The market for dry-dumped shipping has weakened for almost a year and appears to be in “spring” in the near future。

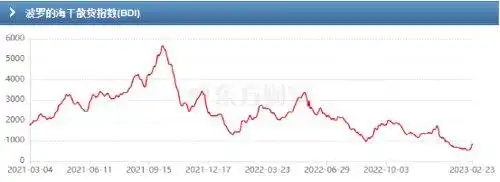

As at 23 february, the baltic dry bulk cargo price index had risen over five consecutive trading days, 23 of which surged by 21 per cent, the second highest increase in its history. For five consecutive days, the total increase in this index has reached 53. 96 per cent。

Since last year, the dry-dry shipping market has been weak, with the baltic dry-dry freight index falling by over 30 per cent. The “five strikes” index has also led to an increase in shipping units in recent days, with a 24-day increase of over 12 per cent in port-based pacific shipping and a peak increase of close to 7 per cent in chinese-owned vessels。

The index rose five days in a row

According to journalists, the baltic dry bulk cargo price index recorded the second highest increase in the history of the baltic sea on 23 december, due to the increased demand for ships of all types. The index rose by 142 points to 21 per cent, the highest since mid-june 2020. It is known that the baltic dry bulk cargo price index has risen from 530 points on 16 february to 816 points on 23 february, with a sudden increase of 53. 96 per cent in five days。

The baltic dry bulk price index, which reflects the change in the current freight rates of the world's main shipping routes, includes three types of shipping prices: capesize (the cape of good hope), panamax (panama), and supramax (the peri-perfect)。

Among them, the caper ship weighs 170,000 to 180,000 tons, mainly for long-distance transport of industrial materials such as iron ore and coal; the panamanian ship weighs 60,000 to 80,000 tons, mainly for human goods such as coal, grain and sugar; and the super-periphery ship weighs 50,000 to 60,000 tons, mainly for grains, fertilizers and cement。

Since the second half of 2022, the dry-dumped shipping market has continued to run down prices owing to the adverse effects of weak demand for iron ore in china, the risk of a recession in europe and the united states, and the russian-ukrainian conflict, which led to restrictions on coal and food exports in the black sea region. Throughout 2022, the average values of the baltic dry diffusion price index, the hyperplytic shipping price index and the pyramid ship fare index declined by 34. 3 per cent, 16. 9 per cent and 16. 7 per cent respectively。

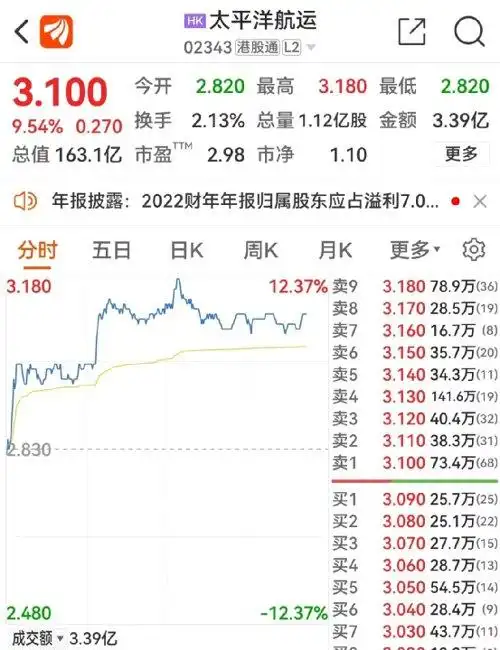

The persistent rebound of the index has also led to a marked variation in the second market share prices of the listed companies concerned. On 24 december, the port stock of pacific shipping increased by over 12 per cent, with china-pacific energy and hydrocarbons international driving the increase. On the a stock side, chinese ships and merchant ships also increased by up to 7 per cent and 5 per cent。

