays in information-building in the disposal of fixed assets, difficulties in defining end-of-life years and poor communication of information, higher-level institutions must actively use the “internet+management” model to improve access to fixed asset management, increase awareness of asset management and further develop asset-sharing, thus contributing positively to the development of vocational education。