01 industry drivers

New energy vehicles and storage dual-wheel drive

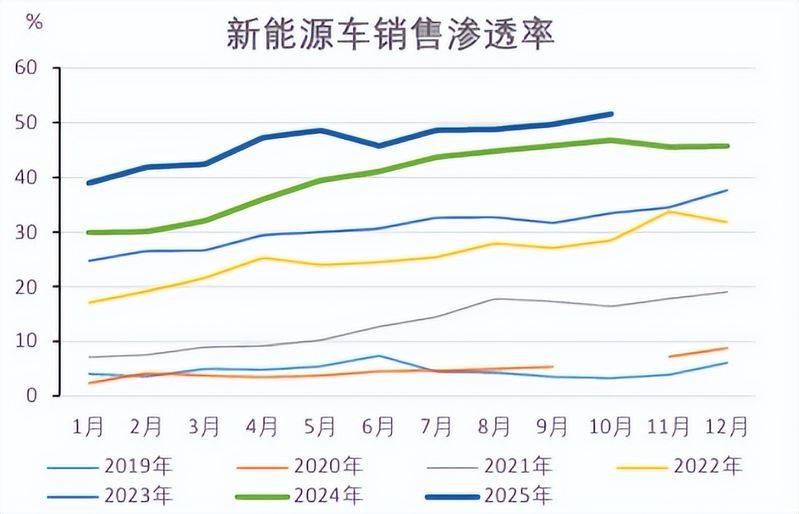

Since 2025, the lithium carbonate industry has witnessed substantial improvements in supply and demand patterns, driven by sustained increases in the penetration of new energy vehicles and over-anticipated growth in the storage market。

By october 2025, our new energy vehicle production had increased by 33. 1 per cent and 32. 7 per cent, respectively, and exports had increased by 90. 4 per cent each year, with a steady penetration rate of over 50 per cent。

Another driving force is in the area of energy storage, with global production of lithium-capable batteries reaching 430 gwh in the first three quarters of 2025, more than 30 per cent of the total in 2024, with a projected annual delivery of 580 gwh, an increase of 84 per cent over the same period。

The centralized release of downstream demand has greatly drained pipeline stocks。

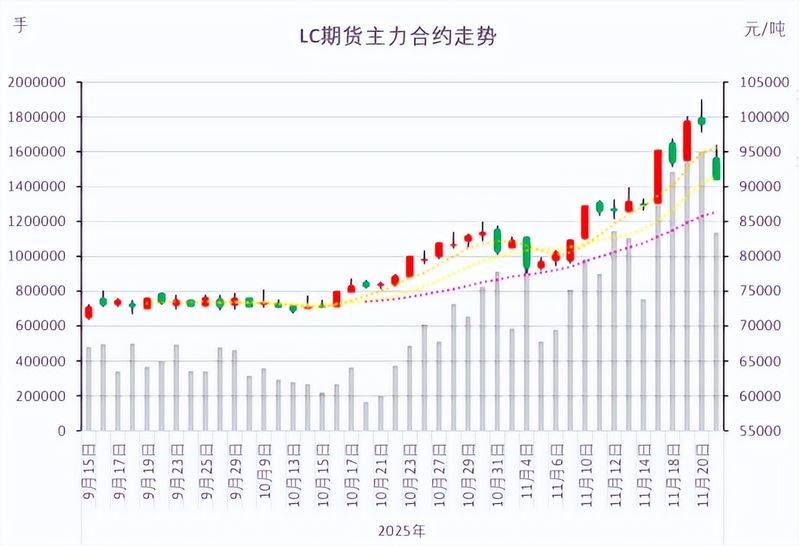

The price of lithium carbonate rebounded strongly

In november 2025, the price of the lithium carbonate futures contract exceeded a maximum of $100,000 per ton, while in june, the lowest price was just $5. 85 million per ton, an increase of over 70 per cent in months。

This round of price rebound marks the prospect of the end of a low peak in the industry that lasted for more than two years, with a clearer signal of the bottom reverse。

02 industrial panorama

Upper chain 03

03-1 lithium resources

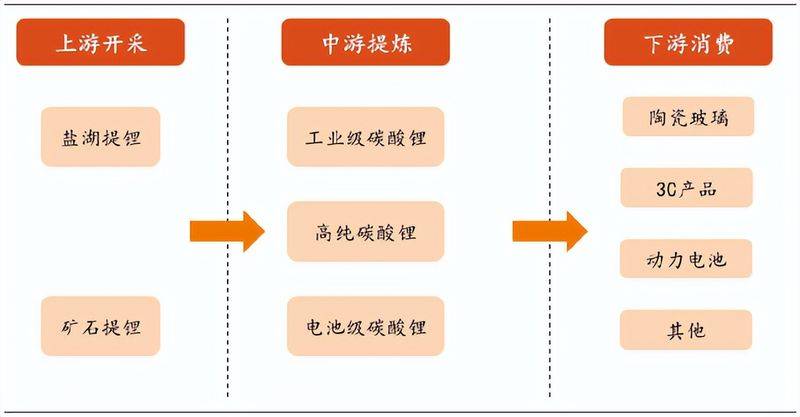

Lithium resources are fundamental to the production of lithium carbonate, mainly from lithium platinum ore, salt lake halogenated water and lithium clouds。

Our lithium resources meet market demand mainly through subsistence and imports。

In recent years, through a new round of mine-seeking operations, our global share of lithium deposits has risen significantly from 6 per cent to 16. 5 per cent, and we have jumped from sixth to second place globally。

This breakthrough resulted from the newly discovered west kunlón-sonpan-ganz lithium-plain belt, which aggregates over 6. 5 million tons of resources and has a potential of over 30 million tons。

At the same time, our additional resources for lithium salt lakes amount to more than 14 million tons, making our country the third largest global base for lithium salt lakes。

Together with the lithium resources of sichuan, qinghai and tibet, these findings constitute the western “asian lithium belt”, which provides a solid resource base for the autonomous and safe development of our new energy industry and reduces dependence on imports。

03-2 lithium technical route

The process of production of lithium carbonate is closely linked to its source of resources, and the choice of technical routes directly determines cost competitiveness。

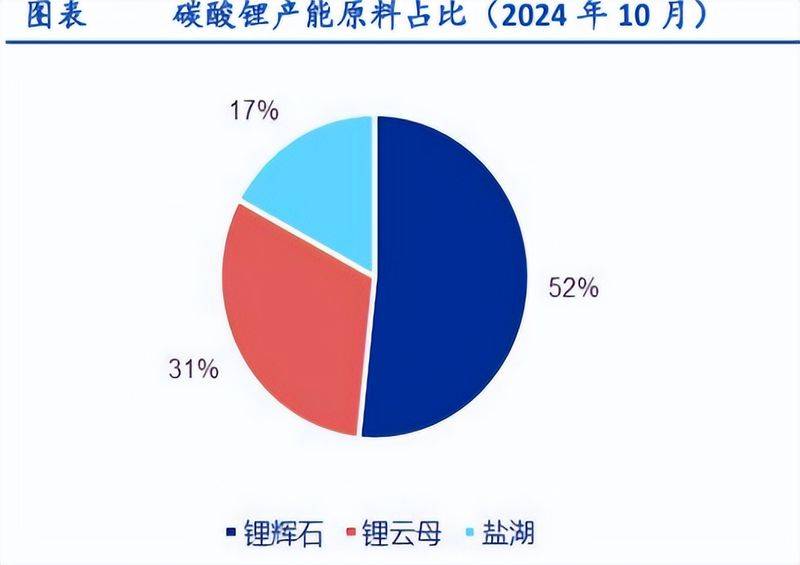

Lithium is the least expensive in salt lakes and is extracted from halogenated water mainly by techniques such as toad adsorption and membrane separation. For example, the salt lake shares used the “sort-+ membrane” technique as a cost pole for lithium in salt lake. However, magnesium and lithium are difficult to separate due to the complexity of halogenated components。

Lithium trithon is the main source of our capacity for lithium carbonate, accounting for 52 per cent. The route is well developed, mainly by sulphuric acid, but faces the challenge of high energy consumption and solid waste, and is more affected by ore prices。

Lithium mackerel is concentrated in jiang xie-chun and is an important element in achieving domestic resource autonomy. Costs have been significantly reduced through technology over time, such as the fourth generation of sulfate。

03-3 related target

The lithium industry: the global leader of the lithium industry, with a global set of multiple types of lithium resources, covering “halogenated lithium” “ore lithium” and “recovered lithium”, has the advantage of an industry-wide chain。

Lithium tinzi: holding one of the largest solid lithium platinum mines in the world, with high resource self-sufficiency, high-quality resource advantage and very low cost of lithium。

Salt lake share: tsalkhan lake, china's largest salt lake, cost as low as 30,000 yuan per ton, based on adsorption plus membrane technology。

Zelig mining: lithium in the concentrated salt lake, the area of interest in the tsalkhan salt lake is large, the lithium is low and the lithium is more efficient。

Tibet mining: the zabuye salt lake, with exclusive mining rights, is the largest lithium salt lake in asia, with the second highest lithium-containing concentration in the world。

China mineral resources: a pioneer in the development of lithium mines overseas, with a focus on the development of african lithium platinum。

04 middle-range industrial chain

Classification of lithium carbonate 04-1

Lithium raw materials are processed to form various lithium compounds such as lithium carbonate and lithium hydroxide。

Of these, lithium hydroxide is mainly a high nickel tri-polar material used in high-end new energy vehicles, while lithium carbonate is widely used in the area of phosphate lithium orthodox, energy storage batteries and traditional chemical industries。

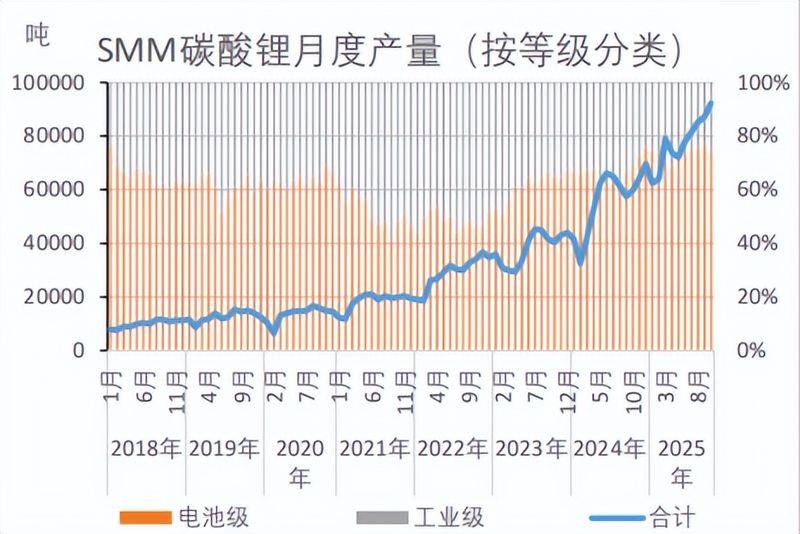

Depending on purity and critical impurities, lithium carbonate is divided into three main categories: industrial, battery and high-purity lithium carbonate。

Lithium carbonate cell-grade is an essential core material for the orthodox materials of lithium batteries with a purity of more than 99. 5%。

According to statistics, in the first three quarters of 2025, domestic battery-grade lithium carbonate production accounted for more than 70 per cent of total lithium carbonate production and became an absolute dominant product。

The industrial-grade lithium carbonate is mainly used in traditional industrial areas such as ceramics, glass, americium and rare earth smelting, with purity generally ranging from 98 to 99 per cent。

In addition, lithium high-purity carbonate is emerging as a new focus for a new generation of high-performance lithium ion and solid cell batteries with a purity requirement of 99. 99 per cent or more。

Technical barriers to the preparation process are highest, usually on the basis of battery-grade lithium carbonate, with deep purity using methods such as hydrogenization-ion exchange combinations to accurately control the content of specific impurities。

04-2 lithium carbonate supply and demand

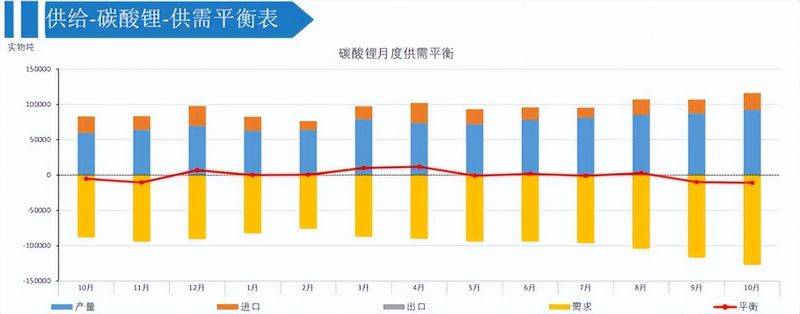

Our market for lithium carbonate is now in a new pattern of “breathing supply and demand and tightening structures”。

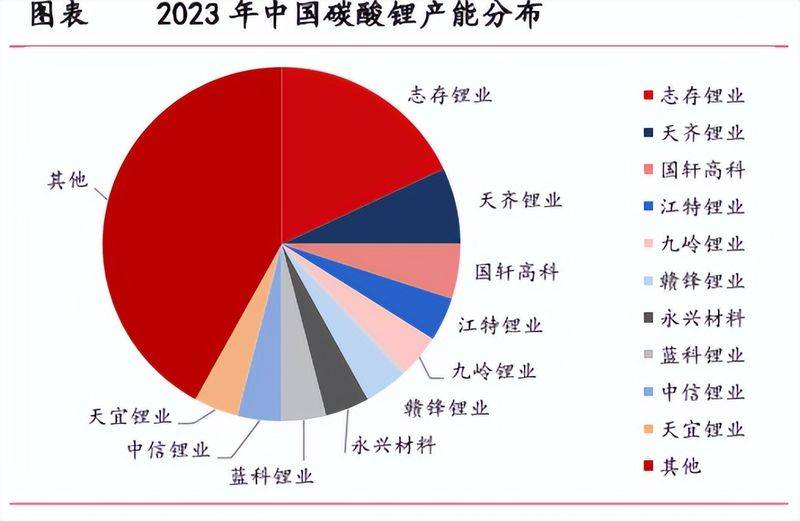

On the supply side, the production of lithium carbonate is relatively concentrated in the distribution of enterprises, with production capacity reaching 1. 3 million tons in 2024, but actual production in that year was only 701,000 tons, with a capacity utilization rate of about 54 per cent, reflecting the contradiction between large capacity planning and the moderate release of actual production。

In 2025, an additional 260,000 tons are expected to be supplied domestically, with a total production expected to reach about 800,000 tons。

Certainly, on the demand side, there has been a marked shift in market patterns as markets continue to disappear, driven in particular by a combination of robust growth in the sales of new energy vehicles and a surge in reserve capacity in 2025。

Looking ahead, as demand growth is expected to continue faster than supply growth, this tight balance may continue and even evolve into a clear supply gap in the future, pushing markets into a new cycle。

04-3 related target

New lithium energy: the capacity for lithium salt production is the highest in the world, the velvet lithium mine is the largest hard-rocked monomer lithium mine in asia, and indonesia has expanded to the most productive ore lithium project overseas。

Acacia group: for many years, deep-drived in the field of fine processing of lithium salt, it has developed a large-scale production capacity for high-purity lithium carbonate。

Zhongxiang: i have the right to prospecting and mining rights for the white water hole, the sud-nam section, the au-china mine, and a complete industrial chain of original mining, mining and battery-grade lithium carbonate smelting。

Quantified shares: the country's most productive lithium mining company, owns the country's rare high-quality lithium the mining resource, mecha lithium plumstone mine 134, is the company's largest customer。

Downstream 05

The downstream application of lithium carbonate is highly concentrated and its demand structure is closely linked to the global green energy transformation process。

Currently, the majority of lithium carbonate production is consumed in lithium batteries, which can be divided into three main application plates: power cells, energy storage cells and consumer batteries。

Among them, the power cell, as the “heart” of a new energy vehicle, is the basic disk and core driver of the demand for lithium carbonate。

Owing to the expected impact of halving next year's acquisition tax, some of the demand for early release has so far been concentrated in four quarters of the year, with heavy cards, passenger cars and light-calorized electric projects, leading to a marked increase in power cell orders。

Storage batteries are the fastest growing demand engine。

Global energy storage batteries are expected to reach 1110 gwh in 2028, with an average annual compound growth rate of 24 per cent, continuing to inject strong momentum into the demand for lithium carbonate。

In addition, consumer-type batteries and other traditional industrial applications, such as 3c electronics such as smartphones, laptop computers and ceramics and glass manufacturing, together form a stable base for the demand for lithium carbonate。

These applications together shape stable and resilient market structures for downstream demand for lithium carbonate, and their future growth momentum will continue to depend on the penetration depth of new energy vehicles and the speed at which storage systems are built。

Trends

Overall, the future profits of the lithium carbonate industry are expected to be gradually restored, driven by an over-anticipated recovery in demand, partial production capacity at the supply end and low levels of stocks. The industry continues to expand to a technology-driven and integrated configuration, moving from low-cost competition to value competition as a whole towards a healthy development cycle with a balanced supply and demand。