2024. 11. 14

Medium-link futures: macro-momentation and suppression, and stinging

On 14 november 2024, the main futures contract contract fell by between 2. 98 per cent and 242,000, a three-day decline. This is mainly due to the recent trump deal and the apparent suppression of non-ferrous metals by the continued high inflation in the united states, offset by higher prices and weak basic margins。

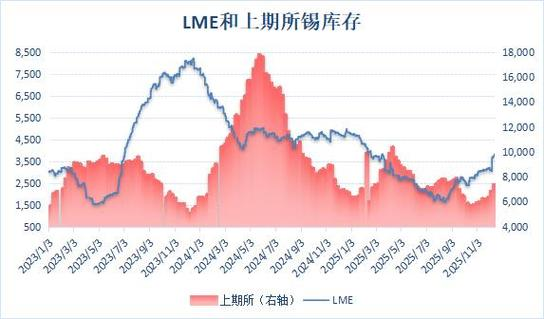

In terms of supply and demand, the demand for tin has been restored and re-opened. On the supply side, domestic tin production recovered in october; while the current wa ban on production is expected to resume in early 2025, with short-term supply problems remaining, the increase in stocks suggests that it has not yet had a significant impact. In terms of demand, the main downstream consumption areas are currently stable, with data on semiconductor sales, tin plating production and pvc production all warming up in the same year, but demand at the initial end of the chain, such as welding, is poor. The current tightness of the mine and the steady performance of the sun have not been accompanied by a significant shortfall, and wa's resumption of open-air work and the increase in imports have brought about immediate equilibrium and long-term excess expectations. At the macro level, the overall pressure on the ground after trump was elected president, while the 2. 6 per cent increase in the united states of america's cpi in october affected the market's decision to lower interest rates in december and weakened its mood。

Overall, today's fall in tin prices is largely macro-induced, with its modest base, but overvalued, leading to a fall in colour. After that, the moods are mostly volatile。

Risk factors: demand overexpected; supply disturbances; macro-emotional fluctuations

Guangzhou futures: short-term weakness by strong dollar-indexed shock

The current fundamentals of the tin market have not changed much, supply and demand tensions have not yet been further exacerbated, supply constraints in tin mines have continued to provide support, demand has not increased significantly, and the elasticity of prices has been released, with an increase of 237 to 10018 tons in tin society last week. The current limited drive, with more passive cassiterite price volatility following the overall colour, as evidenced by the continued decline in holding stock, the current funding heat is limited, the short-term operation of a strong dollar index to suppress shock is weak, not over-observed, and the main focus is on a 240,000 line。

Southwest futures: projected tin prices follow macromerses

Recently, myanmar has reiterated its strict policy of banning mines, the weakness of pre-regeneration concerns, the logic of returning to the mine's tight main line, the domestic aspect, the further weakening of the refining tin start-up rate, the continued decline in production, the continued warming of the electronics sector in terms of consumption, especially with better data on white household electricity discharges, although there is still some optimism about the trend towards the elimination of aggregate stocks, and the return of the absolute level of stocks to the previous year's average level, which is expected to follow macrometeorological trends。

Rhonda futures: watching for a while

At the macro level, the united states met market expectations in october with cpi and the federal reserve expected interest rate reductions to warm up in december; however, weak economic data in the euro area, as well as the trump tariff policy expectations, have kept the dollar strong. Essentially, the supply side, the tight processing costs of the tin mine, the tighter supply of raw materials from domestic tin refineries, increased smelting production pressure, and the decline in refined tin production is expected to continue until the end of the year; however, supply constraints are expected to improve in the near future due to the expected warming of wa production, as well as in indonesia's large exports of tin. On the demand side, the season is characterized by a marked lack of activity, a weakening of macro-magic sentiment and an increase in stocks. As a result, the expected improvement in supply and continued weak demand in the town of tin. Technically, the cystium discharge has fallen and the empty atmosphere has risen, breaking ma60. Operationally, for the time being。

Gin shrell futures: tin prices can still be viewed more widely after macroshocks have subsided

The recent strong dollar shocks have resulted in a general and sustained decline in metal prices. The main strength of tin was $242240 per ton, down 2. 98 per cent。

Essentially, although myanmar's previous submission stated that production had been severely cut off, the precipice of raw materials was still causing a significant reduction in smelting and lido's continued failure to deliver. In the post-market outlook, the balance is still expected to go to the treasury, and downstream purchases have improved in the near future owing to the low level of indonesian exports and the marginal improvement in consumption after the downside tin prices. As a result, tin prices are still viewed disproportionately after macroeconomic shocks have eased。

Light futures: price maintenance shock view

The supply-stretching logic had not materialized by the end of the year, attracting empty positions and more price support. In the short term, if this week's social bank continues to accumulate, it may put considerable pressure on prices. However, the tight reality of mines also continues to have an impact on production, with higher risks of emptying and price maintenance for shocks until actual improvements are seen。

(internally editor zhang yawan)