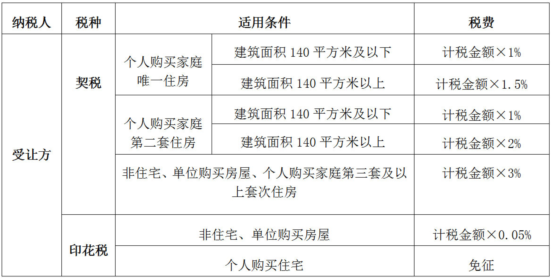

I. Calculation of taxes and fees related to the purchase of first-hand (incremental) homes

[note] in line with the provisions of the circular of the general tax administration of the ministry of finance on further support to small microenterprises and individual businessmen in the development of tax and fees policies (official gazette no. 12 of 2023 of the general tax administration department of the ministry of finance), the stamp duty on vat small taxpayers, small microbusinesses and individual business owners is halved。

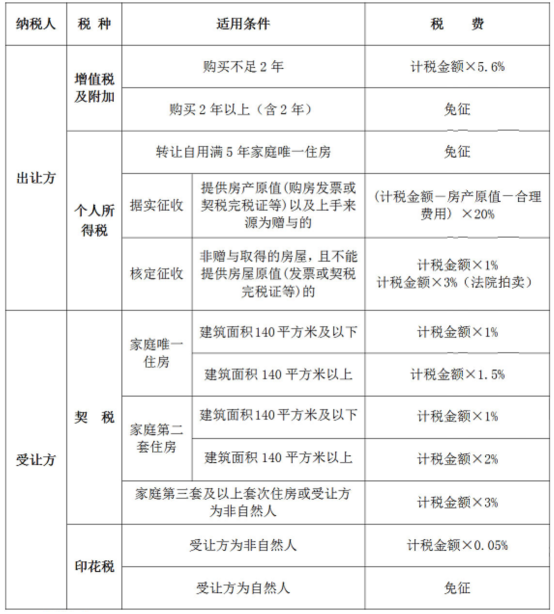

Ii. Calculation of taxes and fees related to second-hand (stock) house transfers

(i) table of calculation of taxes and charges relating to the transfer of residence by individuals

[note]

1. Urban maintenance and construction taxes, stamp duties, education surcharges and local education supplements are levied on small-scale vat taxpayers, small-scale micro-enterprises and self-employed businesses in line with the provisions of the proclamation of the general tax administration department of the ministry of finance on further support to small microenterprises and individual businessors in the development of tax and fees policies (official gazette no. 12 of 2023)。

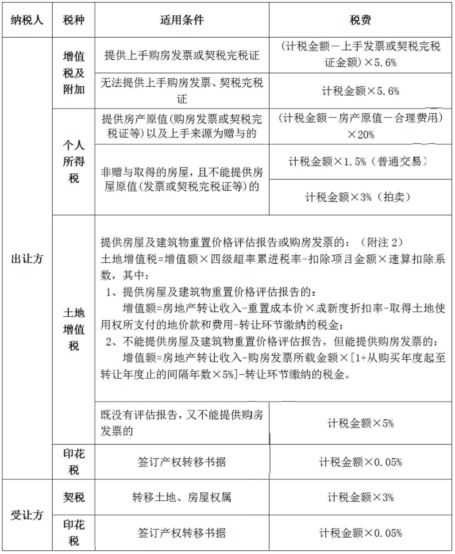

(ii) calculation of non-residential-related taxes on individual transfers

[note]

1. Urban maintenance and construction taxes, stamp duties, education surcharges and local education supplements are levied on small-scale vat taxpayers, small-scale micro-enterprises and self-employed businesses in line with the provisions of the proclamation of the general tax administration department of the ministry of finance on further support to small microenterprises and individual businessors in the development of tax and fees policies (official gazette no. 12 of 2023)。

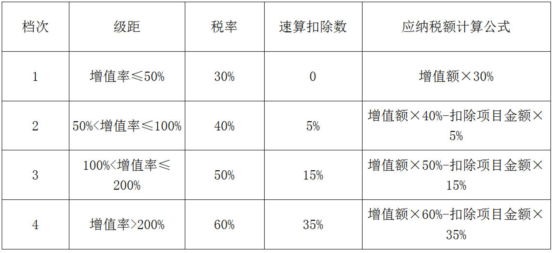

2. The value added of land value added tax (vat) = income from real estate transfers — less project amounts, value added = value added/item amounts x 100 per cent, is determined on the basis of value added rates, which are as follows:

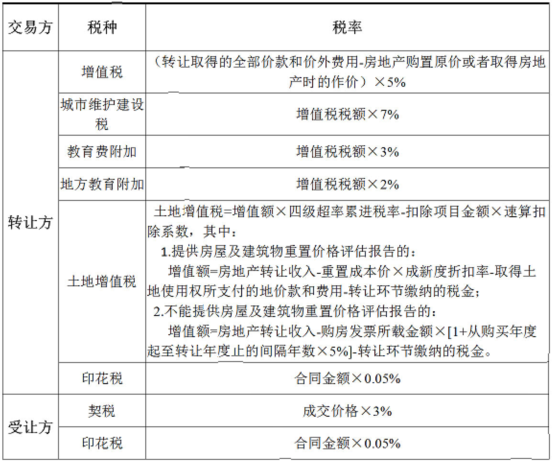

Schedule of rates for transfer (trade) of second-hand houses between enterprises

[note]

1. The above-mentioned taxes and fees are payable only for the real estate transaction (of which vat is the calculated rate of advance payments), and the transferor of the real estate is required to obtain income from the transfer of the real estate and to declare the payment of the relevant taxes and fees on time in accordance with the relevant policy provisions。

2. Urban maintenance taxes, stamp taxes, education surcharges and local education supplements are levied on small-scale vat taxpayers, small-scale micro-enterprises and self-employed entrepreneurs, in line with the provisions of the circular of the general tax administration department of the ministry of finance on further support to small microenterprises and individual businessors in the development of tax and fees policies (official gazette no. 12 of 2023)。

3. The value added of land value added tax (vat) = income from real estate transfers – less project amounts, value added = value added/item amounts x 100 per cent, is determined on the basis of value added rates, which are as follows: