Core views

The cotton market has a short-term pattern of “realistic and expected bias”: a small fall in zheng’s main contract and a fall in hold, reflecting prudent pre-chongqing funding and low downstream purchases; but domestic production reduction expectations for the new year (7-10 per cent or less), weather disturbances in the global home country and high-maintenance low warehouse receipt structures support medium-term growth logic, with short-term inter-zone shocks projected, with a medium-term target price of $18,000 per ton。

A review of the situation

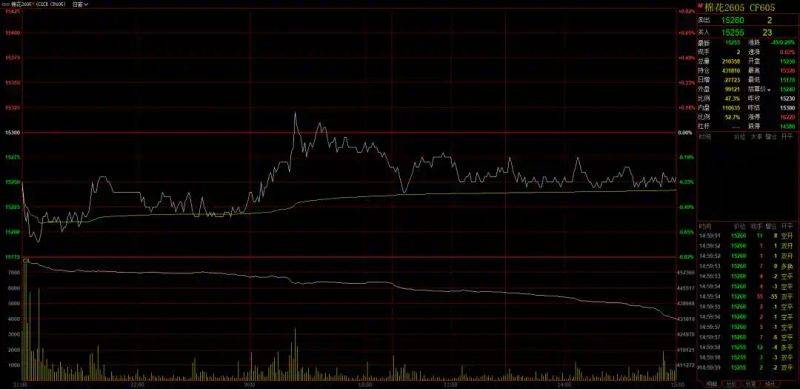

On 3 april, zheng kam main power contract cf 2605 reported $15255 per ton, a decrease of 0. 29 per cent over the previous trading day, with 200. 98 million hand in hand and 27. 7 million hand in hold. Small price reversals accompanied by a significant fall in holding tanks show a decrease in the power of multiple motion and a lack of clear directional driving in the market. At present, downstream spin-offs are dominated by demand-driven purchases, limited new orders, strong interest in the chain of industry and light delivery。

According to monitoring by the shanghai international cotton trading centre, the combined cost of cotton taken from xinjiang in the current year as at 3 april was $14,887/t (gross weight), the cost of cotton collected from xinjiang in the current year was $14,892/t/t/t; the average cost of warehouse billed from xinjiang in the current year was $14,922/t/t/t/t/d as at 3 april. On 3 april, the xinjiang kampuchea-kittiya sales base index (up to 2. 8 per cent for class 31-bis29) was $1379/t, an increase of $5 from the previous day. Of these, the northern territory had a base difference of $1421 per ton, the quilton and changi regions had a dominant base difference of $1365-1470 per ton; the southern territory had a base difference of $1327 per ton, the bay and aksu regions had a main base difference of $1345-1455 per ton and the kash region of $1125-1245 per ton。

Basic surface depth analysis

Supply side: supply-side pressures remain in place this year. As at 2 april, the national certification of cotton had reached a historic high of 7,615,300 tons, indicating an adequate supply of old cotton. At the same time, the state had issued an advance quota of 300,000 tons of smooth duty imports, adding over 600,000 tons of port stocks and sufficient short-term liquidity. However, the contraction in supply is expected to be strong in the new year: the area under cotton cultivation in xinjiang has been significantly reduced, with domestic production projected to decline by 7-10 per cent over the same period; and, at the global level, icac projects a decrease in global production of between 4 per cent and 24. 9 million tons in 2026/27, mainly due to a reduction in production in brazil, australia and the conversion of united states cotton farmers to competitive crops。

Demand side: "gold three" orders are warmed up, but silver four is a concern. The downstream swirl generally reflects the short and poor continuity of the order, the rapid but weak willingness of the finished stock to replenish the raw materials, and the maintenance of the on-demand purchasing strategy. On 3 april, the net cotton market was handed over to light, and some of the hinterlands began to take vacations because of losses, with a clear low-level veil. Despite the 10. 4 per cent increase in retail sales of clothing and the 17. 6 per cent increase in exports between january and february, indicating internal and external resilience, final consumption is still weak and demand pre-eminence inhibits purchasing incentives。

Cost and profit: a significant increase in cotton planting costs constitutes medium- and long-term support. The annual cotton planting cost in xinjiang has increased by $120 to $150 per acre, and farmers are expected to raise the purchase price of seed cotton to $8. 5 to $10 per kg, raising the cost hub of the next cotton price. Current profits from spin-offs have been reduced and the start-up rate has declined, further weakening current cotton consumption. On the external side, there has been a surge in the volume of american cotton export contracts (84 per cent increase in the weekly net-contracting ring compared with that of the united states), particularly for mainland china, with short-term demand improvements expected, partially offset by a stronger dollar。

Industrial chain linkages: brazilian cotton exports, which have reached a six-year high during the same period, have been reduced by price increases, and the middle east conflict has pushed up energy and maritime transport costs, resulting in more cut-off for textile enterprises in south-east asian importing countries (e. G. Pakistan, bangladesh), lower import willingness and a phase-out for international cotton markets. However, the current tight global availability of high-quality cotton resources (defunct australian cotton sales, brazilian fresh cotton on the market in september) has underpinned the recent increase in the base level。

Post-market outlook

Short-term (1-2 months): zheng cotton or the continuation of 14800-15,600 yuan/tonne inter-zone shock, the core contradiction lies in the easing of old supply and weak downstream demand to suppress prices, and the expectation of the replenishment and policy regulation (e. G., from national reserves) will limit the fall。

Medium (3-6 months): as the new year's decline logic is gradually realized, commercial stocks continue to digest and available resources tighten (currently only about 550,000 tonnes are forecasted, well below the 2. 25 million tonnes that have been precipitated in the main-force contract), demand and supply patterns are expected to shift towards tightening, driving up the price weight to 16,500 to 18,000 tonnes/t。

Long term (more than six months): if el niño triggers a further reduction in production in the world's home country, it adds to external and internal resilience support, and cotton prices exceed $18,000/ton。

Key risk points: 1 actual cotton area in xinjiang fell short of expectations; 2 large-scale cotton roll-out policies fell; 3 imports were blocked as a result of the escalation of trade friction between china and the united states; and 4 macro-liquidity tightening or geo-diverse conflicts subsided commodity financial attributes。