Research on innovative models for the transformation of future non-performing loans by commercial banks. 1. Analysis of the causes of non-performing loans. 1{\chffffff}{\ch00ff00} ntents page catalogue page the loan office's new model of dealing with innovative models examines the causes of non-performing loans resulting from the analysis of economic factors leading to adverse loan 1. Macroeconomic volatility: economic downturns, deflation and rising interest rates can have a negative impact on the business's ability to operate and service, leading to an increase in non-performing loans. 2. Sectoral restructuring: structural adjustments in certain sectors may lead to the collapse of some enterprises, thus increasing the volatility of the housing market. 3. The negative impact on the value of mortgage loans in the event of a collapse of a housing market bubble or a significant decline in prices can increase the poor management of poor loan operations, leading to poor management of bad loans. 1. Mismanagement of the enterprise: intra-enterprise mismanagement, such as poor business decisions, poor internal controls and poor financial management, may lead to a deterioration in the financial position of the enterprise, leading ultimately to changes in the external environment of the enterprise: changes in the enterprise's external environment, such as technological advances, increased market competition, may lead to difficulties in operating the enterprise and difficulties in repaying loans, leading to poor internal control: internal control will lead to managers to take more personal interests into decision-making, rather than enterprise interests。

Asset support securitization disposal model commercial banking bad loans the main purpose of the loan service disposal model for innovative models of disposal is to reduce bank exposure to non-performing loans, enhance bank risk 3. Asset support securitization disposal is an innovative method of dealing with non-performing loans, increase bank capital adequacy and reduce the cost of banking operations, and support the operation of the securities disposal model. Management of securitized products by professional asset management companies, including asset management, collection and distribution of cash flows, termination of securitized products: when the securitized product expires, the assets held in the securitized product are liquidated and the principal and interest assets paid to the securities investor are the advantages and disadvantages of the securitized disposal model to support the securitization disposal model: 1. Advantages: - risk spread: the asset support securitization disposal model can spread the risk of non-performing loans to the securities investor, thereby reducing the bank's risk exposure and enhancing the bank's risk resistance。

Increased bank capital adequacy: asset support securitization disposal models can improve bank capital adequacy, enable banks to meet regulatory requirements and provide additional financial support for future development to reduce bank operating costs: asset support securitization disposal models can reduce bank operating costs and reduce bank financial burden by two disadvantages: - complexity of operations: asset support securitization disposal models are relatively complex and require specialized personnel and institutions to engage in liquidity risk: asset support securitization products are traded in the securities market, liquidity risks may lead banks to quickly realize legal risks for securitization products: asset support securitization models involve complex laws and regulations, there are legal risks, such as securities issuances that are not in compliance with regulatory requirements, innovations in asset support of securities disposal models that support the bankability of securities disposals: innovative applications of 1. Asset support securities support securitization models, innovative applications of asset support for securitization disposal models include, inter alia, the following aspects such as the sale of securities in the securities market to achieve the diversification of assets, and the development of securities in the securities market to support the diversification of securities to achieve alternative asset-based asset-based asset-based dispositions, such as:。

The expansion of securitization markets: the expansion of securitization markets, the increasing volume of transactions, and the strengthening of securitization controls, which enrich the variety of transactions: the future outlook for enhanced securitization regulation, improved regulatory regulations, increased transparency in securitization markets, and enhanced transparency in asset-support securitization disposal model 1. The future outlook for asset-support securitization disposal model will include, inter alia, the following aspects: - the asset-support securitization disposal model will be more widely applied in the future, one of the main modes of bank non-performing loan disposal will be more regularized and transparent, regulatory regulations will be improved, transparency in securitization markets will further enhance asset-support securitization disposal model, the variety of securitization products will be enriched, and the volume of transactions in securitization markets will further increase the future outlook for asset-support securitization disposal model the new model of the innovative model of disposal of the loan service studies the debt stock-for-equity-for-disposal model 1. Debt equity-for-disposal model means that a commercial bank is based on non-performing loans. Debt equity-for-equity-for-disposal model, in consultation with the debtor, is a method of disposition. Debt equity-for-disposal model can help commercial banks to effectively control the scale and risks of non-performing loans. It can also help the debtor to emerge from a difficult situation and may face a number of challenges in operationalizing the restructuring and development of the debt-equity-for-disposal model。

3) the equity-for-equity-for-debt treatment model may have a negative impact on the capital adequacy of commercial banks. The debt-equity-for-equity-disposal model may effectively reduce the non-performing-lending ratio of commercial banks. The debt-for-equity-for-disposal model may have a negative impact on the capital adequacy of commercial banks. The debt-equity-for-disposal model may have a negative impact on the capital adequacy of commercial banks. The debt-for-equity-for-disposal model may result in some equity-for-equity gains for commercial banks. The debt-for-equity swap-for-equity-for-equity-disposal model may have a negative impact on the maturity of commercial banks. The debt-for-equity-for-equity-for-disposal-for-equity-for-disposal model may face some challenges in operational operations for commercial banks。

Business banks, in consultation with debtors, determine the debt equity swap option. Commercial banks convert non-performing loans into equity holdings. The loan service's new model of disposal innovation studies the bad asset disposal model and the bad asset disposal model: 1. The adr model means that commercial banks entrust unsound assets to the trustee in a fiduciary manner for the disposal and management of the adr and return the proceeds of disposal to the client 2. The adr model has the following characteristics: - specialization in disposal, entrusting institutions to focus on the disposal of bad assets, applying professional skills, professional teams and disposal experience, significantly shortening the disposal cycle, segregating the risk of bad assets from the adr model, enabling commercial banks to escape the risk of bad assets and focus on the development of credit operations。

