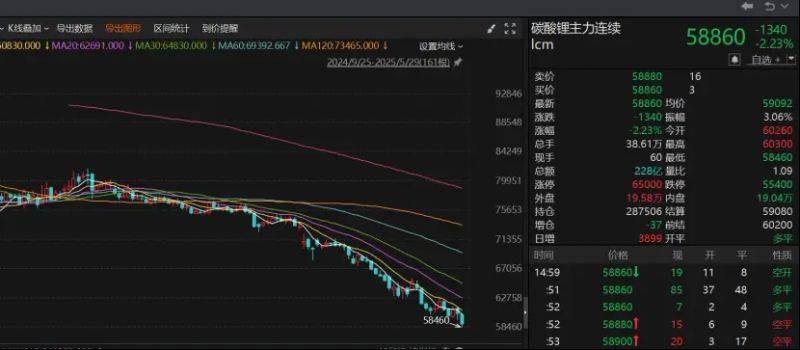

Lithium carbonate, which has fallen, has not stopped the decline. On 29 may, the main futures contract for lithium carbonate fell by 2. 23 per cent and was reported at $58860 per ton, a new low in the year. According to a query, the lithium carbonate futures contract has been in decline since this year, reaching a cumulative decline of 23. 66 per cent compared to the price of the peak of $80,000 per ton at the beginning of the year。

The chinese securities network news report (journalist lee shao peng) has failed to stop the decline. On 29 may, the main futures contract for lithium carbonate fell by 2. 23 per cent and was reported at $58860 per ton, a new low in the year. According to a query, the lithium carbonate futures contract has been in decline since this year, reaching a cumulative decline of 23. 66 per cent compared to the price of the peak of $80,000 per ton at the beginning of the year。

In terms of spot prices, the shanghai steel union data of 29 may show that the battery-grade lithium carbonate (dark disc) fell by $1,000 per ton the same day as the previous day, at an average price of $61,000 per ton, also at a new low in the year。

For the continued downswing of lithium prices, downstream demand is insufficient or the primary cause. Market-based analysis suggests that the current global expansion of lithium resources and lithium salt production capacity, which is growing too rapidly on the market, has been accompanied by a slowdown in demand and increased pressure on enterprise-level stocks, leading to a steady decline in prices。

The price of lithium continues to decline, with the most affected being the lithium carbonate producer. The executive of a lithium mining company in sichuan told journalists that, when they fell by $70,000, what they could do now was to reduce production through cut-off inspections and minimize costs, while continuing to observe market dynamics。

Journalists have been informed that most lithium carbonate producers are currently using cut-off and overhauls to reduce production and minimize costs while reducing market supply。

So what are the subsequent trends in determining the price of lithium for the “fate” of mining upstream? It is generally accepted that lithium prices are not easy to “turn over”. The reason for this is that there is a clear trend towards an increase in the supply of lithium carbonate; that downstream demand is stable and does not increase significantly; and that high-cost production capacity takes time。

In the face of the fact that lithium carbonate prices have not rebounded significantly, industrial companies have to adjust their future plans. According to a lithium company in share a, lower prices can help to phase out higher-cost, less efficient enterprises, promote better and worse outcomes, and concentrate resources on more competitive enterprises。

“consisting weak prices or leading to increased m & as reorganization activities in the lithium industry may result in increased concentration.” in the view of the foregoing, the competitive advantage of integrated enterprises that have developed from upstream resources to lithium salt production will become more pronounced。

Journalists have learned that, although processing companies have been shut down at the smelting end, high-cost lithium carbonate production can be cleared or may take some time. “there are two reasons why lithium salt capacity has not yet begun to be cleared: first, the processing industry's expectations of a warmer price, and secondly, the previous dividends of a boom in lithium prices, which allowed some companies to maintain their cash flow.” lithium mining companies believe。