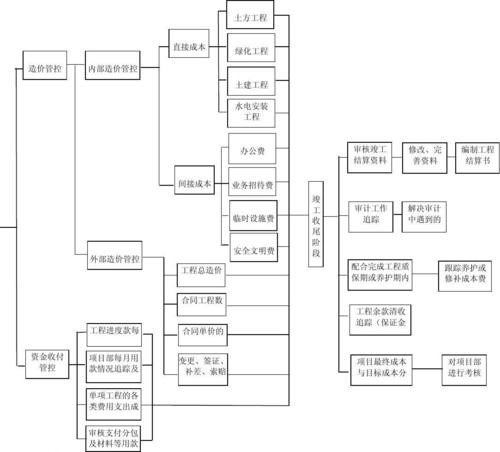

Project cost process management speaker: date: catalogue catalogue 01 cost-budgeted 02 implementation of 03 dynamic control mechanism 04 risk response 05 cost optimization path06 summary and improvement of 01 cost-budgeting percentage method to allocate costs to products or projects such as hours of work, material usage, machine use time, etc. Based on the drivers of cost occurrence. The cost-driven method of operating costs allocates costs according to the operation, and then distributes them to the product or project by calculating the cost of each operation. Total costs are allocated to various cost items in proportion, such as direct costs, indirect costs, administrative costs, etc. The list of works for the target cost decomposition method and the list of components of works based on the list consist of the name of the project, unit of measure, volume of work, unit price and total price, and constitute an important basis for cost budgeting. Based on the updating of the list, reasonable unit and total prices are determined on the basis of the characteristics of the project, contractual agreement, market circumstances, etc., which form the basis of the list. As the project progresses, it is necessary to update the billing and pricing basis in a timely manner to reflect the actual situation. The audit was prepared to collect relevant information and data to make a preliminary assessment of the reasonableness of the cost-budgeting exercise. The review process is conducted in accordance with the established procedures, and the cost budget is reviewed step by step to ensure accuracy and compliance. It provides a comprehensive review of all aspects of cost budgeting, including cost items, costing methods, cost allocation, etc. Based on the results of the audit, the cost budget was adjusted and refined to ensure that it was within reasonable limits. The budget review process standardized the cost plan for the implementation of the resource allocation and progress matching plan for resource requirements, based on the project progress plan, for each phase, including human resources, materials, equipment, etc. Optimization of resources is justified and optimized to ensure efficient use of resources, depending on their availability. The alignment of progress with resources ensures that resources are committed as planned and matched with project progress, avoiding waste or shortfalls. The cost of labour is reasonable in determining the unit price of labour and the number of workers to be used, improving labour productivity and reducing labour costs by strengthening labour management. Controlling the cost of materials for manual and mechanical materials strengthens the acquisition and management of materials, reduces the cost of materials and strictly controls material usage to avoid waste. Mechanical costs rationalize the use of mechanical equipment, increase its utilization and efficiency and reduce its cost. Phase cost accounting criteria determine cost accounting methods at various stages, such as flat cost methods, standard cost methods, etc., to reasonably reflect cost. Cost-accounting methods collect cost data for all phases of the project, including labour, materials, machinery, etc., in a timely manner to ensure the accuracy and completeness of the data. Cost data collection analyses and compares the costs at each stage, identifies the reasons for the cost deviation and takes appropriate measures to control the project cost within budget. The cost analysis and control 03 dynamic monitoring mechanism provide an in-depth analysis of the differences between actual costs and budgets, identifying the causes and factors influencing the cost deviation. Cost variance trend projections are based on actual cost data, predict future cost trends and inform project decision-making. Through tools such as project management software or spreadsheets, actual project costs are tracked and recorded in real time and compared with budgets. An early warning threshold for real costs versus budget analysis of deviations sets an early warning threshold based on project characteristics and historical data, and a reasonable cost deviation warning threshold for identifying and addressing potential cost risks in a timely manner. Early warning mechanisms trigger early warning responses when actual costs exceed established early warning thresholds, prompting the project team to take appropriate measures. Develop specific early warning response measures, such as budget adjustments, optimization of resource allocation, improvement of work processes, etc., to eliminate cost deviations. A rigorous change request, approval and implementation process is in place to ensure that all changes are fully validated and approved. The strict change process of the change of visa management elements provides a comprehensive assessment of the impact that the change may have on the cost, progress and quality of the project in order to make a sound decision. Change impact assessments strengthen the management and audit of visa changes to ensure authenticity and reasonableness of visas and avoid unnecessary cost increases. Visa management 04 risk-response market price volatility strategies have fixed price contracts with suppliers to ensure that price volatility is within control. The conclusion of fixed-price contracts adjusts the procurement strategy in a timely manner in response to project progress and market changes and reduces procurement costs. The procurement strategy is adjusted to set an alert line for price fluctuations and to take timely measures when prices reach or exceed the warning line. A price early warning mechanism has been established to establish unforeseen cost accounts in the project budget for emergency response. The establishment of an unpredictable cost account, based on the results of the risk assessment, set aside a percentage of unforeseen costs to address potential risks. Risk assessment and cost provisions establish rigorous approval procedures to ensure rational and transparent use of unforeseen costs. The risk-avoidance mechanism for the use of the unforeseeable costs set aside in the fee approval procedure, principle 010203, clarifies the rights, obligations and responsibilities of the parties in the contract and avoids disputes over the vague terms. Legal compliance reviews are conducted prior to the signing of contracts to ensure that contract terms comply with legal and regulatory requirements. The dispute settlement mechanism provides for dispute resolution mechanisms in contracts, such as consultation, conciliation, arbitration or litigation, in order to resolve disputes in a timely manner when they arise. Cost-benefit analysis of 05 technology options with different cost-optimization pathways assesses the output ratio of various technology options and selects the most cost-effective programme delivery. Technological innovation and cost reduction reduce production costs and increase productivity through technological innovation and process improvement. Standardization and scale production promotes standardization, scale production, lower procurement and production costs and improve product quality. Technical options optimize the procurement process, reduce procurement costs and increase procurement efficiency by comparing the selection and reduction of efficiency-enhancing vendor management and evaluation. Information sharing on the procurement cost control supply chain has been enhanced with the sharing of information with suppliers to achieve supply chain synergy and lower inventory costs. Establish supplier assessment systems, select quality suppliers and ensure quality and supply stability of raw materials. Wasteful mapping of supply chain synergetic optimization measures and waste mapping in the production process of the rehabilitation programme provides waste screening of various parts of the production process to identify sources and causes of waste. Wasteful corrective measures are wasteful of preventive mechanisms, which are based on the results of the screening process, such as the optimization of processes, the improvement of equipment utilization and the strengthening of management. Establish waste prevention mechanisms, enhance staff training, increase staff awareness of savings and prevent waste from recurring. The summary and refinement of the assessment methodology uses such methods as comparative analysis, trend analysis and results-based assessment of the cost budget, cost control and cost accounting. The cost-concentrating management results assessment assessment indicators include cost deviations, cost-effectiveness, cost savings, etc., to measure the actual impact of cost management. The findings form an assessment report, draw lessons and inform subsequent projects. Lessons learned database development includes lessons learned data on project cost estimates, cost control, cost risk etc. The contents of the database are collected through a variety of means, including actual project data, expert experience and relevant literature. Data collection methods are used to increase cost management levels in terms of decision-making support for project cost management, training education, etc。database application for existence in cost management