With the advent of the era of “public entrepreneurship, mass innovation”, entrepreneurial activity has become more frequent and the related issues of equity trading have increased. The tax treatment of equity transfers is discussed below。

Elements of a tax treatment for the transfer of shares by natural persons

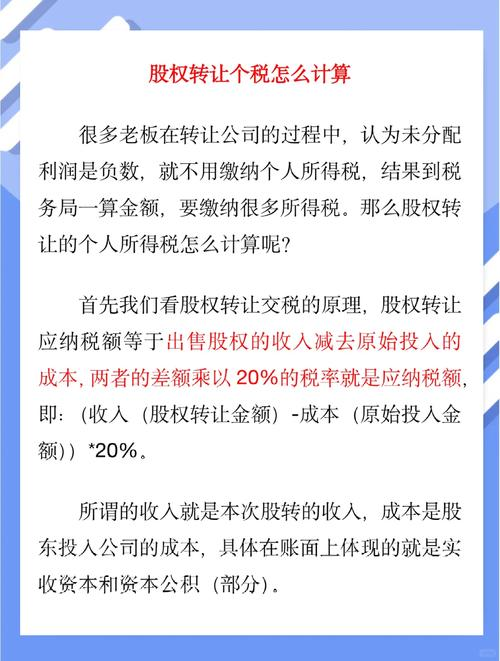

1 personal income tax calculation: taxable amount = 20 per cent (equity transfer income - actual contribution and related taxes)

Stamp duty = value of equity transfer agreement x 0. 05 per cent (print duty is a tax deductible before personal income tax)。

The definition of equity transfer income: according to the proclamation of the state tax administration on the collection of individual income taxes by individuals for the termination of investment operations (official gazette no. 41 of 2011), individuals who, for various reasons, terminate an investment, association, business cooperation, etc., acquire an equity transfer income from an invested enterprise or cooperative project, other investors from an invested enterprise, as well as from an operator of a cooperative project, default money, compensation, compensation and otherwise recovered, are income taxable to the individual, which is calculated in accordance with the provisions applicable to the “transfer of property” project。

Elements of tax treatment for the transfer of shares by legal persons

Enterprise income tax calculation: taxable income from an equity transfer = income from an equity transfer - actual contribution and related taxes and charges

2. Special equity transfers: when an enterprise withdraws, the equivalent of the accumulated undistributed profits and accumulated surplus of the invested enterprise as a proportion of the reduced capital received shall be recognized as dividends; the remainder shall be recognized as proceeds of the transfer of investment assets. Policy basis: state tax administration bulletin on selected issues of corporate income tax (state tax administration bulletin no. 34 of 2011)。

Elements of tax treatment for the transfer of shares by partnerships

1 personal income tax calculation: taxable amount = (equity transfer income - actual contribution and related taxes and charges) x overaccumulated tax-scaling deductions on production proceeds

2. Vulnerability to tax planning:

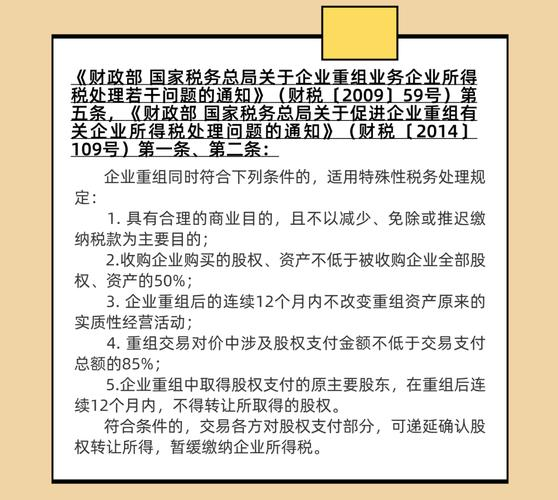

(1) non-fulfilment of the condition of document no. 101, entitled “incentives shall be based on the equity interest of the enterprise of the resident population in the country”, through the incentive of the holding platform, and hence the non-applicability of the deferred tax policy and the inability to complete the deferred tax filing (where documentation has been filed in the prior period, correction has begun where available)

(2) the transfer of shares of listed companies by an individual through a partnership, with a premium of value added tax (vat) of 6 per cent on the basis of a “transfer of financial goods” plus additional duties such as vat

(3) the dividends obtained by employees are not subject to the tax policy of differentiated dividends if they are held through a share-holding platform or, in the case of a partnership employee-owning platform established by a non-listed company prior to listing, if they continue after listing

(4) the transfer of shares by a partnership in the secondary market is also not subject to tax exemption on capital gains

(5) the dividends of the investment are not tax-exempted from the dividends of the resident enterprise, and the partners are still subject to a 20 per cent personal income tax based on the principle of “first-in-first-out tax”。

Iv. Elements for the treatment of equipment

Basic principles: the transaction price shall be determined in accordance with the principle of independent transactions, and the tax authority shall have the power to adjust it if the price is manifestly unfair

2. Several mispricing areas:

(1) “change of the sun”

(2) prior period transaction prices exist without reference

(3) the subject company, which deals with assets that may have significant added value, such as real estate, patents, or mining rights, and fails to comply with evaluation procedures, still deals at book value, resulting in unfair transaction prices。

Concluding remarks

In view of the differences and special circumstances in the calculation of the relevant taxes and fees in the course of the transfer of shares, which are discussed in the context of the different identities of the subject of the transfer, it is necessary to make further judgements on the basis of the above lines of reference in the specific transaction and to provide advance information and communication with the tax authorities。

Thanks for the attention