“development costs” are an important consideration in the calculation of land value added tax by real estate development enterprises. The following is a detailed answer to the specific application of the “development costs” of real estate in land value added tax calculations:

Composition of development costs

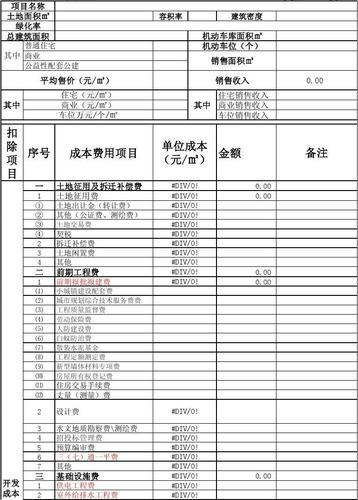

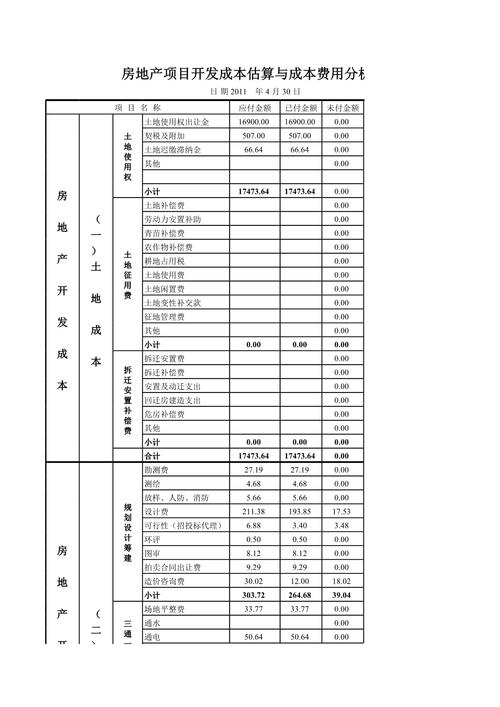

The cost of real estate development consists mainly of the following components:

Land cost: this includes the amount paid to acquire land tenure, such as land concessions, land transfer costs, etc。

Cost of construction materials: refers to the cost of construction materials, equipment, etc. Purchased in the course of real estate development。

Construction cost: includes payments made to the construction unit in the construction process and related administrative costs。

Other related costs: this may relate to design fees, supervision fees, ancillary facilities, etc. During real estate development。

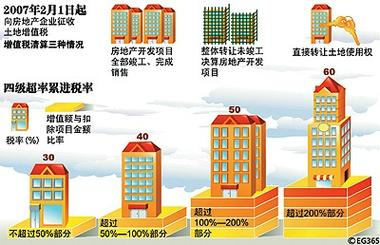

The role of development costs in land value added tax calculations

In calculating the land value added tax, development costs as one of the deductions directly affect the taxable amount of the land value added tax. In general, the land value added tax (vat) formula is: taxable = value added x tax rate - less project amount x speed deduction factor. Of these, value added represents the income from real estate transfers less the balance after deduction of the project amount, which includes development costs。

Iii. Attention to development costs

The principle of actual occurrence: the cost of development must be the actual cost incurred and cannot be a false or fabricated amount. This means that in calculating the land value added tax, an enterprise must provide real and accurate proof of costs。

Legitimacy review: development costs must meet the requirements of the relevant national tax legislation, otherwise they may be subject to tax risk. Therefore, when undertaking real estate development, an enterprise should ensure the legality of the costs incurred。

Iv. Legal basis

In calculating the land value added tax, development costs are determined and deducted in strict compliance with the relevant laws and regulations. For example, the law of the people's republic of china on land value added tax and its implementing regulations clarify the specific scope of development costs, criteria for deduction, etc。

In the light of the above, real estate development enterprises, when calculating land value added tax, should take full account of the development costs, ensure accurate accounting and declare tax payments in accordance with the law. At the same time, businesses should strengthen communication and cooperation with professional lawyers to ensure compliance with tax treatment and reduce potential risks。