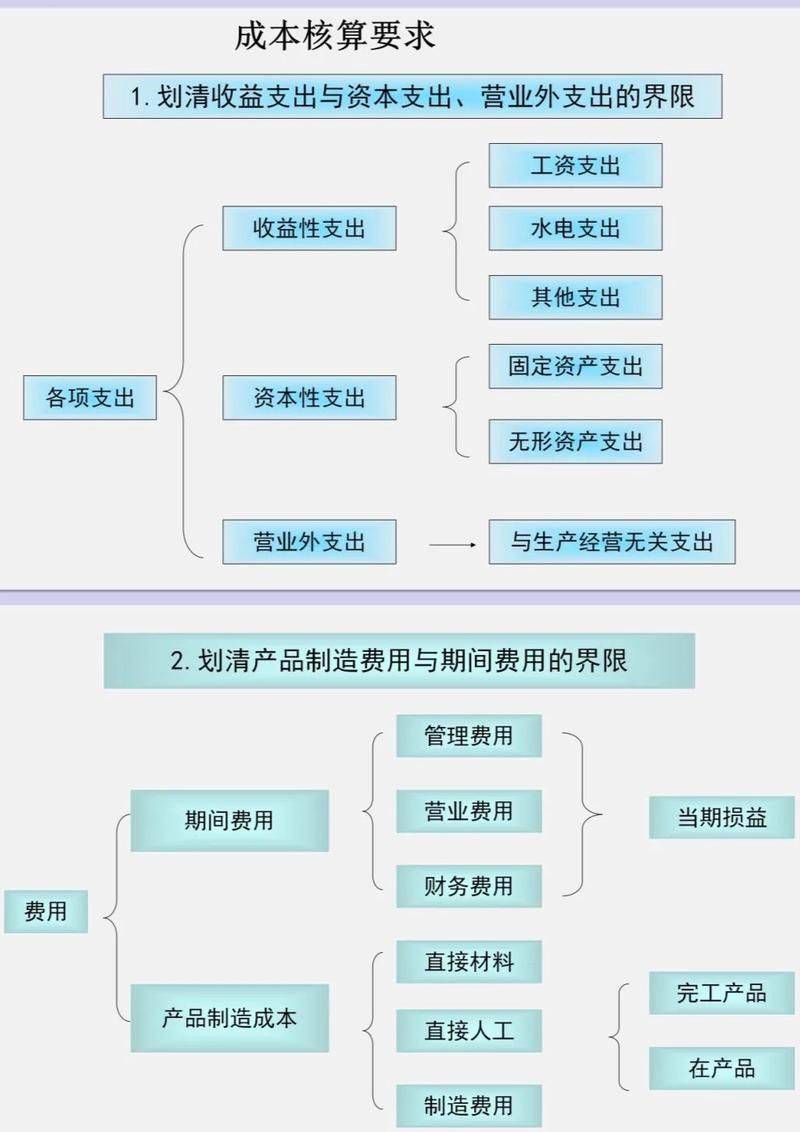

Relationship between manufacturing costs, production costs and inventory commodities

Source: accounting training school in yichang province: 2018/1/26 17:51:05

The accounting training school in yichang province has compiled the relationship between manufacturing costs, production costs and inventory commodities:

1. Manufacturing costs

(1) concept: refers to the indirect costs incurred by the enterprise's production workshops for the production of products and the provision of services, such as office costs, utilities, etc., which form part of the cost of the product。

(2) nature: the costs incurred in manufacturing the production workshop are borne by the product and constitute the cost of the product, which falls under the cost category and forms part of the inventory. Although there are “costs”, it is not a cost-type account。

(3) account setting: “construction costs”, cost type accounts。

(4) application: first, the debits assembled in the “manufacturing costs” account, then transferred to the “production costs” account, indicating the cost of the uncompleted product, and then the cost is carried over to the “inventory goods” account。

Production costs

(1) concept: refers to the production costs incurred by enterprises in industrial production, including the production of products (finished products, semi-finished products, etc.), home-made materials, etc。

(2) nature: the direct costs incurred in manufacturing the products of the production workshops, which constitute the direct materials of the main entity of the product and the direct labour incurred in manufacturing, are borne by the product, constitute the cost of the product, are in the cost category and form part of the inventory。

(3) account setting: “cost of production”, cost type accounts。

(4) application: a debit that is first consolidated in the “production cost” account; or a carry-over cost from the “manufacturing cost” account credit, which represents the cost of the unfinished product and is carried over to the “stock commodity” account after completion。

3. Inventory commodities

(1) concept: refers to the actual or planned costs of various commodities in the stock of the enterprise, including finished inventory, out-of-pocket goods, goods to be sold in front of the ministry of the market, goods to be displayed and goods to be sent outside the premises。

(ii) nature: goods that have been produced and the revenue pool verified as part of the inventory for sale。

(3) account setting: “inventory goods”, asset class accounts。

4. The relationship between manufacturing costs, production costs and inventory commodities

The costs directly comprising the product entity are recorded in the “production cost” account; the indirect costs incurred by the production workshop are first aggregated to the debit in the “production cost” account and then carried over to the “production cost” account, and then to the “stock commodity” account, indicating the cost of the completed product, which is an integral part of the inventory。

“construction costs” “production costs” “inventory goods”

This is the course on accounting for ichangurai, which is a small compilation of the relationship between manufacturing costs, production costs and inventory commodities