What's going on

In the dry bulk freight industry, china is the largest buyer of the global bulk transport market, with bulk imports accounting for 46 per cent of the global seaborne bulk volume (2021, clarkson data). Among the three main types of iron ore in dry bulk, coal and food, china contributed 76 per cent of global iron ore-calibre turnover requirements, as well as 13 per cent of coal requirements, and india contributed 24 per cent of global coal requirements。

As a result, the trade demand for dry bulk goods in china has a more direct impact on the market for dry bulk carriers. In industry, recovery demand rebounded in the wake of the 2023 epidemic in china and is expected to boost global demand for dry diffusion。

The chinese-taiwan securities point out that since late 2022, inflation in europe and the united states has gone up, economic growth has slowed and the chinese epidemic has been strained in four quarters, and the high prices of dry-dispersed shipments have been severely depressed, while the return to production in 2023, following the chinese epidemic, will lead to a rebound in import demand for iron ore, coal, food, etc。

In addition, shin gin mangang calls “the bottom of dry bulk goods is late but not absent”. According to the agency, unlike the rebound of the previous year's index at the bottom of the scale from the beginning of the fifth month to the fifteenth of the first month of the agricultural calendar, this year it was at the bottom of the twenty-sixth month of the agricultural calendar, which was related to the overall resumption of work, and the subsequent baltic dry freight price index had the potential to increase by two consecutive digits。

According to clarksons projections, global seaborne bulk is expected to increase by 1. 3 per cent, or 1. 9 per cent, in 2023 and 2024. Of these, iron ore, coal, food and small bulk volumes are expected to increase by 0. 1 per cent, 2. 1 per cent, 5. 0 per cent and 0. 6 per cent in 2023. The agency expects that shipping prices will rebound in the first quarter of 2023, and that prices will rise quarterly in 2023。

It is important to note that the first quarter is a less season of traditional maritime transport, but at this time there is a “lower season” in the dry transport market. As previously indicated by merchant ships, the three main sub-sectors of shipping appear to be less pronounced in recent years and should be characterized by changes in the pattern of the shipping industry。

Next, south american cereal exports will begin a boom season in march, which is expected to boost the market for small and medium-sized vessels. Moreover, the expected further landing of the accelerated domestic infrastructure programme will help boost demand for commodities such as iron ore and coal, thereby boosting the price index and restoring the maritime market in the second quarter。

The supply side of the dry bulk ship is tense

On the supply side, the capacity of dry bulk carriers is affected by the ageing of the fleet, insufficient capacity for new construction and environmental constraints。

A study of zhexiang securities indicates that, owing to the serious ageing of the dry bulk fleet, future supply growth is expected to decline further. As of december 2022, the share of hand orders in the current fleet was 7 per cent, while the share of the industry-wide dry-dumping fleet was 12 per cent over 20 years of age, higher than the share of additional capacity. The economy of old ships is poor, while new environmental regulations will accelerate the dismantling of old ships。

In the case of merchant ships, it was also mentioned last year that in 2022 bulk fleet deliveries declined by nearly 30 per cent in terms of weight tons, totalling 194 vessels, totalling 15,622 million heavy tons (28 capes of good hope and 58 panamanian). Also, in the first half of the past year, 17 dismantled cargo vessels were affected by the weakness of the large bulk ship market, which was mainly of good hope. Clarkes projected an increase of 1. 8 per cent, or 0. 3 per cent, in global dry bulk supply in 2023 and 2024, with demand increasing by 2. 0 per cent or 2. 2 per cent, with supply increasing at a slower rate than demand。

Its current shipyard capacity is strained and future new supplies are limited in the face of the crowding of containers, lng ships, automobiles, etc. Chinese ships have also recently indicated that company orders are full and are scheduled until 2026。

It is also believed that, from the perspective of the whole of 2023, the possibility of a full transition in the dry bulk market would be highly relevant to the pace of economic recovery in china. If the tempo is restored to an ideal level, the supply side of the fleet, which grew slowly in 2023 and 2024, is expected to enter the horizon and lead to a recovery in dry and bulk freight prices。