While the us-iraq war has been raging and the geopolitical situation continues, gold, a “traditional refuge”, appears to have been “disappeared” by the market, once into bear city。

According to robin brooks, senior fellow of the brookings institution, former chief economist of the international finance institute and former chief foreign exchange strategicist of goldman sachs, wednesday, the real driving force behind the price movement of precious metals since the beginning of the american-iraqi conflict has been the recent dramatic increase in bulk traders in metal markets。

In a recent article, he explains:

There are currently three theories in the market. First, the pre-war boom in prices of precious metals undoubtedly attracted a large number of bulk investors who had never traded precious metals such as gold. It is reasonable to assume that a broader group of investors may change the way precious metals are traded, making them more risk-like than risk-averse assets. This is in line with the fall in the price of gold at the time of the soaring oil prices and the rebound in the last day or two due to the expected slowdown in the market.”

The second general view is that, following the sharp rise in precious metal prices in late 2025 and early this year, many investors have already earned substantial returns on their precious metal positions. Increased uncertainty can end the profit, so people — reasonably speaking — may have locked in part of the gain。

The third interpretation was that increased market volatility in general led to losses in other positions, particularly in hedge funds. This situation means that people will receive additional security notices, and they will need liquidity to cope with it. This may result in them selling profit positions to release cash. Gold is one of them。

On the whole, however, brooks believes that none of these factors will undermine the risk-averse position of gold, nor will they negate the devaluation that had previously underpinned the price of gold. He wrote: “these factors do indicate that the buyer's group may have expanded, which is why we now see exceptional fluctuations in gold prices.”

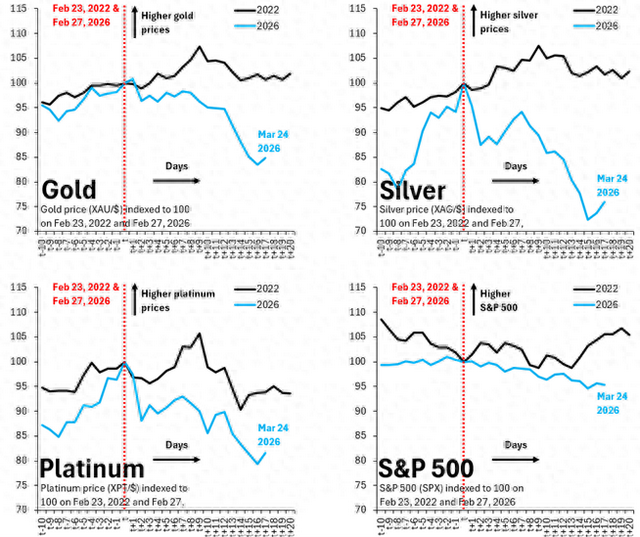

Brooks also shared four graphs showing the price trends of the gold, silver, platinum and platinum 50 indices since the beginning of the american-iraqi conflict, and the performance of these assets after the outbreak of the russian-ukrainian conflict in 2022。

“first, the prices of all precious metals have fallen since the outbreak of the war. Gold fell by 15 per cent, silver by 25 per cent and platinum by 20 per cent. In contrast, the standard 500 index fell by 5 per cent during the same period. Thus, the performance of precious metals is clearly less than that of large plates.”

“secondly, the 5 per cent drop in the standard 500 index is hardly an increase in risk avoidance, which means that the risk avoidance properties of gold have not been triggered.” brooks wrote: “this tends to suggest that the recent decline is a legacy of the sharp increase in prices and warehousing of precious metals。

Thirdly, the russian-ukrainian conflict did not really trigger a significant increase in the price of gold or other precious metals, while the standard 500 index - at similar time scales - is almost the same as it is today. This proves again that this could be a silo clean-up."

According to brooks, his personal explanation for the recent wave of sales was that the sharp increase in the price of precious metals prior to the outbreak of the iranian conflict had significantly broadened the investor base。

“for the time being, precious metals may be traded more like risky assets, which may explain why prices of precious metals have fallen as conflict escalates, while in recent days there has been a rebound with signs of detente. High volatility could also have a severe impact on some markets. It is not uncommon for a profit position to be forced to level off when there is a trade loss. Finally, as uncertainty increases, it is perfectly reasonable for people to lock in gains. When you are uncertain about the situation, you should stop the damage in time.” he added。

Finally, brooks concludes: “these explanations do not negate the devaluation transaction, which i am the proponent of. The need to seek safe havens beyond the monetization of debt will continue.”

I'll be right back