The adr model allows commercial banks to reap the benefits of an adr and increases the innovation of the adr model for commercial banks: 1. Innovations in the adr model are mainly reflected in the following aspects: innovation in financing modalities, the introduction of equity investments and layers of investment, and the broadening of the diversification of financing channels for trustees, including not only traditional trust companies, but also asset management companies, investment companies and professional adr companies, including the application of multiple types of adr models such as debt swaps, asset securitization, auctions for bad assets, etc.: 1. The bad asset trust disposal model has been widely applied in the disposal of bad assets by commercial banks and has had a positive effect. With the rapid growth of the chinese economy and the continued development of the financial sector, commercial banks' non-performing loan-packing operations have developed rapidly and have become one of the key instruments for commercial banks to address the risks of non-performing loans. 2. Because of the wide range and complexity of the non-performing loan-packing operations, high demand has been placed on commercial banks' risk management capacity, disposal capacity and integrated service capacity. 3. In the future, commercial banks ' unperforming loan-packing operations will continue to show the following trends: firstly, they will be more diversified and flexible; secondly, they will be further expanded; and thirdly, they will be more complex and diversified。

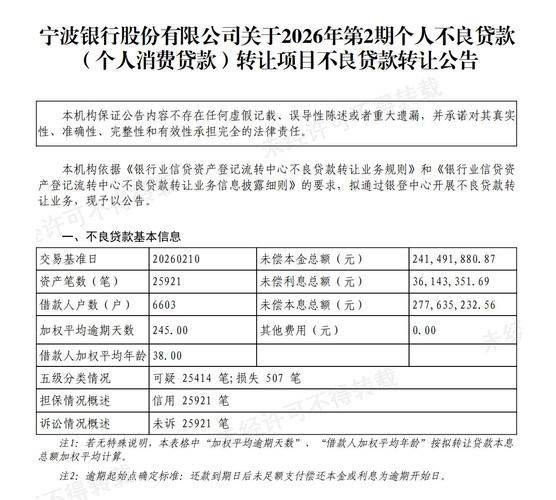

The main ways in which non-performing loans from commercial banks are disposed of are: direct packaged disposal: a commercial bank sells non-performing loans directly to the recipient, which is the simplest and most direct method of dealing with non-performing loans, and indirect packaged disposal: a commercial bank transfers non-performing loans to intermediaries, such as bad asset management companies or trust companies, and is then sold by intermediaries to the subcontractor's third packaged disposal: a trend for commercial banks to sell non-performing loans and other financial asset portfolios to the recipient commercial bank for non-performing loans: a commercial bank's non-performing loan packaged to address the advantages of commercial bank non-performing loans for commercial bank loans: 1. To help commercial banks focus on non-performing loans, to reduce the erosion of their capital and other assets, to improve the quality and credibility of their assets, to improve the efficiency and effectiveness of the disposal of non-performing loans, to achieve rapid disposal of non-performing loans through market-based means, to reduce losses of commercial banks, to promote the development of the market for non-performing loans, to create secondary markets for non-performing loans and to provide more effective platform for the disposal of non-performing loans: 1. Difficulties in pricing non-performing loans: because of the high risk of non-performing loans, it is difficult to determine a reasonable price at the time of packaged disposal, which can easily lead to disputes between commercial banks and the recipient. 2. Information on the disposition of non-performing loans is asymmetric: commercial banks and the recipient have different levels of knowledge of non-performing loans, which can lead to information asymmetries and inadequate laws and regulations affecting the smooth conduct of non-performing loans in packaged disposal 3. At present, the laws and regulations governing the disposal of non-performing loans are inadequate, which to some extent constrains the development of non-performing loans。

Risk control measures for commercial bank non-performing loans packaged to deal with non-performing loans packaged: 1. Strengthen due diligence on non-performing loans: commercial banks should enhance due diligence on non-performing loans before packing to deal with non-performing loans, fully understand the risk profile of non-performing loans and avoid the failure of packing because of the high risk of non-performing loans. 2. Select the appropriate method of packing disposal: commercial banks should choose appropriate packaged disposals based on the risk profile of non-performing loans, the timeliness of disposal and the cost, among other factors. 3. Develop a well-developed risk management system for bad loan packaged disposal: commercial banks should establish a well-developed risk management system for bad loan packaged disposal, including risk identification, risk assessment, risk control and risk control, to effectively control the prospects of poor commercial bank loan packaged disposal at risk of non-performing loan packaged disposal: 1. The bad loan packaged disposal business will continue to develop rapidly and will become one of the key tools for commercial banks to address the risks of non-performing loans. The new model for research into innovative models of disposal by the loan office examines the scope of application of the negative asset disposal model. 1. The negative asset disposal model applies to various types of negative asset, such as mortgage-guaranteed bad asset, non-mortgage-guaranteed bad asset, non-negative loan derivative asset. The negative asset disposal model applies to various types of asset, whether large or small, that may be disposed of by auction。

3. The disposal model for auctions of bad assets applies to the treatment of undesirable assets in different industries, whether passing through。