There is a new trend in the taxation of individual housing properties. Chongqing issued royal decree no. 367, which clearly introduced a new pilot policy on the taxation of individual housing properties from 1 january 2024. Let's see what happens

The pilot of an individual housing property tax has been taking place in only two cities since 2011: shanghai and chongqing, and other provinces and cities have not started. Thus, changes in the pilot policy represent, to some extent, a trend towards future property taxes. The new pilot policy has changed considerably compared to the previous individual housing property tax pilot, as summarized below:

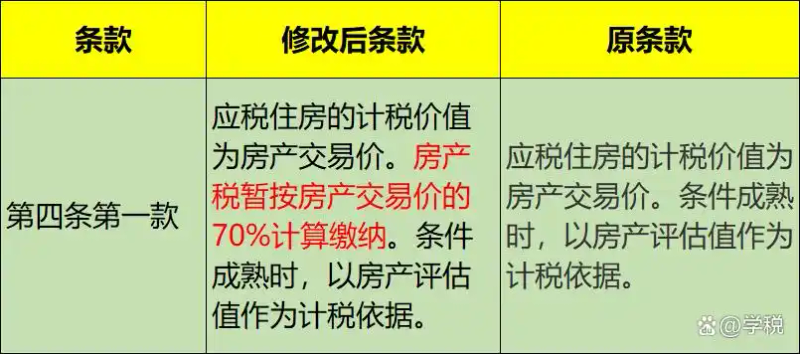

1. Lower tax basis

The tax basis for taxable housing is adjusted from the previous real estate transaction price to 30 per cent of the real estate transaction price. This is taxable = 70 per cent * tax rate for taxable building area* the unit price for trading construction area*。

Note: taxable building area means the area of construction of a taxable dwelling, after deduction of the taxed area。

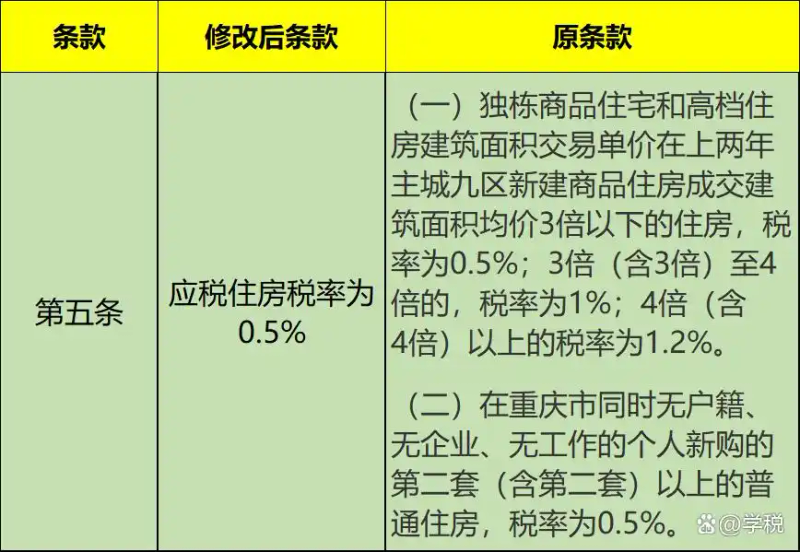

2. Reduction of tax rates

Previously, different tax rates were applied to single-commodity dwellings and high-end dwellings, as well as to the purchase of two or more units of general housing in specific cases: 1. 2 per cent, 1 per cent and 0. 5 per cent. The new policy is directly harmonized at 0. 5 per cent。

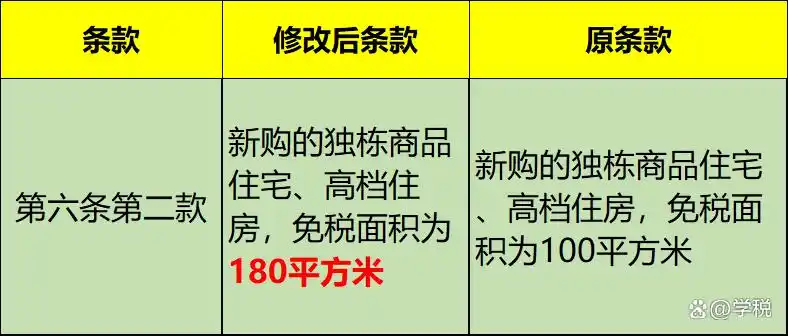

3. Significant increase in tax-free area

The former purchase of a single commercial dwelling, high-end housing, with a duty-free area of 100 square metres, has significantly increased the tax-free area to 180 flats。

