Still using private households to collect money, private households to avoid taxes? In 2026, the fourth phase of the tax + bank data network has developed a full-dimensional, no-angle regulatory network, and the “safe zone” of private tax avoidance has completely disappeared

Many recent cases have been reported by the state tax administration, covering manufacturing, technology, live broadcasting, and health care, each of which warns that private households must be investigated and punished for hiding their income

Goodbye, private accounts tax avoidance

In february 2026, the general state tax administration focused on several cases of private account theft, in which enterprises and individuals were charged taxes plus late payments plus heavy penalties, and the cost of violating the law was alarming。

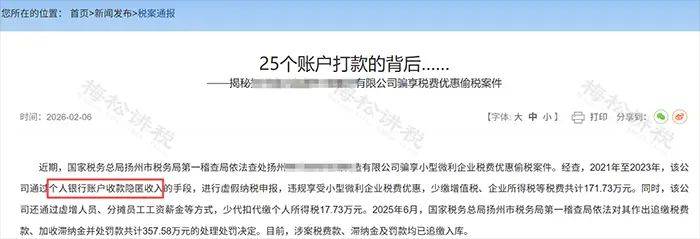

Case one: a manufacturing enterprise in yangzhou - private households conceal their income + cheat on a small margin

In violation of the law: in 2021-2023, the company collected real income through individual bank accounts, made false tax declarations, violated the micro-interested enterprise tax incentives, reduced value-added tax and enterprise income tax, among other things, in the amount of rmb 1. 7173 million; and, at the same time, paid a tax of rmb 1773 million in the form of surrogate increases in personnel and assessed wages。

(b) consequences of violations of the law: ultimately, tax charges, withholding payments and penalties amounting to $3. 575 million, all of which have been fully accounted for。

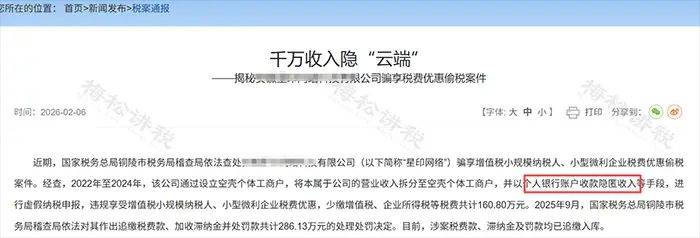

Case two: anhui, a technology company - split income + shell + private collection

In violation of the law: in 2022-2024, the company set up a shell of individual business owners, transferred the business income, concealed it through individual bank accounts, received a small-scale taxpayer, small-scale micro-enterprise benefit under the false declaration, and paid $1. 68 million less。

Consequences of violations of the law: tax, late payment and fines, totalling $28,613,000。

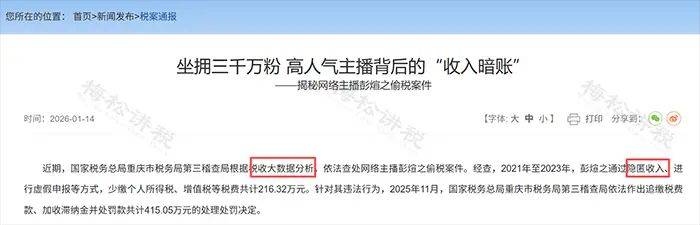

Case iii: high-profile network anchors — multiple accounts scattered to hide revenues

In violation of the law: in 2021-2023, a anchor dispersed collections through various personal accounts, concealed real income, made a false declaration, paid a tax of 2,1632,000 yuan, vat, etc。

(b) consequences of violations of the law: ultimately, they are charged with taxes, arrears and penalties, amounting to $4. 15 million。

All of these cases, without exception, are subject to direct targeting through large-scale tax data, with no “suspicious space”。

Four typical features of private-sector tax fraud (four issues focused on early warning):

1. High levels of income and expenditure from private accounts and a significant mismatch between the flow of funds and the scale of operations

2. Multiple related enterprises are controlled by the same person and related transactions are not consolidated

3. Frequent write-offs, new subjects and attempts to circumvent tax regulations

4 declaration of revenues is far below actual operating costs and data logic is contradictory。

Tax 4+bank networking

The time has come for private accounts to be strictly regulated

Many employers wonder: why do we check now

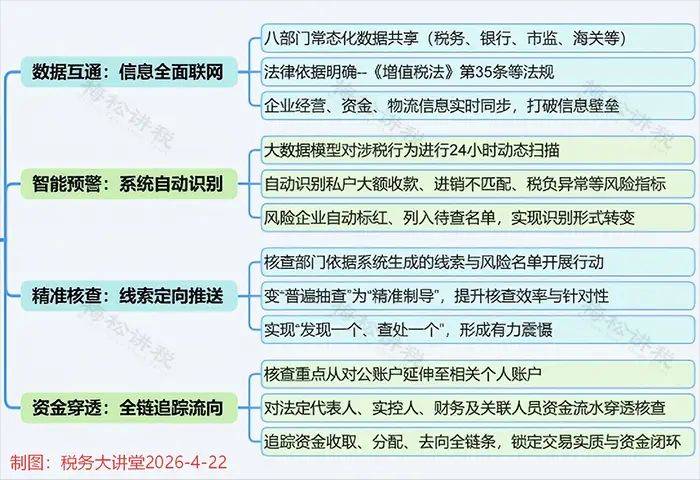

Core reasons: regulatory upgrades have been made to move out of the traditional model of “seek-and-seek, flip-book” and to develop a precision regulatory system for big data analysis + smart warning + penetrating verification。

Four periods of taxation have been achieved, with multi-sectoral data-sharing and cross-matching, such as taxation, banking, customs, social security, market regulation, and individual account transactions within regulatory horizons。

According to the financial institutions large transactions and suspicious transaction reporting scheme, the following may trigger a large transaction or suspicious transaction report by a financial institution:

≥50,000 in single or cumulative cash transactions on the date of any account

Transfers of £500,000 in private accounts and £200,000 in cross-border transactions

3. Two million yuan for individual/cumulative transfers to public accounts

4. Excessive amounts and frequency of private-public transfers

5. There is a clear discrepancy between the nature of the operations and the size of the income collected by the same account, which is frequently collected in the short term。

In short, banks send data to the anti-money laundering monitoring and analysis centre (amlac), tax revenues are channelled through cross-sectoral information-sharing mechanisms, compared to business income declarations and tax returns, and activities such as concealment of income, false billings and private collection tax avoidance are easily detected and verified。

We're in the middle of a tax zone

Just the same

A lot of the bosses are in the wrong zone: personal bank card receipts will be checked, and it's safe to switch to micro-intelligence, to pay for the treasure code

It's a mistake

Under the regulation on the supervision of non-bank payments institutions, non-bank payment agencies such as micro-credit payments and payment treasures are also included in the financial supervision system. Data can be consulted by law and used for tax risk analysis。

This means:

You can't turn private

These nine scenarios are completely compliant

Private individuals cannot be used to conceal operating income, but legitimate “public-private” compliance is fully permitted. The transfer is assured in the following nine cases, where there are supporting and compliance declarations: