In order to follow up on the party's central and state council decision-making deployments and to promote the smooth and healthy development of the real estate market, the ministry of finance, the general tax administration department and the ministry of housing, urban and rural construction have recently issued a bulletin on tax policies to promote the smooth and healthy development of the real estate market, and the general tax administration department has issued a bulletin on lowering the floor of the land value added tax forecast, which has been in effect since 1 december 2024。

“the emergence of a series of policies reflects not only the refinement and flexibility of government regulation of the real estate market, but also the determination to regulate markets and stabilize expectations through tax policy.” lee xuhong, vice-president of the beijing national school of accounting, said。

What is the content of this new policy on taxation of housing transactions? What will be the impact on home buyers? Journalists are interviewed。

Increase tax incentives on the transaction of housing, and actively support the demand for affordable and improved housing

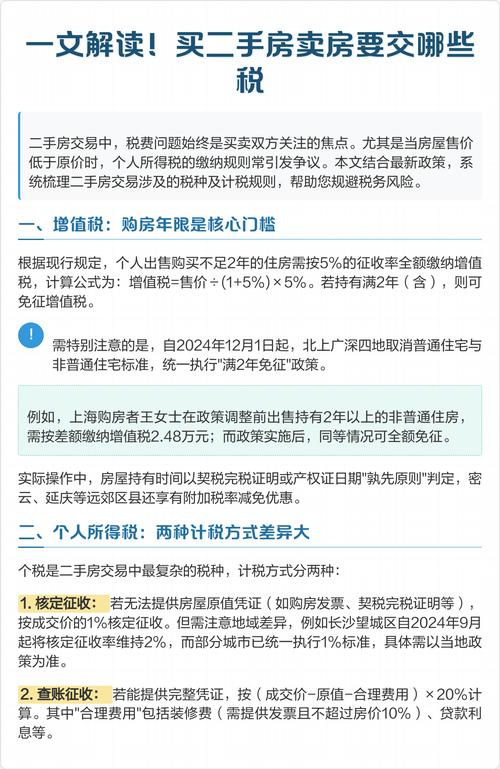

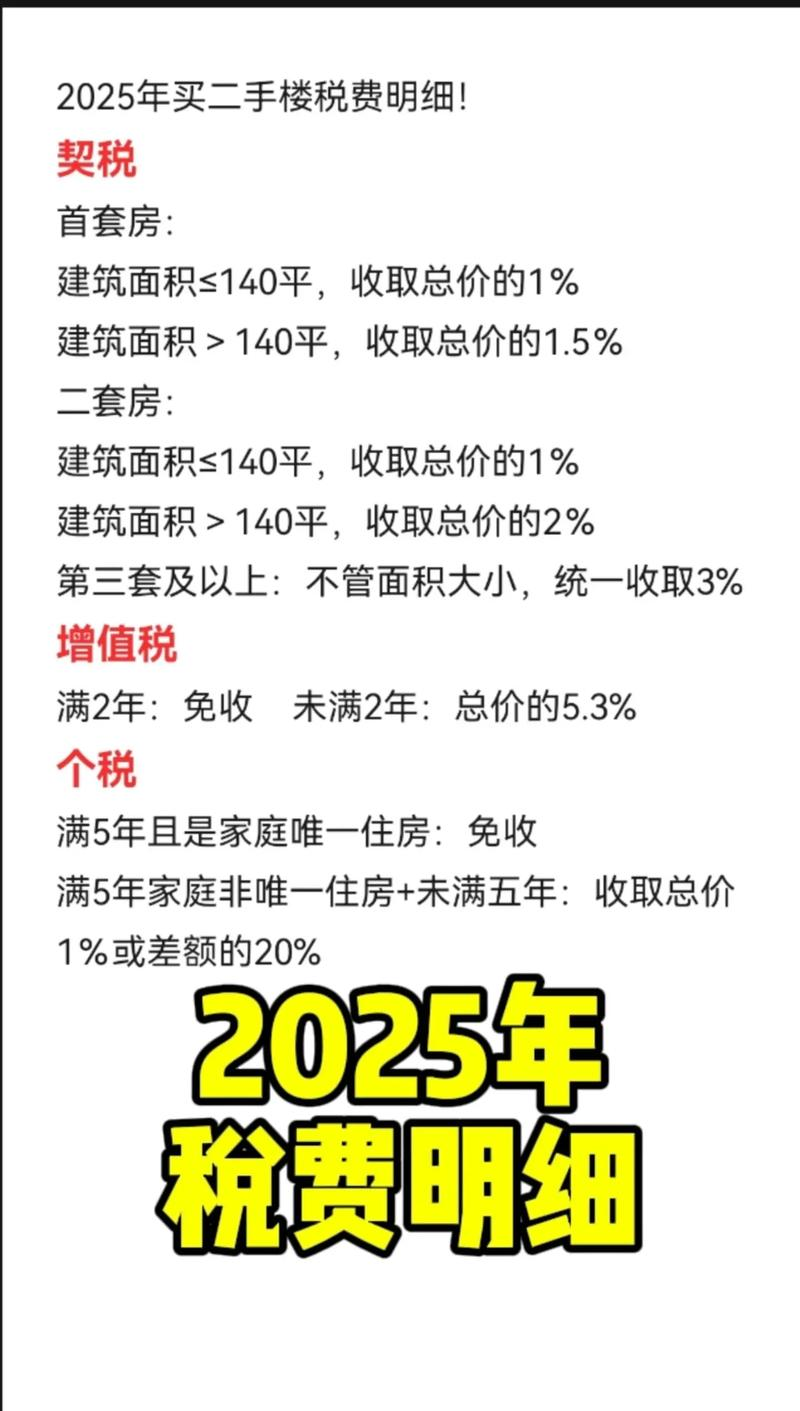

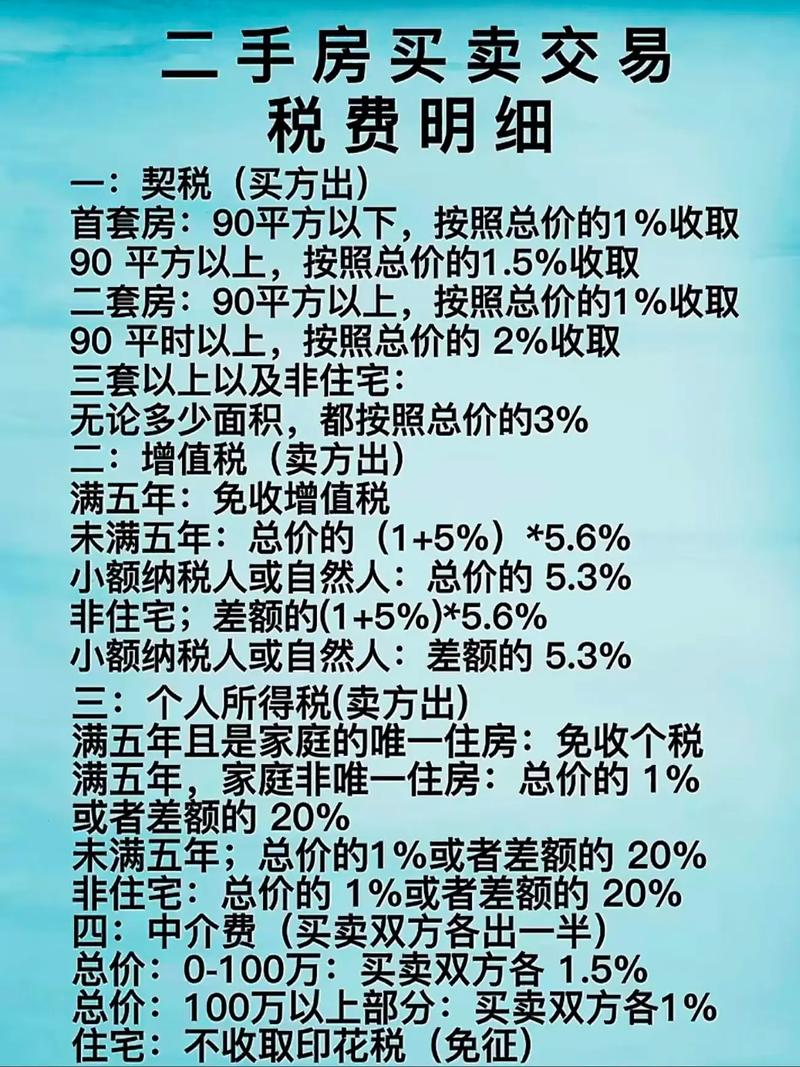

In accordance with the relevant bulletin, the new deal has increased tax incentives on the transaction of housing, and has actively supported the development of demand for affordable housing. To raise the current size rate of the 1 per cent low tax rate from 90 square metres to 140 square metres, and to clarify that four cities in beijing, shanghai, guangzhou and shenzhen could apply the second home tax credit policy in a uniform manner with the rest of the country, i. E., after the adjustment, pay the tax rate of 1 per cent for the purchase of a single home and a second home for a family, provided that the area does not exceed 140 square metres。

“the real estate chain, and in particular the second-hand housing transaction, is mainly related to deed and value-added tax (vat), which will increase the size rate of the 1 per cent low tax premium to 140 square metres, and will reduce the tax cost of the transaction by adjusting the tax rate of the beijing, shanghai, guangzhou, shenzhen 2 flats to 1 per cent and more than 2 per cent within 140 square metres. For example, the purchaser of a 100 square metre second flat in beijing, at a total cost of $5 million, compared to 3 per cent in the past, or $150,000, will receive 1 per cent, or $50,000, of the new policy。

It was explained that, if a taxpayer applied for tax benefits, he should submit to the competent tax authorities a family member information certificate and a written search of the taxpayer's home by the real estate administration in the place where the house was purchased. In order to increase the number of taxpayers benefiting from the policy dividend, tax dues are payable on individual housing purchases after 1 december 2024, as well as on the purchase of housing before 1 december 2024 but the declaration of tax due after 1 december 2024, which is subject to the new public notice。

Currently, our tax preference policy distinguishes between ordinary and non-ordinary dwellings, with corresponding standards in some places. The new deal clearly sets out the value-added tax (vat) and land value-added tax (vat) preferences that are linked to the elimination of ordinary and non-ordinary residential standards。

In particular, following the cancellation of the standard for ordinary and non-ordinary dwellings in the cities concerned, all purchases of personal housing for more than two years (including two years) are exempt from vat, and the provision for the imposition of vat on non-ordinary dwellings for more than two years (including two years) in four cities in beijing, shanghai, guangzhou and shenzhen has been suspended。

According to zhang, the policy is designed to encourage consumption and, in particular, to encourage improved replacements for those already living in housing. For example, a 160 square metre second-hand house in beijing, although it had been in possession for more than two years, was subject to differential value added tax because it was a non-ordinary dwelling. If, however, the distinction between ordinary and non-ordinary dwellings is eliminated, then the tax fee will be saved。

“these policies help to simplify the tax system, reduce the tax burden and compliance costs on enterprises and individuals, thereby stimulating market dynamism and promoting a balance between supply and demand in the real estate market.” lee xuhong said。

Lower floor of 0. 5 percentage points of advance tax on land value added tax to ease the financial difficulties of real estate enterprises

Land value added tax is required for land development by real estate enterprises. In order to guarantee the timely and balanced entry of land value-added tax (vat) revenues, the tax authorities, in accordance with the relevant provisions, levy a percentage of the advance land value-added tax (vat) on the income of taxpayers transferred to real estate before the completion of the project, pending the completion and settlement of the project。

In 2010, in order to better perform the role of pre-regulating land value-added tax (vat) tax, the directorate-general of taxes issued a circular on strengthening the administration of land value-added tax (vat), which established a lower rate of pre-collection, with the exception of secure housing, at 2 per cent in the eastern provinces, 1. 5 per cent in the central and north-eastern provinces and 1 per cent in the western provinces. At present, with changes in the real estate market situation, the level of value added for different real estate projects is structurally differentiated, and in some cases the rate of value added for real estate items has fallen significantly. It is necessary to adjust the lower limit of the forecast rate in order to provide space for the scientific adjustment of the rates and to promote the smooth and healthy development of the real estate market。

This time, the general tax administration announced a reduction of 0. 5 percentage points in the minimum pre-recruitment rate, which is 1. 5 per cent in the eastern provinces, 1 per cent in the central and north-eastern provinces and 0. 5 per cent in the western provinces, with the exception of secure housing. Moreover, local authorities may adjust the actual rates of advance collection to local realities, which need to be adjusted by establishing specific rates for each type of real estate on the basis of scientific estimates, in conjunction with local government guidance from the local tax authorities, taking into account, inter alia, the actual tax levels of local real estate projects。

Previously, there was a distinction between ordinary and non-ordinary dwellings in respect of land value-added tax benefits. The new deal explicitly abolished ordinary and non-ordinary housing standards in cities and continued to implement the land value-added tax (vat) waiver policy for the construction of general standard housing for taxpayers whose sales value does not exceed 20 per cent of the project amount。

In his view, the above-mentioned policy adjustments have helped to ease the financial pressure on real estate enterprises and support the promotion of the real estate sector。

Increased facilities for taxpayers to benefit from relevant preferential policies

The head of the relevant department of the general tax administration stated that, in order to ensure that taxpayers benefit from the tax incentives in a timely manner, the tax administration will take a series of measures with the relevant authorities to continuously optimize the tax service and increase the taxpayer's satisfaction and access。

Further enhance the effectiveness of window services. Local tax administrations will further optimize the offline window set-up and online operation, based on the “one-window” model of real estate tax processing, and provide a “one-stop shop” for the purchasers of their homes with taxes and certificates for “one-off”. In addition, tax authorities will provide tax services to those in need, depending on demand, through additional windows and extended tax processing times。

Further optimization of information delivery. :: continue to increase collaborative information-sharing in the sector, using shared information to prefill data and reduce the burden on taxpayers to provide and fill in information. In cases where information-sharing conditions are not available and the taxpayer is unable to submit the relevant documentation, the taxpayer may choose to apply the notification promise system in accordance with the current provisions。

Further strengthening of policy advocacy and interpretation. Local tax administrations, in conjunction with the relevant departments, will provide taxpayers with professional policy content interpretation and tax process counselling services through the tax service office's tax counsellors and the 12366 tax service hotline to respond quickly to taxpayers' concerns and ensure orderly tax administration. At the same time, multiple media have been used for policy advocacy and interpretation to create a good tax business environment。

Lee said that the “one-stop” tax service, the pre-filling of data using shared information, the ease of the tax process and the optimization of tax services would facilitate the timely access of taxpayers to the dividends of tax incentives。