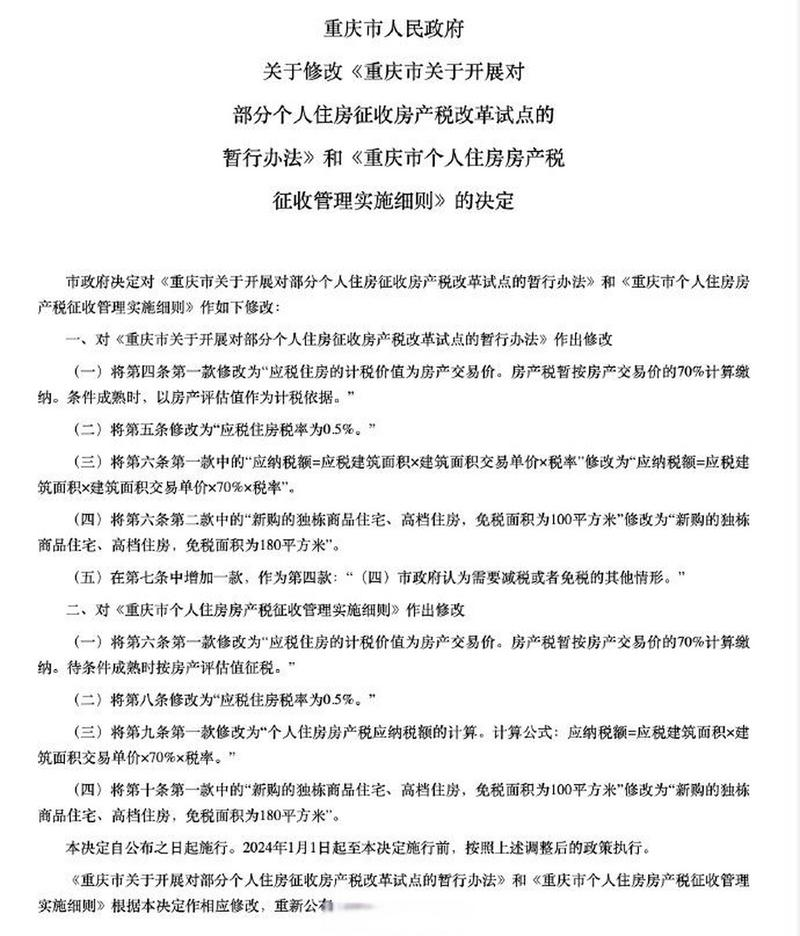

On 21 january 2024, the municipality of chongqing issued the decision of the people's government of chongqing city on the revision of the interim measures of the city of chongqing for the implementation of the reform of the real estate tax on selected individual housing and the regulations for the administration of the personal housing tax on chongqing city (order of the people's government of chongqing city no. 367, hereinafter referred to as the decision). In order to make the contents of the decision widely known in society, the policy is read as follows。

I. Background to the decision

In september 2023, in order to ensure that the party's central and state council decisions are deployed in order to better meet the demand for rigid and better sex housing and to promote the smooth and healthy development of the real estate market, our city adjusted the subject of the individual housing tax to “the first and more general housing units purchased simultaneously in chongqing city without a domicile, enterprise or jobless person” to “the second and more general housing units purchased simultaneously in chongqing city without a domicile, enterprise or jobless person”. The adjusted policy has been smooth and generally well-reacted. With a view to deepening the pilot reform of the individual housing tax, and taking into account the new situation in which the current supply-demand relationship in the real estate market has changed significantly, our city, based on the policy adjustments made in september, has made further changes to the interim measures for the implementation of the chongqing city pilot for the implementation of the property tax on selected individual housing and the rules for the administration of the chongqing city housing tax。

Ii. Main elements of the decision

As of 1 january 2024, one is to adjust the taxable basis for the taxable housing of our city's individual housing estates to 70 per cent of the value of the real estate transaction; two is to adjust the equivalent of 0. 5 per cent, 1 per cent, 1. 2 per cent and 0. 5 per cent of the equivalent of the three-storey rates for the commercial housing and high-storey housing carried out between the different trade price zones; three is to adjust the tax-free area for families that have acquired a single commodity dwelling since the pilot to 180 square metres; and four is to adjust the formula for calculating taxable amounts to 70 per cent of the taxable = the taxable building area plus the unit price of the construction area × 70 per cent of the taxable taxable area (of which: the taxable building area is the area of the taxpayer's taxable housing, after the tax-free area); and five is to increase the base clause “other case in which the municipality considers that tax relief or exemption is required”。