4. Increase in the tax-deductible floor clause

The new policy added a bottom-up clause for other cases where the municipality considered tax relief or exemption to be necessary。

In general, the pilot policy adjustments focused on reducing the tax base, lowering tax rates and increasing tax-free areas, among other things. In the long run, this may mean that even if the property tax were subsequently introduced nationally, it would not be a burden for most people。

In the form of a thought map, i would like to summarize the content of chongqing's new housing tax for individuals:

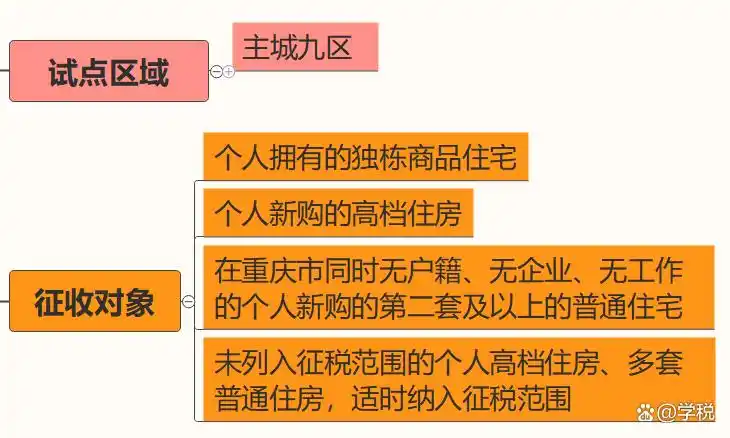

1. Pilot areas, tax users

The pilot was aimed at the nine main urban areas, namely: utsumi district, jiangbei district, saffang dam district, kowloon hills district, grand crossing area, south coast region, north china region, subei region, banan region, and also at the two new river areas, the chongqing new technologies industrial development area and the chongqing economic technology development area。

The pilot was implemented in a step-by-step manner, with the first collections mainly targeting single commodity houses, high-end housing, etc., and other follow-up, as appropriate, being gradually included in the tax coverage. Specifically:

Several conceptual interpretations:

(1) single-commodity housing: separate, single and unconnected housing complexes built according to law on state-owned land in real estate commodity development projects。

(2) high-grade housing: a unit price for the trade in building space up to two times the average value of a new commercial building in the 9th district of the main city in the last two years. Of these, the average price of the agreed building area is determined by the publication of the urban-rural construction sector。

(3) new housing purchases: including new houses and second-hand houses。

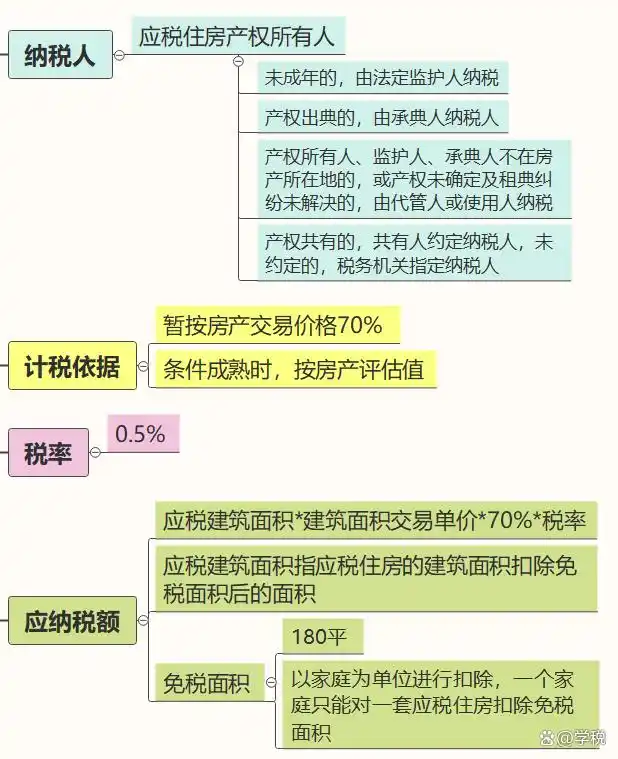

Taxpayers, basis of taxation, tax rate, calculation of taxable amounts

The taxable owner of the home is a taxpayer, temporarily paying the property tax at a flat rate of 0. 5 per cent, calculated at 70 per cent of the transaction price of the property. Specifically:

Note that:

(1) single-commodity dwellings and high-end dwellings, once included in the taxable domain, are subject to taxation in the absence of new provisions, regardless of whether or not property rights change, and the price of the tax transaction and the applicable tax rates are not changed。

(2) where the taxable housing is used for rental purposes, the new property tax is levied, and no property tax is levied on rental income。

(3) in the case of multiple taxable housing units, in general, the calculation of the first purchase is reduced by the amount of the tax exemption. Single-commodity dwellings owned prior to the implementation of the interim scheme, where taxpayers are free to choose which type to deduct tax-free space。

(4) taxable housing in the city of chongqing is not subject to tax exemption。

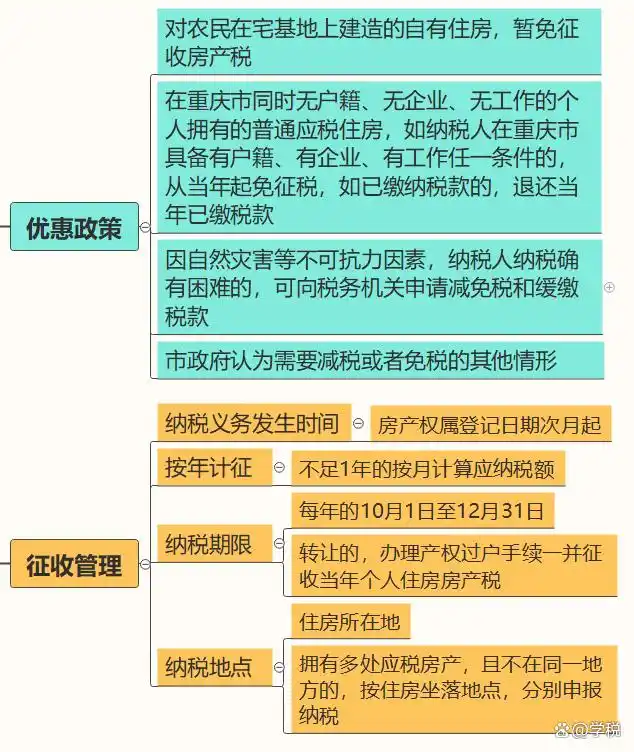

3. Preferential policies, collection management

The relevant tax relief benefits, as well as the time of occurrence of the tax obligation, the duration of the tax, the place of taxation, etc., are as follows:

In addition, the rules for the administration of individual housing taxes in chongqing city specify that:

Taxpayers who are unable to pay their taxes on time due to special difficulties may, at their request and with the approval of the tax authorities, defer payment of the current year's tax for up to three months。

In addition to the above, the administration issues and tax-related risks that taxpayers need to pay attention to include:

Under the information-sharing mechanism, departments such as urban-rural housing construction, planning natural resources, etc. Will share relevant housing information with tax authorities in real time. At the same time, the tax authorities will establish a “one-household” personal housing tax collection file。

Under the four-phase tax, the relevant departments will work together to establish a system of price comparisons for the stock of housing transactions, to assess the various types of individual housing stock and to use it as a reference for tax purposes. In cases where the transaction price of the housing stock is clearly low and unjustified, it will be taxed at the tax reference value。

3. The failure to pay the personal housing property tax will affect personal housing transactions, and the failure to complete the tax certificates and to carry out such formalities as household transfers, as well as personal correspondence。

4. Non-payment of the required tax on personal housing property and non-payment or underpayment of the tax constitute tax evasion, and taxpayers face a fine of 0. 5 to 5 times the non-payment or underpayment of the tax。

Finally, the above are for general reference only and not as a practical basis for action. High-quality author list