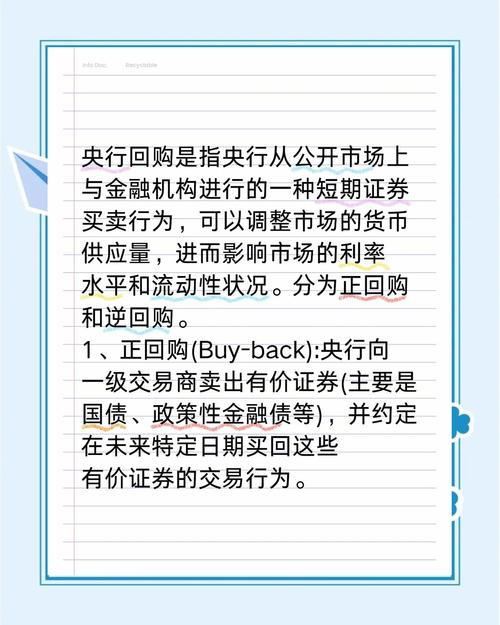

An ongoing buy-back is an agreement between the central bank and an institution to sell its own public debt in proportion to its nominal value, which is bought back after a specified period of time. The difference between purchases and purchases is the cost of using the funds during this period。

Repurchase and reverse

What is the impact of repurchases on the bond market? As ordinary shareholders, how can this information be used?

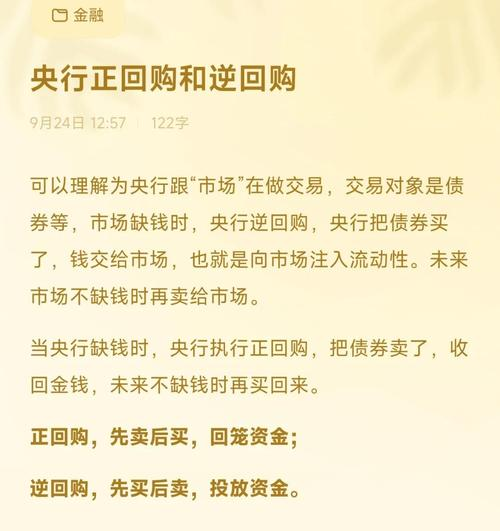

As a general definition, a bond buy-back transaction refers to a bond transaction in which both parties to a bond deal agree contractually to repurchase the bond by the “seller” of the bond from the “buyer” at an agreed price at a future date. One easier way to understand is to treat a bond buy-back transaction as a “bond pledge loan” in daily life, whereby a bond is mortgaged to a lender of money, obtain funds, and finally return the principal of the money to redeem the bond. From the point of view of the originator of the transaction, transactions in which the bonds are mortgaged and the funds borrowed are referred to as transactions in which the bonds are being repurchased; transactions in which the funds are loaned voluntarily are referred to as transactions in which the bonds are pledged in reverse. It is clear that the positive and reverse purchasers who are parties to the repurchase transaction are reciprocal and that the positive purchasers who have initiated the transaction must have the reverse buyer who accepted the transaction. Thus, we can simply say that the right buyer is the collateral that mortgages the bond and secures the equityr of the money, while the reverse buyer is the recipient of the bond pledge and the lender of the money。

In fact, in terms of the origin of the repurchase transaction, the repurchase transaction begins in close association with the operation of the central bank. In 1918, the federal reserve created a buy-back transaction to advance the development of bank bills of exchange, except for bank bills of exchange, not bonds, as collateral. So the bond buy-back deal, initiated by the central bank as the right buyer, is what we call the central bank's right buy-back operation. A bond buy-back transaction initiated by the central bank as a reverse purchaser is a reverse buy-back operation for the central bank. In accordance with international practice, central banks usually select from among market members those commercial banks, securities firms or trusts, i. E., those at the level of the open market, who are well-funded, well-reputable and trading, to act as counterparties to a positive and reverse buy-back through bidding. In general, in order for central banks to be successful in repurchase operations, they often offer a return interest rate that is slightly higher than the market return rate at the time of the volume bidding exercise, which makes it easier to enter into transactions and serves the purpose of smooth recovery. When central banks engage in counter-purchase transactions, they often give a return interest rate lower than the market return rate。

