This paper combes the core foundation of options, pricing models, risk measurement tools (greek letters) and practical trading applications. The rationale and parameters of the black-scholes pricing formula were elaborated and the definition, nature and significance of the delta, gamma, vega, theta, rho five greek alphabet were analysed in depth, and the pricing analysis, risk monitoring and strategy-building of the right deal provided the theoretical basis。

Definition and type of options

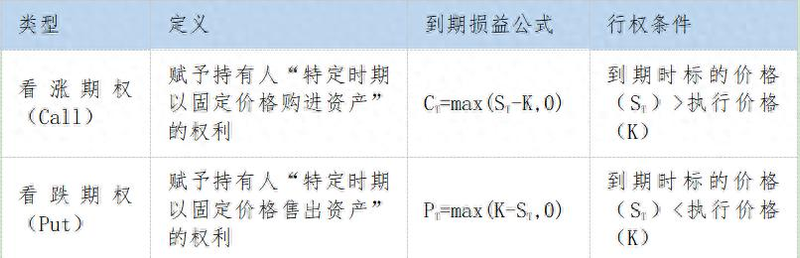

An option is the holder's right to buy and sell assets at fixed prices at certain times (european: maturity date; american: at any time before maturity). The difference is as follows:

Ii. Parity formula

For the same object, the current price of the item and the present value of the right, there is an accurate, non-arbitrable pricing relationship between the same item, the current price of the asset and the present value of the right, the european option of t at the same maturity date (and the asset in question is not paid for dividends during the life of the right), its subscription options (call) price,c the purchase options (put) price,p the price of the asset and the present value of the right to trade: c+ke-rt=p+s

The following is to be pushed down through arbitrage-free pricing and replication of assets:

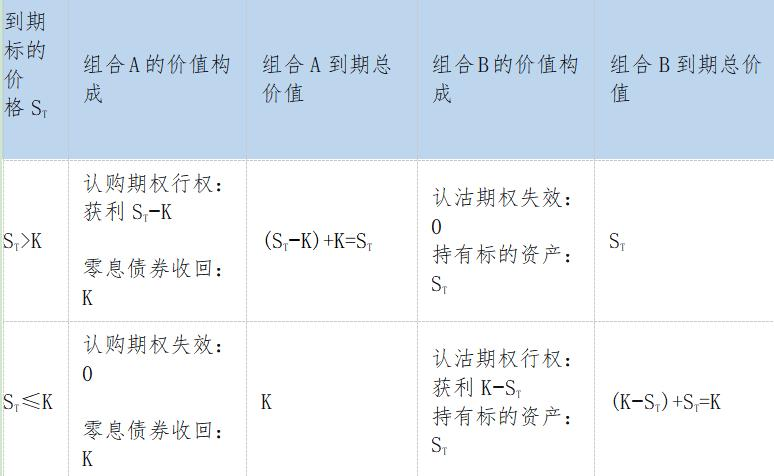

Construction of two portfolios:

Portfolio a: a european-style subscription option plus a zero-interest bond with k at t-time

Group b: a european-style buyout plus a unit-based asset s

The performance price of the right to subscribe, the right to sell, is k and the duration is t. The current value of portfolio a is ke-rt, the value of european-style subscriptionsc and zero-interest bonds; the current value of portfolio b is the value of european-style purchase optionsp and the asset s。

Conclusion: in all market situations, the value of combination a and group b at maturity date t is max (st, k). According to the principle of arbitrage, their current construction costs (i. E. Present value) must be equal: c+ ke-rt=p+s

It shows that the value of european-style subscriptions can be derived from the value of the same liner price and european-style subscriptions on maturity dates; conversely, the value of european subscriptions can also be derived from the same liner prices and european subscriptions on maturity dates。

The black-scholes pricing formula

1. European-based options pricing formula:

C=s0n(d1)—ke-rtn(d2)

2. European-style options pricing formula:

P = ke-rtn (-d2)—s0n (-d1)

Where: n ('): standard normal cumulative distribution function; d1 and d2 are extrapolated intermediate variables associated with s, k, r, & & t

C. P: look up, look down, look down, say up

S0: current price of the targeted asset

K: right-of-hand prices

T: expiration

R: no risk interest rate

Consideration: annualized volatility of assets

3. Pricing rationale and value composition

Core logic: the black-scholes formula can understand the expectations of rights-based maturity gains and losses at a risk-neutral probability measure, namely, c=e-rte, p=e-rte。

Value composition:

Intrinsic value: right to immediate movement, rising to max (s-k, 0) and falling to max (k-s, 0)。

(b) time value: the higher the rate of volatility, the longer the maturity, the higher the time value of the option price, which is influenced by fluctuations and maturity。

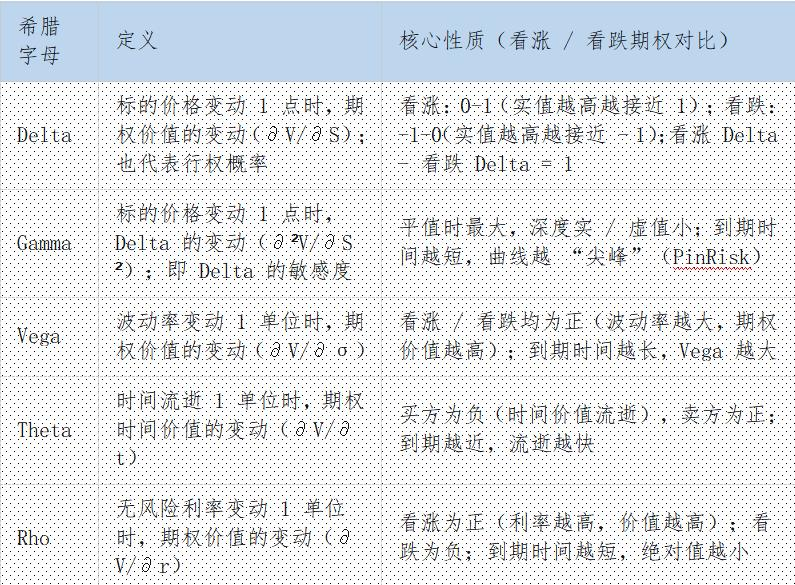

Greek alphabet: quantitative indicators of option risk

The greek alphabet is used to measure the effect of variations in the “target price, volatility, time, interest rate” on the value of options. The core indicators are as follows:

Xu yeon (investment advisory certificate z0020627)