Examples of policy interfaces

Example 1: taxable single-commodity housing over 180 m2

The king of chongqing holds the first home of a family with a single taxable commodity, purchased in 2018 in the new regions of the two rivers. In that year, a real estate title certificate was issued covering 200 square metres of construction at a trade price of 3. 2 million yuan, at an original rate of 0. 5 per cent. Before and after the adjustment of the policy, wang was required to pay the personal property tax on the house as follows:

Tax payable in 2024 as a result of policy adjustments:

=(200-180) x (3200000 ÷ 200) x 70% x 0. 5% = $1120

Prior to the policy adjustment, tax payable in 2023:

= (200-100) x (3200000 ÷ 200) x 0. 5% = 8,000 yuan

Example 2: taxable single-commodity housing with a construction area not exceeding 180 m2

Zhongqing citizen zhang holds the first home with a single taxable commodity, purchased in 2017 in the kowloon poe district. In that year, a real estate title certificate was issued covering 170 square metres of construction at a trade price of $3. 23 million, at an original rate of 0. 5 per cent. Before and after the policy changes, a personal property tax on the house was payable as follows:

Tax payable in 2024 after policy adjustment = 0 yuan

Prior to the policy adjustment, tax payable in 2023:

= (170-100) x (3. 23 million x 170) x 0. 5 per cent = 6650 yuan

Example 3: high taxable housing with an area exceeding 180 m2

Zhongqing citizen li holds the first taxable home of a family purchased in 2017 in the northern district of sumatra. In that year, a real estate title certificate was issued, covering 190 square metres and a trade price of $2. 85 million, at an original rate of 0. 5 per cent. Before and after the policy changes, li should pay the personal property tax on the house as follows:

Tax payable in 2024 as a result of policy adjustments:

= (190-180) x (285000 ÷190) x 70% x 0. 5% = 525 yuan

Prior to the policy adjustment, tax payable in 2023:

= (1900-100) x (285000 ÷190) x 0. 5% = 6750 yuan

Example 4: high taxable housing with a building area not exceeding 180 m2

Chongqing citizen liu xiao holds the first taxable home of a family purchased in the chu region in 2017. In that year, a real estate title card was issued for 160 square metres of construction at a trade price of 2. 4 million yuan, at an original rate of 0. 5 per cent. Before and after the policy changes, liu should pay the personal property tax on the house as follows:

Tax payable in 2024 after policy adjustment = 0 yuan

Prior to the policy adjustment, tax payable in 2023:

=(160-100) x (2. 4 million x 160) x 0. 5% = 4,500 yuan

Example 5: second and higher taxable dwellings

(resumed 4) citizen liu xing is also in possession of high-taxable housing purchased in the northern province in 2018. In that year, real estate titles were issued, with an area of 160 square metres and a trade price of 2. 56 million yuan, with an original tax rate of 0. 5 per cent. This is the second class of high-tax housing held by liu's family, which is deducted from the family's share of the taxable area, and a family can only deduct the taxable area from one set of dwellings. Before and after the policy changes, liu should pay the personal property tax on the house as follows:

Tax payable in 2024 as a result of policy adjustments:

=(160-0) x (2560,000 ÷160) x 70% x 0. 5% = $896

Prior to the policy adjustment, tax payable in 2023:

=(160-0) x (2560,000 ÷160) x 0. 5 per cent = 12,800 yuan

Example 6: in the city of chongqing, more than 2 new taxable general housing units have been purchased by individuals with no domicile, no business and no work

In chongqing city, zhao, who has no domicile, no business and no employment, holds a taxable general housing permit purchased in the south coast district in 2022. In that year, he issued a real estate permit with an area of 90 square metres and a trade price of 1. 08 million yuan; this is zhao's second common housing unit held in chongqing (as of october 2023, zhao's first common housing unit held in chongqing no longer pays a personal housing property tax). Before and after the policy changes, zhao was required to pay the personal housing tax for the second common housing unit as follows:

Tax payable in 2024 as a result of policy adjustments:

=(90-0) x (1. 8000 x 90) x 70% x 0. 5% = 3780 yuan

Prior to the policy adjustment, tax payable in 2023:

=(90-0) x (1. 8000 ÷90) x 0. 5% = $5,400