The central bank's open market is working on reverse buyback

The role and impact of the central bank’s open market and reverse buy-back operations are as follows:

Impact short-term market interest rates. Owing to the current high volume of repurchase transactions, the resulting repurchase rates have essentially become representative of short-term market interest rates and thus exist as a basic pricing measure for all types of investment. In carrying out positive buy-back operations, central banks will tend to lead to rising interest rates in short-term markets, which in turn may lead to rising interest rates in the medium to long-term. Often, higher market interest rates result in higher issuance rates in bond-level markets, where issuers tend to be willing to issue short-term bonds to lower the cost of debt; for secondary bond markets, the price of bonds, especially medium- and long-term bonds, may decline as interest rates rise, with the effect of opportunity costs or discount factors. Conversely, when central banks conduct reverse buy-back operations, as they usually have lower interest rates than market buy-back rates, they act as a disincentive to increase market buy-back rates, and may even lead to a downward trend in short-term interest rates, leading to a downward trend in medium- and long-term interest rates, leading to lower bond-level market issuance rates, where debtors tend to be more willing to issue long-term fixed-interest-rate debt; for secondary markets, bond prices, especially medium- and long-term bond prices, are rising as short-term interest rates contract。

2. Impact on the adequacy of market funds. When the central bank carries out an active buy-back operation, the central bank emerges as a lender of funds, thereby reducing the bank's excess reserves -- that is, the bank's free money is temporarily out of circulation. This would have a direct impact on the banks ' own ability to invest in bonds, while reducing their lending capacity to enterprises, thus tightening market finance as a whole and ultimately discouraging market demand for bonds. When central banks conduct reverse buy-back operations as financiers, especially in successive reverse buy-back operations, the result is to make markets rich. The impact of the adequacy of market funds on debt markets is self-evident, especially in the case of large-scale capital-driven debt markets or stock markets, and their impact is even more significant。

3. To influence the psychological expectations of investors. We know that in a situation where interest rates and funding levels are largely fixed or unchanged, the mental state of the market, investors or layoffs is almost entirely responsible for the rise and fall in the debt market. The role of the central bank in opening up markets and repurchases as powerful external information can naturally trigger speculation and judgement on interest rates and financial aspects, creating a complex market climate. In fact, when central banks are opening up their markets and repurchase operations are receiving more attention, the greater their influence on market psychological expectations。

The above discussion is a static analysis of the impact of active central banks’ positive and repurchase operations on debt markets. When central banks engage in ongoing or reverse buy-back transactions, the actual effect may be closer to the above analysis. But reality is often much more complex. First, because of the reversibility of buy-back transactions and their duration, which usually does not exceed one year, central bank buy-back operations are often used as a short-term daily tool, and when central bank buy-back operations are aimed at stabilizing short-term market interest rates, the central bank’s role and impact on interest rates and the financial landscape will be relatively neutral. Second, when other external conditions change, such as excessive foreign exchange, positive hedges by central banks, or reverse buybacks by central banks in response to market liquidity shortfalls, the effect will be different from the above analysis. Thirdly, the premature or irrational behaviour of market investors tends to inappropriately magnify or weaken central banks ' intentions to conduct positive and reverse buybacks, creating in many cases a situation that is contrary to theoretical analysis. Moreover, as a result of complex factors, exchange and inter-bank debt markets are still relatively fragmented, with central banks having different, reverse-purchase operations for the specific purposes and to varying degrees of impact for the two markets, as well as more time lags in policy roles, which may also lead to a number of distortions。

Since central banks are in the macro category of monetary policy, repurchase operations are of little operational significance for the specific guidance of a single bond or stock operation. However, ordinary investors should closely monitor the movement of central banks’ positive and reverse buy-back operations from the point of view of analysing the fundamentals of a debt or stock market, with due regard to the continuity of observation。